Investors have been betting heavily on an artificial intelligence (AI)-driven future over the past two years, as technology stocks have led the S&P 500 index up 60%.

As of January 24, 2025, the cumulative market capitalization of Nvidia (NVDA) and other major AI infrastructure companies was nearly $16 trillion.

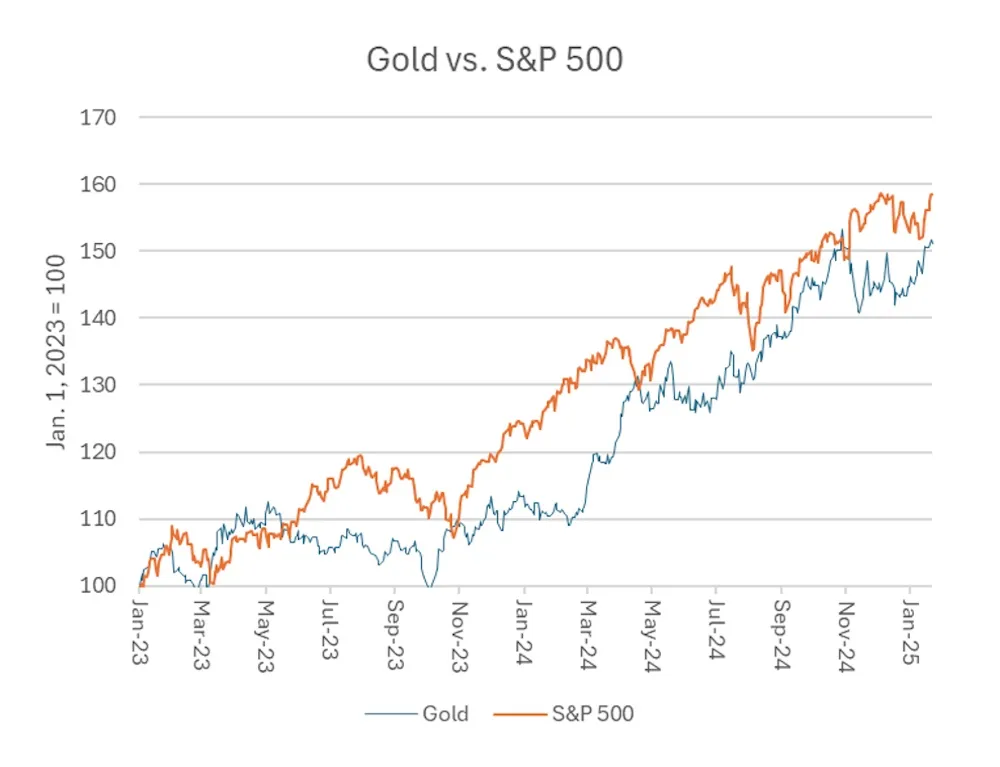

But there has also been a lot of speculation in the so-called “barbaric relic” of a monetary era that preceded the hegemony of the dollar, pushing the price of gold to historic highs.

In particular, gold has outperformed alternative hedging against the dollar by a huge margin.

Why would anyone take protectionist measures amid explosive tech-driven optimism?

The answer is that a lot could go wrong — lead to disaster, in fact.

Technology stocks are now the primary asset in the dollar-based global monetary system. Wall Street is in full swing while the economy falters – The Great Paradox!

