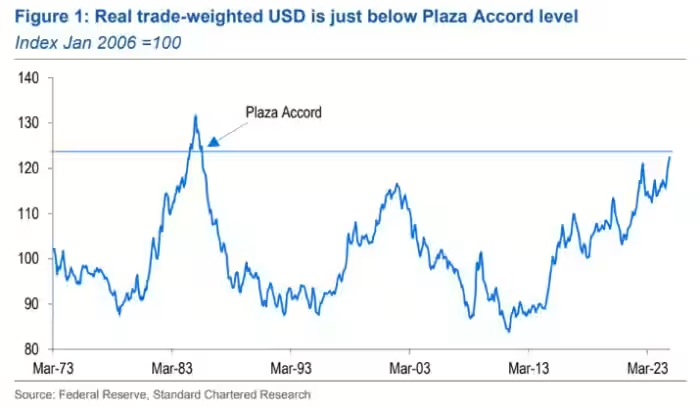

The successful Plaza Accord of the 1985s is now apparently serving as inspiration for the administration of US President Donald Trump, as it seeks ways to weaken the dollar with the ultimate goal of improving America’s trade balance.

While at the same time not wanting to weaken the dollar’s power as a reserve currency. Donald Trump and his team – notably Stephen Miran, the new chairman of the Council of Economic Advisers – would call the agreement the “Mar-a-Lago Accord”, as it would be signed at the president’s eponymous resort in Florida (we have reported on this proposal for restructuring the US debt in The Liberal Globe).

One could imagine a reasonable proposal for coordinated intervention among the major economies to weaken the dollar. The United States would take steps to reduce its budget deficit, and countries with large surpluses like Germany would increase theirs, thereby addressing the fundamental driver of today’s international trade imbalances. But the Mar-a-Lago Accord does no such thing—and therein lies the problem.

Instead, it is a vision that risks doing exactly what the Trump administration fears: damaging America’s ability to finance its deficits (and, in particular, to keep interest rates low) and undermining the status of the U.S. dollar as the world’s leading reserve currency.

- Let’s start with interest rates

A foreign central bank intervention to weaken the dollar’s exchange rate would reduce foreign holdings of U.S. Treasury bills. But the fall in demand for interest would lead to a fall in their prices and an increase in interest rates.

If we think about it this way: if the trade balance improves when the economy is at full capacity, the elements of domestic demand (household consumption and business investment) must be put on the back burner (and therefore we have a recession in economic activity), so the economy has an outflow of critical capital.

As for the dollar, its dethronement is, in a sense, an integral part of the vision that animates the Mar-a-Lago Agreement.

The first to use the term was the economist Zoltan Pozsar, who proposed a “Bretton Woods III” agreement that would replace the global monetary system based on the dollar with a system based on central bank digital currencies (CBDCs), along with gold or other commodities. According to Pozsar, the US government would strengthen its balance sheet by revaluing gold. But such an effort to devalue the dollar could well lead to its collapse as the dominant reserve currency—a process that would be accelerated if monetary easing by the US Federal Reserve was part of the deal.

While Trump has pushed for a more accommodative monetary policy, he has also made it clear that he wants to maintain the dollar’s global primacy, even if it means using tariffs to force countries (such as the BRICS economies) not to undermine it, Goldman Sachs and other investment banks have sounded the alarm about this trade war that would be costly for all sides. Of course, as Treasury Secretary Scott Bessent has noted, dollar depreciation and dollar dominance are not necessarily mutually exclusive.

In the late 1990s, for example, the dollar was both depreciating and representing a larger share of central bank foreign exchange reserves. But there is a clear contradiction between the two goals. If a Mar-a-Lago Accord discourages central banks from holding U.S. bonds, it is particularly difficult to see how the dollar’s global position will survive.

Free lending and fees

However, that is exactly what Miran seems prepared to do. He proposes requiring foreign central banks to hold 100-year US bonds with no coupon payments in place of the T-bills they currently hold. (This would be tantamount to restructuring the US debt, which is tantamount to default).

Alternative—or additional—provisions include the introduction of “user fees” charged to foreign central banks holding US debt and a more general tax on foreign investment in the US (reminiscent of the infamous Tobin tax on short-term currency market transactions proposed in the 1970s).

The Role of the Sovereign Wealth Fund

The sovereign wealth fund (SWF) that Trump has ordered created is apparently also supposed to play some unspecified role in the vision of the Mar-a-Lago deal.

It is not clear where the money for this SWF will come from. Like developing economies, the US would do well not to start a SWF that would have to borrow to finance the economy due to insufficient international reserves. It is also worth noting that SWFs work best when—unlike Trump’s proposed fund—they invest in foreign rather than domestic assets.

Even setting the Fund aside, this proposal is not based on reality.

- Why would the world’s central banks and other investors accept 100-year bonds—which would pay no interest for a century—in place of old bills?

- Why would they accept new fees and taxes on their U.S. debt or investments?

Trump may say the answer is simple: it can avoid punitive tariffs. But he has invoked this weapon so relentlessly—in the name of so many goals, with so many delays and reversals—that it is quickly losing its potency. Countries will not kneel, but they are already asking for ways out. If Trump pushes too hard, the leak may well turn into a mass flight from the dollar.

Efforts to leverage U.S. military and geopolitical power to force countries to accept the terms of the Mar-a-Lago agreement will prove equally ineffective.

Yes, in the 1960s, Germany agreed to cover the cost of stationing U.S. troops on its soil in order to preserve the Bretton Woods system. And in 1991, Kuwait and Saudi Arabia covered a large share of the U.S. costs of the Gulf War.

But there is a crucial difference between then and now: goodwill.

With his penchant for threats and coercion, his willingness to betray friends and allies, and his disregard for rules, Trump has systematically destroyed whatever international political capital he inherited, decimating US global leadership in the process.

The coercive Mar-a-Lago Accord—which harks back to the Roman Empire’s demand for a poll tax on the lands its legions occupied—would only hasten America’s decline.