The roots of the US economic hardship are found in the dollar, the head of the “wise men” of Donald Trump’s government, Stephen Miran, found in a study he wrote in November 2024 (“A User’s Guide to Restructuring the Global Trading System“) and which is the guide to Trump’s economic policy regarding international trade/tariffs and currency.

Why has Donald Trump imposed sweeping tariffs on every economic partner?

The global uproar that has erupted leaves the economic logic behind the logic of tariffs in the dark.

Central axiom: The structural problems of the ruling economic order with regard to the US economy are rooted in the persistent overvaluation of the dollar and asymmetric terms of trade.

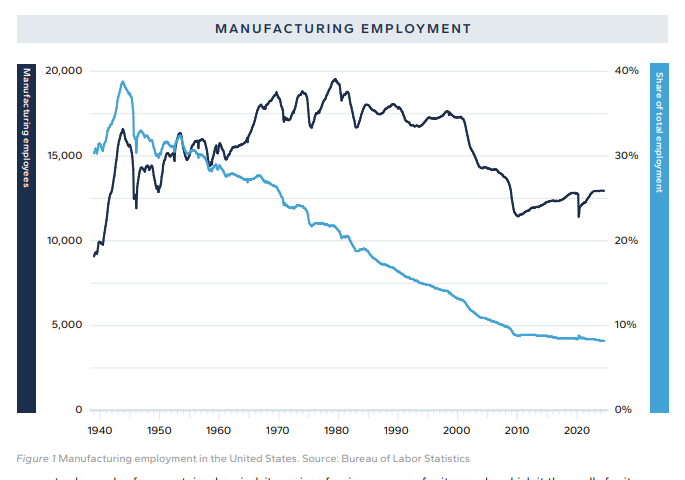

This overvalued currency makes U.S. exports less competitive, imports cheaper, and creates a structural disadvantage for manufacturing. Manufacturing employment declines as factories close.

Local economies shrink, many working families are unable to support themselves and become addicted to government benefits or opioids or choose to leave their homes.

Local communities die

M’Iran notes that between 600,000 and 1,000,000 jobs were lost in the U.S. between 2000 and 2011 due to the “China shock.” Including broader categories, the number of jobs lost during that decade was closer to 2 million.

Another 2 million were estimated to have been lost. jobs lost in a decade amounts to only 200,000 per year, a fraction of the upheaval in employment that occurs each year due to technology or the fluctuations of the business cycle.

But this logic was flawed in two ways: Estimates of job losses due to trade have increased over time geometrically.

1. The “China shock” was much larger than initially estimated. Indeed, many non-manufacturing jobs that depended on local economies were lost as well.

2. Τhere was an asymmetry in the distribution of job losses as they were concentrated in states and specific cities where alternative employment was not readily available.

The Return of National Security Threats

The problem is compounded by the return of national security threats. Without major geopolitical rivals, U.S. leaders believed they could minimize the importance of declining manufacturing activity.

But with China and Russia not only as trade threats but also as security threats, the Trump team believes there is an urgent need to renew the manufacturing base. If you don’t have the supply chains with which you can produce weapons and defense systems, you don’t have national security.

As President Donald Trump has argued, “if you don’t have steel, you don’t have a country.” Loss of trust in trading partners: While many economists fail to include such externalities in their analysis and therefore rely unconcernedly on trading partners and allies for such supply chains, the Trump camp does not share this trust.

Many of America’s allies and partners have significantly larger trade and investment flows with China than with America.

The Dollar as a Mechanism for Producing Trade Deficits

At this point, the persistent overvaluation of the dollar is the primary mechanism through which trade imbalances are produced, keeping imports stubbornly cheap despite widening trade deficits.

So how in this regime is it possible for foreign exchange markets, which are the largest markets in the world in terms of net trading volume, to balance?

The answer lies in the fact that there are (at least) two concepts of equilibrium for currencies.

1. One has its roots in economic models of international trade. In trade models, currencies adjust over the long term to balance international trade. If a country has a trade surplus over a fixed period, it receives foreign currency for its goods, which it then sells for domestic currency, pushing the domestic currency higher. This process occurs until its currency is strong enough that its exports fall and imports rise, balancing the trade balance.

2. The other concept of equilibrium is financial, and it comes from savers choosing alternative investments among different nations. In this concept of equilibrium, currencies are adjusted so that investors can indifferently diversify their portfolios across different currencies, on a pre-adjusted basis.

