Geopolitical developments affect the global economy in real time and the US no longer has the power to deal with the consequences of the crises it causes.

We are already in a new era and the war with Iran is probably the last one that America makes as a superpower. Although the stock market has not yet “registered” the major risks due to the euphoria of AI, the facts are inexorable: The Persian Gulf states with the “thick” wallets that bought the US debt and were a critical source of financing for the financial system and American businesses no longer find a reason to pay premiums to the US.

The US debt will no longer be recycled through “petrodollars”, while the risk of hyperinflation is no longer an extreme scenario, as the former buyers of surplus dollars will be driven to the yuan.

Wars have historically been one of the most important factors in the increase in the public debt of the United States, and of any state at war.

War and the Federal Debt in the United States

- The American Civil War of the 1860s was the first real explosion of debt: the federal debt increased from about $65 million in 1860 to about $2.7 billion after the end of the war – an increase of more than 4,000%. (This huge percentage increase was due to the fact that the debt was starting from an extremely low base, as President Andrew Jackson had completely eliminated it in 1835. In contrast, in later wars the percentage increases appear smaller because the initial debt level was already very high.)

- World War I caused another huge jump, raising the debt from about $2.9 billion in 1914 to about $25 billion in 1920 – an increase of about 760%.

- World War II was even more painful in absolute terms, rocketing the debt from about $51 billion in 1940 to about $260 billion after the war – an increase of about 410%.

- During the Vietnam War, the U.S. national debt rose from about $317 billion in 1965 to about $533 billion in 1975—a jump of about 68%.

- The war in Afghanistan added costs equal to about 59% of the federal debt that existed when it began.

- The war in Iraq in 2003 added costs equal to about 47%.

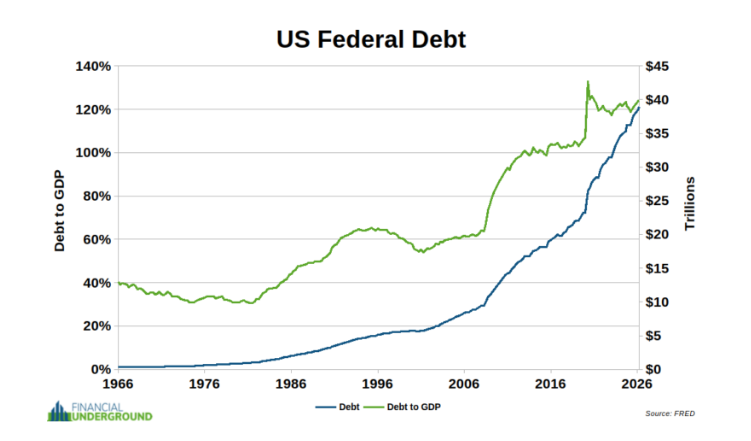

We are now in the third month of the war with Iran. The United States federal debt was about $38.7 trillion when the war broke out and has already surpassed $39.2 trillion.

Where will the federal debt be when the war is over? No one can know. However, it is almost certain to be significantly higher.

Indeed, the equation is true: War = Inflation. But there is an intermediate stage in the process: debt. War spending is financed primarily through borrowing, which is then largely purchased by the central bank with money created “out of thin air.” A more accurate equation would therefore be: War = Debt = Inflation.

Thus, the war with Iran accelerates the US government’s spiral of debt and further strengthens the ongoing depreciation of the dollar, which was already approaching a critical point even before the cumulative effects of the war were taken into account. But that is not all.

The Alarm from the Persian Gulf

Another potential casualty of the war is the petrodollar system, which essentially functions as a protection mechanism for the major oil-producing countries in the Middle East that are aligned with the United States, such as:

- Saudi Arabia,

- Kuwait,

- the United Arab Emirates,

- Bahrain,

- and Qatar.

The petrodollar system has been a key pillar of the dollar’s international power since 1971, when Nixon permanently severed the last link between the US currency and gold.

