Liquidations, steepening and sell-off – The new phase of volatility in global bonds has begun. At a time when the positive side of the distribution curve in US stocks was starting to gain interest again (as we were approaching the point of exercise of options dealers’ “short” positions above 6,000 units of the S&P 500), Trust Economics warns that macroeconomic dysfunction is returning.

After a decade – and more – of “American exceptionalism” and “bold quantitative easing” that favored overinvestment, which is now starting to lose momentum.

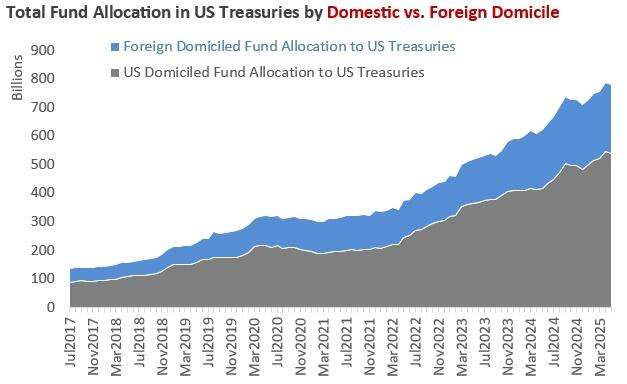

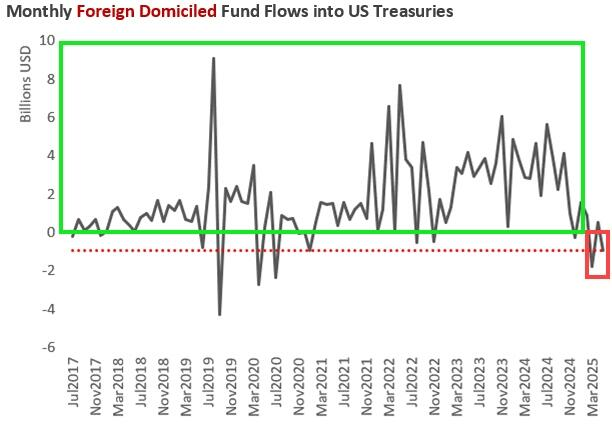

There are still a lot of positions in US Treasury bonds owned by foreigners (R.O.W.), which are gradually being liquidated / restructured. The simultaneous hemorrhagic sell off in both the dollar and long-term US Treasurys (USTs) reveals further vulnerability for both.

Trust Economics argues that the current momentum regarding the dollar and the “decomposition of US exceptionalism” is not only related to the shrinking growth premium and interest rate differentials with the rest of the world.

It is also related to the sudden shift to “Plan B” of Trump’s trade policy, under which tariffs are now being reduced and exchange rates are taking center stage, with the aim of bilateral agreements on parity – as reported almost weekly by Asian sources (e.g. yesterday: “S. Korea says FX talks with US ongoing, but no decision yet”).

Result? Huge demand for put options against the dollar against the euro, yen, Swiss franc and sterling.

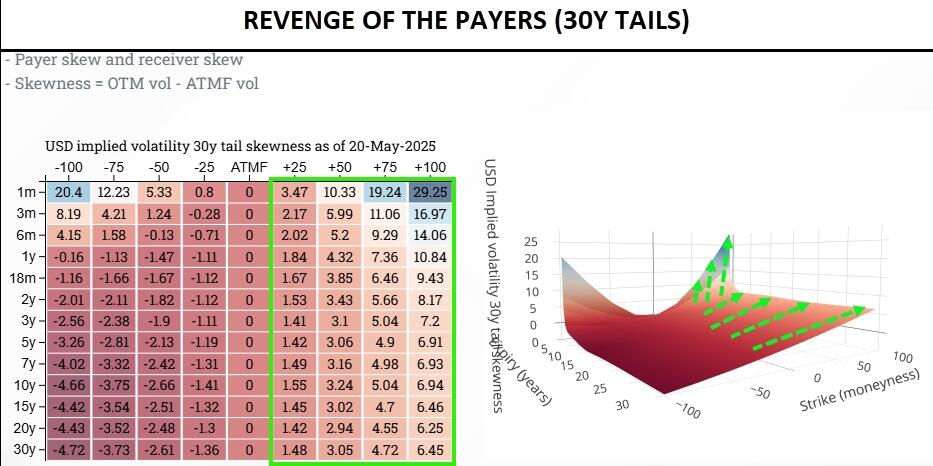

Steepening

The US yield curve remains too flat, given the current wave of fiscal mismanagement, which requires a restructuring of the term-premium (long-term risk), and leads to a continued steepening, i.e. an increase in the yield spread between short-term and long-term bonds.