However, the latter class of models becomes more complicated when a nation’s currency is a reserve currency, as is America’s. Because America provides reserve assets to the world, there is a demand for dollars (USD) and U.S. Treasury securities (USTs) that does not reflect the balancing of bilateral trade or the optimization of (risk-adjusted) returns. These reserve assets serve to facilitate international trade and provide a vehicle for large pools of savings, often held for policy reasons (e.g., reserve or currency management or sovereign wealth funds) rather than to maximize returns.

Much (but not all) of the reserve demand for USD and USTs is inelastic. The bonds purchased to secure bilateral trade between Micronesia and Polynesia are purchased regardless of the US trade balance, either by the most recent jobs report or by the relative yield of US bonds against German bonds.

What is a Triffin world?

Such phenomena reflect what can be described as a “Triffin world,” according to the famous Belgian economist Robert Triffin. In this world, reserves are a form of global money supply, and the demand for them is a function of global trade and savings, not a function of the domestic trade balance or the performance characteristics of the reserve state. When the country holding the reserve currency is large relative to the rest of the world, it does not suffer significant externalities. The distance from the Triffin equilibrium to the trade balance is small.

However, when the country with the reserve currency is small relative to the rest of the world—say, because global growth exceeds the country’s growth for a long time—tensions increase and the distance between the two widens.

The gap between the Triffin equilibrium and the trade balance can become quite large. The demand for the reserve currency leads to a significant overvaluation of the reserve currency with real – disastrous – economic consequences.

Permanent current account deficits

In the Triffin world, the producer of reserve assets must suffer persistent current account deficits as the other side of the export of reserve assets. USTs (assets in that currency) become exported goods that feed the global trading system.

When exporting, the US receives new currency, which is then spent, usually on imported goods. The US suffers a large current account deficit not because it imports too much, but it imports too much because it must export USTs to provide reserve assets and facilitate global growth.

As US GDP as a percentage of world GDP shrinks, the current account or fiscal deficit that must be run to finance global trade and savings grows as the share of the domestic economy increases.

Therefore, as in the rest of the world, the consequences for domestic export sectors – an overvalued dollar that incentivizes imports – become more difficult to deal with and the damage done to this part of the economy increases.

Eventually (in theory), a Triffin “tipping point” is reached at which such deficits become large enough to pose a credit risk to the country holding the active reserve.

The debt crisis

The country with the reserve currency can lose this status, causing a wave of global instability, and this is referred to as the “Triffin dilemma”.

Indeed, the paradox of being a reserve currency is that it leads to permanent “twin deficits”, which in turn lead over time to an unsustainable accumulation of public and external debt which ultimately undermines the security and reserve currency of such a large debtor economy.

While the United States’ share of world GDP has halved from 40 percent of world GDP in the 1960s to 21 percent in 2012, and has recovered slightly to its current level of 26 percent, it is still a long way from such a turning point, in part because there are no meaningful alternatives to the dollar or the UST.

While countries like China aspire to reserve currency status, they do not meet any of these criteria. And while Europe can, its bond markets are fragmented, and its share of world GDP has shrunk even more than the United States’.

Tariff Rates – How Does the US Lose?

The backdrop to these monetary developments has been a system of tariff rates that define the international trading system that is, by and large, locked into a configuration designed for a different economic era.

