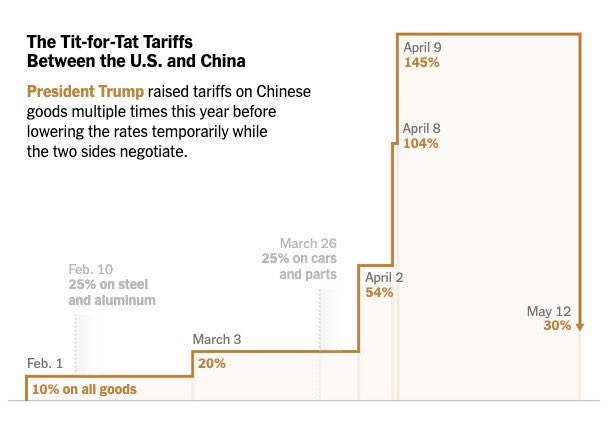

With “significant progress” being made in US-China trade talks, including the announcement of a temporary 90-day “haircut” on tariffs, exceeding even the most optimistic expectations (with each country reducing its tariffs by 115%, i.e. the US reducing from 145% to 30% and China from 125% to 10%), US Treasury Secretary Bessent said that neither side wants to “disengage” the other.

In this context, the view of Thanos Chonthrogiannis, chief economist for Developed markets at Trust Economics, is as follows:

The reduction of US tariffs on China to 30% is indeed a big and positive surprise, given that Trump had hinted that it would go up to 80% at most last weekend. While this reduction may not last forever, it seems reasonable that we may remain at these lower levels.

This Trump setback raises serious possibilities for growth and downside risks for inflation. However, as we have seen with the almost complete reversal of the last few days on the part of Trump, things can change extremely quickly.

It is possible that tariffs will be raised again on July 8 for the rest of the world and on August 10 for China — when the two crucial 90-day periods expire. This is extremely important — it is essentially a “hard reset” and a reversal of bets based on the “stagflationary” US economy and the global growth shock of recent months.

In this case, we now have a significant reduction in the “doomsday scenarios” that focused on a self-inflationary US recession — with the chances of such a development drastically reduced and the relevant positions closed at least until we reach the next 90-day deadlines in July and August.

As a result, pessimism about US macroeconomics, with an emphasis on the stagflationary outlook and a “hard landing”, is being radically redefined, with almost every macroeconomic positioning of recent months being reversed:

“Negative” dollar positions are taking a strong hit — with a 3.5% drop in gold, and significant losses in the euro, yen and Swiss franc due to liquidations and stop-loss triggering.

- Yield curves are being squeezed as the “deepening” trend reverses to a sharp (negative) flattening, with yields at the short end leading the decline and expected Fed rate cuts being postponed indefinitely.

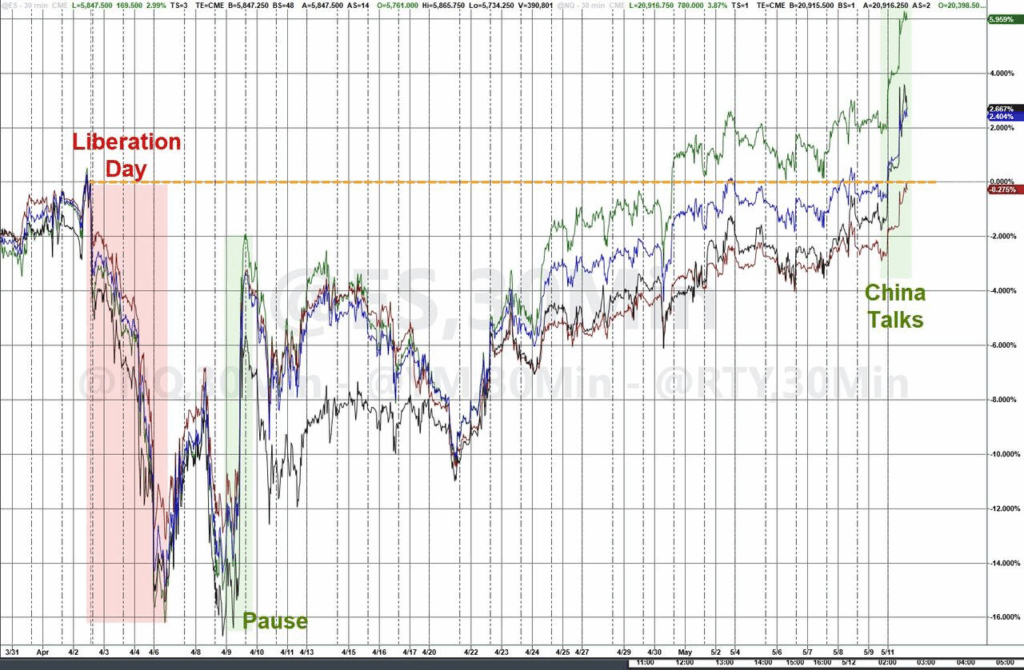

- Global growth indices and oil shorts are in sharp reversal — with crude surging +4.0%.

- US large-cap tech stocks (“Mag8”) — once the main vehicle for over-positioning in the narrative of American “exceptionalism” — are now leading the way, with Nasdaq futures surging +4.0% before the open.

