-The White House narrative is simple: The war with Iran has shattered the Persian Gulf economy, and the US is offering its allies a lifeline.

-The mainstream media narrative:

- The Wall Street Journal described the proposed dollar swap line with the UAE as a financial safety net.

- The Financial Times called it a “bailout.”

- CNBC spoke of a “bailout.”

-The real question: who gets access to the Fed’s balance sheet — and on what political terms.

Mainstream media coverage points vaguely toward the instability of war with Iran… But the balance sheets point elsewhere.

Although the narrative is neat, the numbers don’t add up

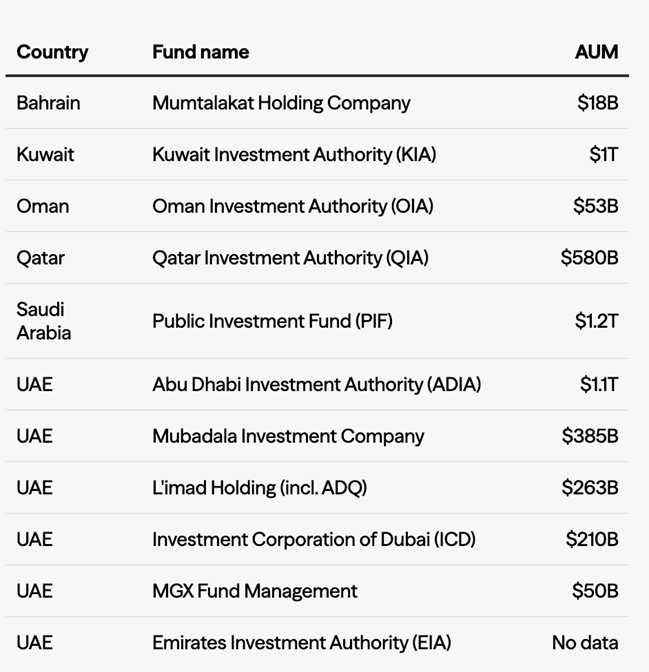

The United Arab Emirates has $270 billion in foreign exchange reserves and about $2 trillion in sovereign wealth funds. The country that is supposedly being “bailout” holds ten times more dollars than the fund used to bail it out.

Bailouts save the weak – supposedly. In this case, they protect a system that cannot withstand Gulf disobedience. In mid-April 2026, the governor of the UAE Central Bank, Khaled Mohamed Balama, raised the idea of a dollar swap line during his meetings with US Treasury Secretary Scott Bessent in Washington. The news was reported by the Wall Street Journal.

A few days later, Bessent defended the idea before the Senate Appropriations Committee, calling the swap line, in his words, “a testament to the primacy of the U.S. dollar and the strength of the U.S. economic shield.” When asked on CNBC and “Squawk Box” if he supported the move, U.S. President Donald Trump responded, “If they had a problem… I would be there for them.”

A swap line is a back-up arrangement between two central banks. Think of it like an emergency water pipe between two houses. Nothing flows until the valve is turned on, but the mere existence of the pipe reassures the neighborhood.

Three things are worth noting about the announcement:

- Nothing has been signed.

- No money has been moved.

- Even the UAE embassy has reacted publicly. Any suggestion that Abu Dhabi needs external financial support, the embassy said, “misrepresents the facts.”

So if the country being “rescued” denies that it needs a bailout, what exactly is Washington announcing?

- The UAE has ten times more dollar reserves than the entire fund that Bessent can tap without resorting to Congress.

- That fund—the Treasury Exchange Stabilization Fund (ESF)—is limited to about $219 billion. Only the reserves of the Central Bank of Abu Dhabi exceed that.

- Add in the Emirati sovereign wealth funds, and the “rescuer” appears with a thimble against a flood that… doesn’t exist.

- Bessent told the Senate that “many other countries, including some of our Asian allies,” have requested their own swap lines. He described the goal as creating “new dollar financing centers in the Gulf and Asia.”

- The Emirates’ request may be the entry point, but Washington is planning something broader: a regional liquidity map based on the dollar, just as the Gulf region’s reliance on American protection is beginning to wane.

The swap line is a pre-fabricated leverage infrastructure — designed not for a liquidity shortage in the UAE, but for the day Gulf capitals decide the dollar is no longer worth the obedience it demands.

The Dollar Recycling Machine Begins to Break

- For more than 50 years, the dollar has been running on a silent engine.

- The Persian Gulf sells oil priced in dollars.

- These dollars return to the United States through Treasury bonds, real estate, stocks, and arms purchases.

- John Perkins, author of “Confessions of an Economic Hit Man,” described it as the way the empire pays for itself.

- This return of capital is what makes an 8% federal deficit sustainable. The American economy does not balance its books — it leaves that balance to those who recycle surplus dollars.

- The Gulf has been the only financier whose contribution is directly tied to oil.

- The war with Iran and the blockade of the Strait of Hormuz did not destroy the Gulf.

- The Gulf remains solvent.

- What was called into question was the recycling process itself.

The Investment Pledge

In May 2025, Trump’s tour of Riyadh and Abu Dhabi resulted in two of the largest commitment packages in modern American diplomacy.