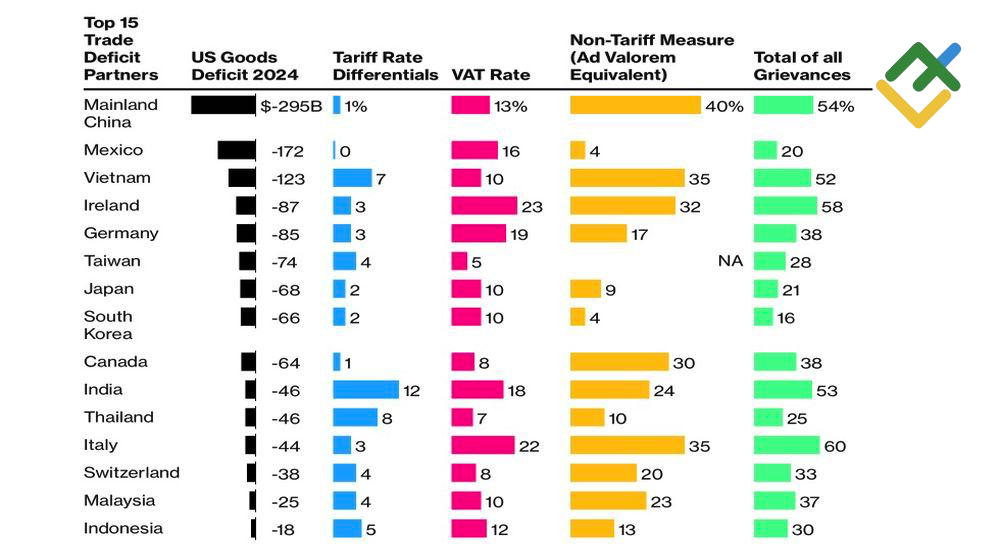

According to the World Trade Organization, the United States’ effective tariff on imports is the lowest in the world, at around 3%, while the European Union charges around 5% and China charges 10%. The figures are a weighted average across all imports and do not reflect bilateral tariff rates; bilateral differences can be much larger, for example the US charges only 2.5% on car imports from the EU, while Europe charges a 10% tariff on US car imports.

Legacy of Another Era – The Myths of the Strong Dollar

These tariffs are, to a large extent, a legacy of an era when the United States wanted to generously open its markets to the rest of the world on favorable terms to help rebuild after World War II or build alliances during the Cold War.

While we are probably a long way from the economic crises that are the turning point of the Triffin dilemma, we must nevertheless calculate the consequences of a Triffin world. The status of the state holding the world’s reserve currency comes with three main consequences: somewhat cheaper borrowing, a more expensive currency, and the ability to pursue security objectives through the financial system.

1. Cheaper Borrowing

Because there is a persistent reserve-based demand for UST securities, the United States may be able to borrow at lower rates than it would otherwise have.

Because economists have few variations to study (the United States has had the sole reserve currency for many decades), it is impossible to be confident about how large this benefit is. Some estimates, however fanciful, put it as large as 50-60 basis points of the borrowing rate (McKinsey, 2009). In any case, there are many countries that borrow much cheaper than the United States.

At the time, all G7 members borrowed cheaper than the United States, except the United Kingdom, which borrowed one-tenth of a percent more. Other peers like Switzerland and Sweden also borrow cheaper, Switzerland by almost 4 percentage points. Meanwhile, even a classic troubled borrower like Greece can borrow a bit cheaper.

The bottom line is that any benefit is likely to be tempered by things like central bank policy outlooks, growth and inflation, forecasts, and stock market performance.

However, the borrowing advantage can be understood differently: rather than reducing (overall) borrowing costs, it may reduce fluctuations in borrowing costs. In other words, the US is not borrowing much cheaper, but it can borrow more without pushing yields higher. This is a consequence of the price inelasticity of demand for reserve assets, while the other side of the mountain is that they have large external deficits to finance this reserve provision.

2. Richer Currency

The most important macroeconomic consequence of the US functioning as a global reserve producer is that demand for US assets pushes up the dollar, driving it to levels far greater than what international trade balance would have been in the long run.

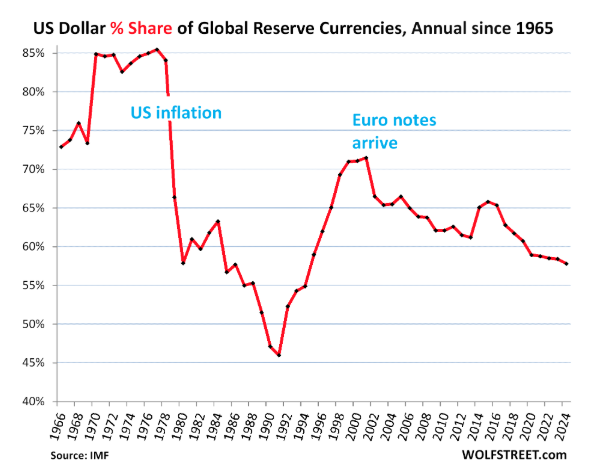

According to the IMF, there are about $12 trillion in official global foreign exchange reserves, of which about 60% is in dollars – in reality the amount of dollars held is much higher, as unofficial reserve assets in dollars.

Clearly, $7 trillion in demand is enough to move the needle in any market, even the foreign exchange markets.

$7 trillion is about a third of the U.S. M2 (money supply), flows that create or unwind these holdings would obviously have significant market consequences.

If trillions of dollars in securities purchased for Fed policy rather than investment purposes on the Fed’s balance sheet had any effect on financial markets, then trillions of dollars purchased for foreign central bank policies rather than investment purposes should also have some effect if they were on other countries’ balance sheets rather than the Fed’s balance sheets.

Because nations accumulate reserves in part to cushion pressures on their own currencies, there is a contemporary negative correlation between the exchange value of the dollar and the level of global reserves. Reserves tend to rise when the dollar falls, as countries buy dollars to lower the exchange rate of their currencies, and vice versa when the dollar rises.