- Cyclical and highly volatile US small-cap stocks are seeing strong gains, with Russell 2000 index futures jumping +4.8% before the open as investors exit defensive low-beta positions.

- On the derivatives side, volatility is sharply down (with the VIX falling below 20) as put options evaporate, forcing dealers to buy stocks (spot futures) to cover the change in their portfolio delta — further fueling the rally.

- The finding is repeated that most investors do not have significant coverage for large upside scenarios through call options — instead, they had sold options to benefit from high implied volatility, estimating that the rise was limited due to concerns about growth and policy uncertainty.

In spot indices, we are now at levels where prices have exceeded critical “short gamma” points for dealers, and we are approaching areas where dealers have positive gamma due to calls sold to them by their clients — any clear break could trigger additional short covering and accelerate the rise.

Cash Flows

From a flow perspective, we spent a significant amount of time discussing the impending “buy” repositioning flows from Volatility Control funds into equities, due to the decline in Realized Vol, as the large extreme sessions since early April have been excluded from the calculation horizon over the past week and a half.

This has led Vol-scalers to repurchase a corresponding amount of equity exposure.

We now estimate that Vol Control funds have repurchased +34.9 billion. dollars in US stocks in the last week (at the 97th percentile), to bring their overall historical exposure back to a less extreme under-allocation in stocks — but only to one more extremely low level: at the 15.1st percentile (over a 3-year horizon) and the 7.7th percentile (over a 10-year horizon).

Moving forward, within this Target Volatility category, a pause is expected after last week’s automatic rebalancing — especially since we see that 1-month volatility has now collapsed well below 3-month volatility.

The latter is probably now acting as a major signal for allocation and remains extremely high at the 96.7th percentile.

This means that it will be a few more weeks before there is a new wave of reallocation, as more “extreme” days need to be removed from the calculation — such days occurred in late February and early March.

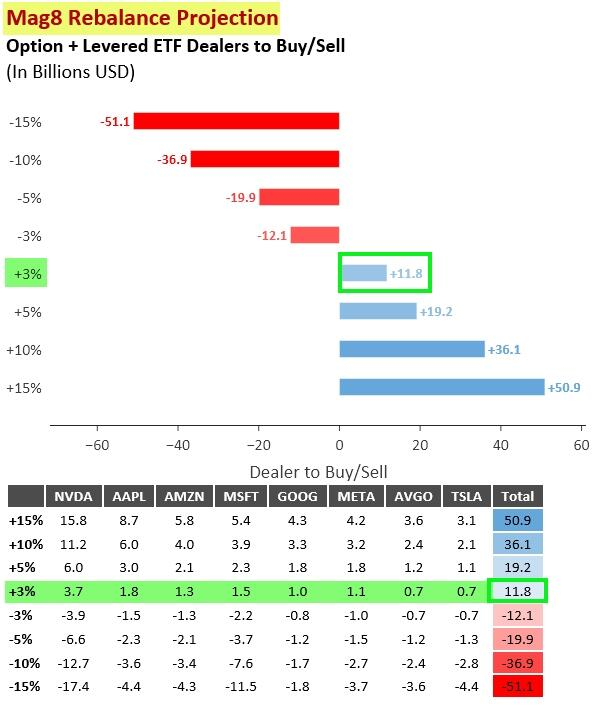

Now that the Target Volatility / Vol Control category has done most of the “heavy lifting,” the majority of mechanical buying in US stocks will come from Negative Gamma — both from “real” sources like Options Dealers, either on individual Mag8 stocks or indices, and from “synthetic” sources like Leveraged ETFs, where EOD rebalancing is particularly sensitive to the performance of the Mag7-8 MegaCap / AI “innovation” tech stocks, which are the mainstay of these products.

Based on today’s “+3%” upside projection to close, it is estimated that there will be +30.9 billion $ of hedging purchases by Options Dealers in indices and leveraged ETFs, as well as an additional +$11.8 billion in implied purchases in individual Mag8 stocks — with a cumulative estimate of +$42.7 billion in additional buying flows today.

Additionally, note the strong optimism from Republican Party circles regarding the Budget Reconciliation, as expressed at the annual US banking sector strategy dinner, attended by Representative and Chairman of the House Financial Services Committee French Hill, as well as legendary economist and current White House advisor Dr. Arthur Laffer.

Of course, not everything is perfect, especially considering the possibility that the strong market recovery could reinvigorate the President’s rhetoric as we approach the various “pause windows” in July and August — where things could “turn upside down” again.

We do not rule out a tariff increase on July 8 for the rest of the world and August 10 for China (the end of the two relevant 90-day periods).

Therefore, it is possible that some tail hedgers may seek to reposition themselves in VIX positions or sell old positions in –Vol and buy new ones for July/August, in case the President cannot contain himself and reopen the front…”

In any case, when we see the consensus of positions reaching “reversal risk” levels due to abrupt changes in the overall market narrative—and prices jumping out of pockets of “negative gamma” and liquidity gaps—it is wise to monitor additional market forces that act as “flow accelerators” and may fuel the downward pressure due to deleveraging in such trades.