- Saudi Arabia pledged $1 trillion in investments in weapons, energy, and infrastructure, including a $142 billion arms deal—the largest in American history.

- The UAE pledged $1.4 trillion over 10 years, targeting artificial intelligence, semiconductors, and biotechnology.

Both packages relied more on memorandums of understanding than on binding contracts.

US security guarantees offer nothing

A year later, with the war with Iran in full swing, the Strait of Hormuz contested and Gulf capitals seeing that US security guarantees do not offer the expected protection, one question hangs over these memoranda: will they finally be implemented?

And if Riyadh and Abu Dhabi are no longer sure that recycling dollars to Washington ensures their security, why continue to do so at the same rate?

The swap line appears at the very moment when this question is being asked. A warning shot to those betting against the dollar.

It is worth seeing who is at the center of this initiative

Scott Bessent made his fortune in 1992 by betting against the British pound with George Soros, contributing to the collapse of the Bank of England in a single afternoon. He spent his career as an aggressive investor looking for weak currency systems to exploit. Now he is the man called upon to protect them.

The fund from which he draws his resources, the ESF, is limited to about $219 billion. That is the amount of money he can use without congressional approval. Compared to the scale of the problems, that is “small change.”

So what does this announcement actually do?

It is a warning shot to the trading floors of London, Singapore and Hong Kong — the places where the next big bet against the dollar could be made.

Bessent knows these rooms, because he once sat in one of them himself. And he also knows that a credible threat can work like a real fire. The goal is to make the trade appear “overloaded” before it even starts. The message is in his own words.

Bessent did not describe the swap line with the UAE as an emergency measure. He called it “an important first step” toward permanent dollar funding centers in the Gulf and Asia. The “pipes” are already leading east.

The mainstream media presents the swap line as a bilateral affair.

The factor no one is talking about is China

- The UAE has had a yuan swap line with the People’s Bank of China since 2012.

- Saudi Arabia signed its own in November 2023.

Both are participants in Project mBridge, the Chinese-inspired platform that allows central banks to settle in their own digital currencies, bypassing the dollar.

China’s yuan swap network now covers more than 40 countries. The Fed’s permanent network reaches only five. When UAE officials warned in April that oil sales could be shifted to yuan, the mainstream media took it as a bargaining chip. It was not a bluff. The infrastructure was already in place.

The pattern is not limited to central banks. Ten days after the UAE’s warning, Saudi Arabia gave its 12 million citizens direct access to Alipay+, China’s consumer digital payments network.

Riyadh is building alternatives at every level: central bank settlements via mBridge, consumer payments via Alipay+, and the national mada network beneath it all.

You don’t need to announce a shift when the infrastructure is already there. First you build the alternative. Then you let the dollar reliance erode on its own.

Bessent’s “permanent financial centers” in the Gulf and Asia come after China has spent 15 years building the infrastructure for trade beyond the dollar system. Washington is now asking the Gulf to recommit to US-controlled dollar liquidity channels, at a time when the alternative is no longer theoretical. And after the war with Iran, which exposed the limits of American security guarantees, this demand has less weight than in the past.

The Fed’s gate opens inward

The real change begins with Kevin Warsh’s entry into the game when he takes over the Fed. Jerome Powell, the outgoing Federal Reserve chairman, is not leaving with a clean record.

In January 2026, the Justice Department issued subpoenas to the Fed, threatening criminal charges related to Powell. Powell himself called the investigation “a pretext” to pressure the Fed on interest rates.

Trump had repeatedly indicated that he wanted Powell removed, but the pressure campaign was later weakened when a federal judge rejected the Justice Department’s subpoenas.

Warsh is no neutral technocrat. He is a former Morgan Stanley banker, with a personal fortune of more than $100 million, who last year received $10.2 million in consulting fees from Stanley Druckenmiller’s family office.

He is also married to a member of the Lauder family — one of Trump’s largest donor networks, with deep connections to the political architecture of the Abraham Accords.

The man who is being positioned to open the Fed’s gates to the Gulf does not come from outside the very system for which those gates are built.

In his formal answers to Senator Elizabeth Warren and other Democrats on the Senate Banking Committee, Warsh articulated the doctrine that makes all of this possible.

“The Fed’s independence is at its peak in the operational conduct of monetary policy,” he wrote. “This degree of independence does not extend to the full range of functions assigned to it by Congress.” On issues “affecting international finance,” Warsh added, “the Fed will work with the Administration and Congress.”

The Fed’s gateway to the global economy is being handed over to the executive branch by the man who will guard it. Three men now sit at the heart of this architecture.

- Bessent at the Treasury—the aggressive investor who once broke up a central bank—is presenting the proposal.

- Warsh at the Fed holds the keys to the liquidity that supports it.

- And the Lauder family, behind both, operates as a political machine to promote the Abraham Accords in the Gulf.

Conclusion-Forecast

Does liquidity follow “normalization”? Will the Fed gate open for the Gulf states that sign the Abraham Accords and remain closed for the rest?

From now on, watch who gains access to US liquidity channels. That will answer the real question. The rest are already building their own.