Reserve Currency and Job Loss

However, except for two quarters in 1991, the United States has had a current account deficit since 1982.

The fact that the current account balance has not been in balance for a negligible period of more than half a century tells us that the dollar does not play a role in balancing international trade and income flows.

The interaction between the reserve status and manufacturing job losses is strongest during economic downturns. Because reserve assets are “safe,” the dollar appreciates during recessions. In contrast, other countries’ currencies tend to depreciate when they go through economic downturns.

This means that when aggregate demand falls in a downturn, the pain in export sectors is compounded by a sharp erosion of competitiveness.

Thus manufacturing employment falls sharply during a recession in the United States and then fails to recover substantially.

It may seem strange to assume that reserve demand for U.S. Treasury securities plays only a small role in achieving favorable lending terms but a major role in currency appreciation. However, this explanation is more consistent with the results in both interest rate markets and the balance of payments.

Indeed, it is also consistent with the idea that liquidity injections ultimately raise interest rates because they stimulate growth in nominal terms.

3. Economic Extraterritoriality (International Transactions)

Finally, if reserve assets are the lifeblood of global trade and financial systems, it means that whoever controls the reserve asset and currency can exercise some level of control over trade and financial transactions. That is, it allows the US to enforce its foreign and security policy will using economic power rather than military force.

The US can and does impose sanctions on states and individuals around the world in a variety of ways. From freezing assets to excluding states from the state and restricting access to the US banking and financial system that is critical for any foreign bank doing global business, the US exercises its economic power to achieve the foreign policy goals of weakened enemies without having to mobilize a single soldier.

Many previous reserve-providing nations had significant sea power due to their trading empires, which allowed them to block rival nations and hinder their economic production; sanctions achieve similar results, without the need for military action.

The erosion of competitiveness

Combining these properties of reserve assets, if there is persistent, price-inelastic demand for reserves but only modestly cheaper borrowing, then the US reserve currency status lends the weight of an overvalued currency that erodes export competitiveness, relative to geopolitical advantages.

Achieving core national security is aimed at minimal cost through economic extraterritoriality (a legal term for relations entered into outside a nation state). The trade-off is therefore between export competitiveness and the projection of financial power.

Because the projection of power is integral to the global security order that the US assumes, the issue of its reserve currency status must be understood as intertwined with national security.

This connection explains why President Trump believes that other nations exploit America in both defense and trade: our defense umbrella and our trade deficits are linked, through currency. In a Triffin world, this adjustment becomes more difficult as the United States shrinks as a share of global GDP and as a military power.

As the economic burden on America increases as global GDP surpasses American GDP, it becomes more difficult for the United States to ensure global security, because the current account deficit increases and its ability to do so decreases as the productive base becomes an empty shell. The growing international deficit is a problem because of the increasing burden on the American export sector and the socio-economic problems that flow from it.

Reshaping the Global System is Necessary

The dollar is the reserve asset largely because America provides stability, liquidity, market depth, and the rule of law.

These are related to the characteristics that make America strong enough to project physical power around the world and allow it to shape and defend the global international order.

The history of the intertwining of reserve currency and national security is long. In any potential reshaping of the global trading system, these connections will become increasingly clear. Both tariffs and monetary policy aim to improve the competitiveness of American manufacturing and thereby increase the productive capacity and distribution of aggregate demand and jobs within the international distribution.

These policies are unlikely to lead to a significant renewal of low-value-added industries such as textiles, for which other countries—such as Bangladesh—will maintain comparative advantage despite significant currency fluctuations or tariff rates.

However, these policies can help maintain the American advantage in producing high-value-added goods and deter further offshoring and potentially increase negotiating leverage in agreements by other countries to open their markets to American exports or protect intellectual property rights.

Moreover, because many in Trump’s camp see trade policy and national security as inextricably linked, they will pursue this tariff policy despite the pain it will cause. Many interventions will target security-critical industrial facilities, to the extent they can.

The term national security will likely become increasingly broad, for example to include products such as semiconductors and pharmaceuticals. Despite the dollar’s role in significantly burdening the U.S. manufacturing sector, President Donald Trump has shown the value he places on its status as the world’s reserve currency and has threatened to punish countries that move away from the dollar.

International trade policy will seek to recapture some of the benefit that reserve provision transfers to trading partners and link this economic burden-sharing to defense burden-sharing.

Although the Triffin results have hurt manufacturing, there will be efforts to improve the US position within the system without destroying the system. There is a risk of substantial adverse consequences for financial markets and the economy – but it is the birth of a new world. In short, welcome to the new world where the US is regaining its economic dominance.