This is boosting demand for long-term (e.g. 30-year) caps/options-style yield curves, as the global long-term bond market is in an extremely fragile state.

In the past, we have always seen support at the far end of the curve from all regions whenever the 30-year yield reached 5%, but to date we have not seen much interest. It seems that we will have to test even higher yields for interest from Asia to return.

TLT ETF flows were -1.1 million / 01 and confirm continued weakness in the long term.

In swaps, the pain trade appears to be the continued decline in spreads, and we expect a test of -60 points in the 10-year in the near future.

Deficits

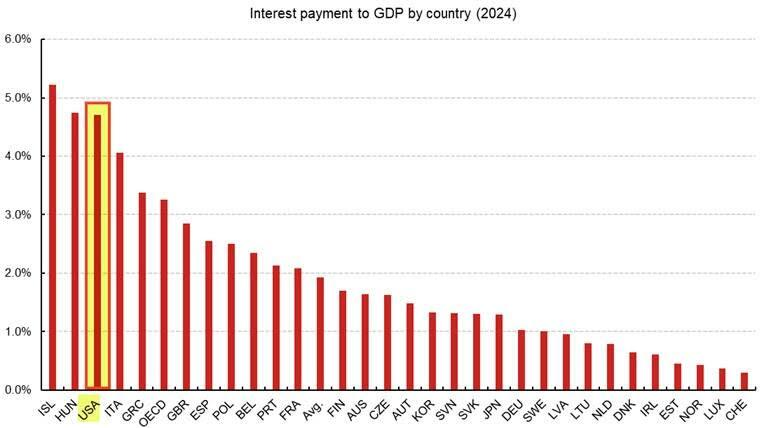

The trajectory of US fiscal deficits is off-track, thus incorporating: Inflation risk, increased debt service costs, increased likelihood of “negative” outcomes

And all this, while nominal GDP remains strong, thanks to simultaneous high growth and inflation rates, a result of the post-COVID era of fiscal support packages. This keeps the Fed “stuck” in a restrictive policy, away from deep interest rate cuts.

Meanwhile, the expectation of a recession is not borne out, as companies continue to avoid layoffs (thus keeping wages and employment levels stable).

This maintains the narrative of the “miracle of the American consumer,” but it looks like a zombie economy that could collapse if margin squeeze begins and hits corporate profits, causing layoffs.

Regarding the Republican budget fight in the House – a little while ago, Speaker Johnson said they agreed to a $40,000 SALT deduction limit.

Thus, the message to the market is that the final package will have more upfront “stimulus” due to tax cuts – however, with such a narrow majority in Parliament, it is not ruled out that the final package will be more “austere” and disappoint expectations for a strong support package.

It’s not just the US…

But Trust Economics says it’s not just the US… And the global bond market has many reasons to be under pressure:

Europe is scrapping old austerity rules, issuing huge amounts of debt to repair decades of deindustrialization, defense/security dependency, and energy mistakes.

Japan is getting the most attention, following the explosive rise in JGB yields and the failed 20-year auction two days ago.

In Japan, domestic investors (insurance companies, pension funds) have become overweight in duration due to decades of QE, ZIRP and NIRP by the Bank of Japan – which is now reducing its JGB purchases from July 2024.

Now the central bank is forced to tighten monetary policy, having emerged from a deflationary vicious circle and facing real inflation and wage growth.

And let’s not forget… in a world focused on recession risk, we are currently seeing hot CPI (inflation) in the UK and Canada, while at the same time, companies like Home Depot, Lowe’s and Amer Sports are expressing optimism for the consumer.

Conclusion

According to Trust Economics, there will be no serious demand for duration (long-term bonds) in this environment until a new “net equilibrium price” is determined, i.e. a larger term-premium, which compensates for the above risks. And all this… on the day of the 20-year UST auction! Will the bond punishers wake up and use their power?