The logic of the system is simple: the US military “protects” these countries, and in return, they agree to:

- price oil in dollars,

- and reinvest their revenues in the US Treasury bond market and the US financial system.

This supports the dollar and keeps interest rates lower than they would otherwise be.

The oil-producing countries of the Persian Gulf are still significant investors in the US Treasury bond market, although their participation is smaller compared to the largest countries holding US debt such as Japan or China.

According to the most recent data from the US Treasury Department and international financial sources, Saudi Arabia held about $149.6 billion in US Treasuries as of March 2026, while the United Arab Emirates held about $114.1 billion.

Kuwait also saw a significant increase in its holdings, reaching about $66 billion at the end of 2025, a record level for the country.

In total, the major Gulf monarchies—Saudi Arabia, the United Arab Emirates, Kuwait, and Qatar—are estimated to hold approximately $350–500 billion in U.S. Treasury bonds directly, while their combined investments in the United States through sovereign wealth funds, stocks, private equity, and real estate reach several trillion dollars.

The Petrodollar System

The importance of these funds is directly linked to the “petrodollar” system. Since the 1970s, the Gulf countries have priced their oil primarily in dollars and reinvested much of their surpluses in U.S. assets, particularly Treasury bonds.

This process helps maintain high demand for the dollar and allows the United States to finance its public debt at lower borrowing costs. However, in recent years there have been gradual diversification trends.

Recently, Saudi Arabia and the United Arab Emirates reduced their positions in US bonds by almost $17 billion in one month (in March), amid geopolitical tensions and pressures on oil markets.

At the same time, there is increasing discussion about using alternative currencies, mainly the Chinese yuan, in some energy transactions.

Despite these developments, the dollar still maintains a dominant position in the global financial system.

Total foreign holdings of U.S. bonds remain at historically high levels, with the U.S. Treasury Department estimating that total foreign holdings of U.S. securities will exceed $35 trillion in 2025.

However, this system now appears to be rapidly weakening. The war with Iran reveals the limits of American military power and the inability of the United States to provide the protection that it believed the Arab Gulf states were providing.

Iran has shown that it is now the new decisive player in the region and that American security guarantees are not only insufficient but may also be destabilizing, as the American presence introduces risks and instability into the region’s regimes.

With the Strait of Hormuz closed and important energy infrastructure destroyed, oil exports have fallen significantly.

This means that far fewer petrodollars are now returning to the US government bond market. This is another negative factor for the US Treasuries market.

There is not only reduced demand for US bonds due to the shrinking recycling of petrodollars; there is also the risk of active sales – a sell off.

The currency swap lines

The United Arab Emirates has reportedly considered selling some of its US bond holdings – which make up a large part of its $285 billion in foreign exchange reserves – to offset the loss of oil revenues.

Instead of selling and causing turmoil in the markets, however, they have reportedly negotiated a currency swap line (for more information on this issue please read the analysis titled “The FED’s $ liquidity swap line to the Gulf countries is to obey the $, so that they do not head towards the CN¥“).

Treasury Secretary Scott Bessent described these lines as a means of: “preventing a disorderly sale of US assets.” It is clear that there is a strong concern about pressures on the US bond market.

At the same time, Iran has openly stated that one of the conditions for the safe passage of oil tankers through the Strait of Hormuz is the payment of a fee in Chinese yuan, about one dollar per barrel of oil.

According to information from The Liberal Globe, more than 20 countries have already accepted these new terms. Iran appears to be accumulating these revenues in Chinese bank accounts and then using the yuan:

- to purchase physical gold,

- or Chinese goods and raw materials, some of which directly strengthen its war effort.

Japan is reportedly one of these countries. Tokyo is hugely dependent on imported energy, as about 90% of its oil passes through the Strait of Hormuz.

This explains reports that Japan may even use the Chinese yuan — the currency of a strategic competitor — to maintain uninterrupted energy supplies. It is possible that we will gradually see the petrodollar system give way to, or coexist with, a “petroyuan” system.