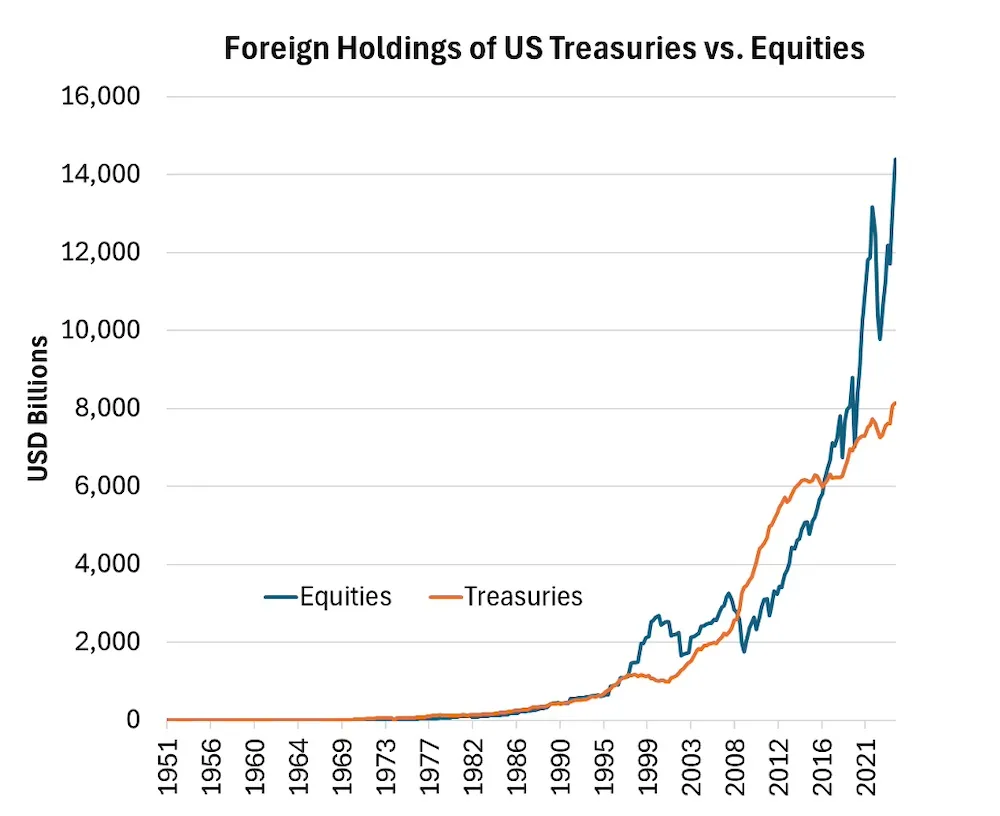

The United States has sold $24 trillion more in assets to foreigners than foreigners have sold to Americans.

This “net international position deficit” of $24 trillion, up from $18 trillion at the end of Donald Trump’s first term, has offset America’s cumulative trade deficit over the past 30 years.

For the past 10 years, foreigners have been buying stocks instead of U.S. Treasury bonds, as they did in the past.

Foreign central banks hold less U.S. government debt now than they did five years ago. If the tech boom turns out to be a bubble, it will drag the dollar down with it.

The race for market share in artificial intelligence could dictate the fate of the U.S. currency. If, for example, DeepSeek, China’s open-source technology outperforms ChatGPT and other American large language models (LLMs), tech stocks could send the dollar and the American economy into a tailspin.

There are many ways to hedge against the dollar. Few of them are attractive.

A 6% to 7% U.S. budget deficit without war or recession, as incoming Treasury Secretary Scott Bessent told Congress last week, is unprecedented in history.

But the dollar’s status as a reserve currency means America will be the first to suffer the consequences.

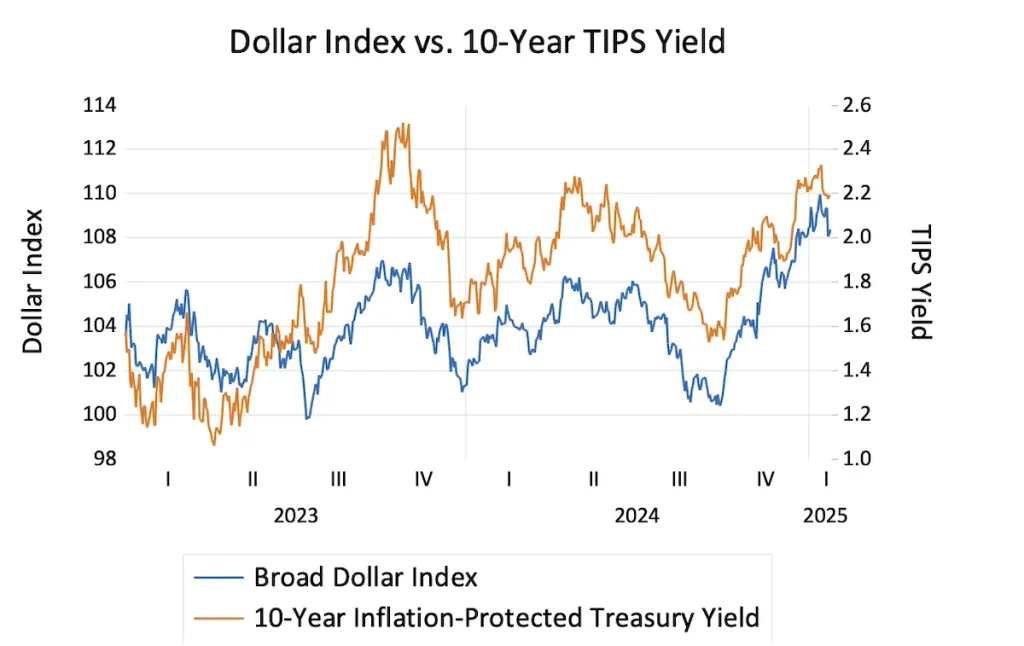

Buying Treasury bonds linked to inflation (TIPS) — in part because of expectations of a higher U.S. deficit under Trump — has pushed the dollar higher against all major currencies.

If U.S. inflation rises, so will interest rates, and the dollar’s exchange rate will rise against other currencies, even as the dollar loses value.

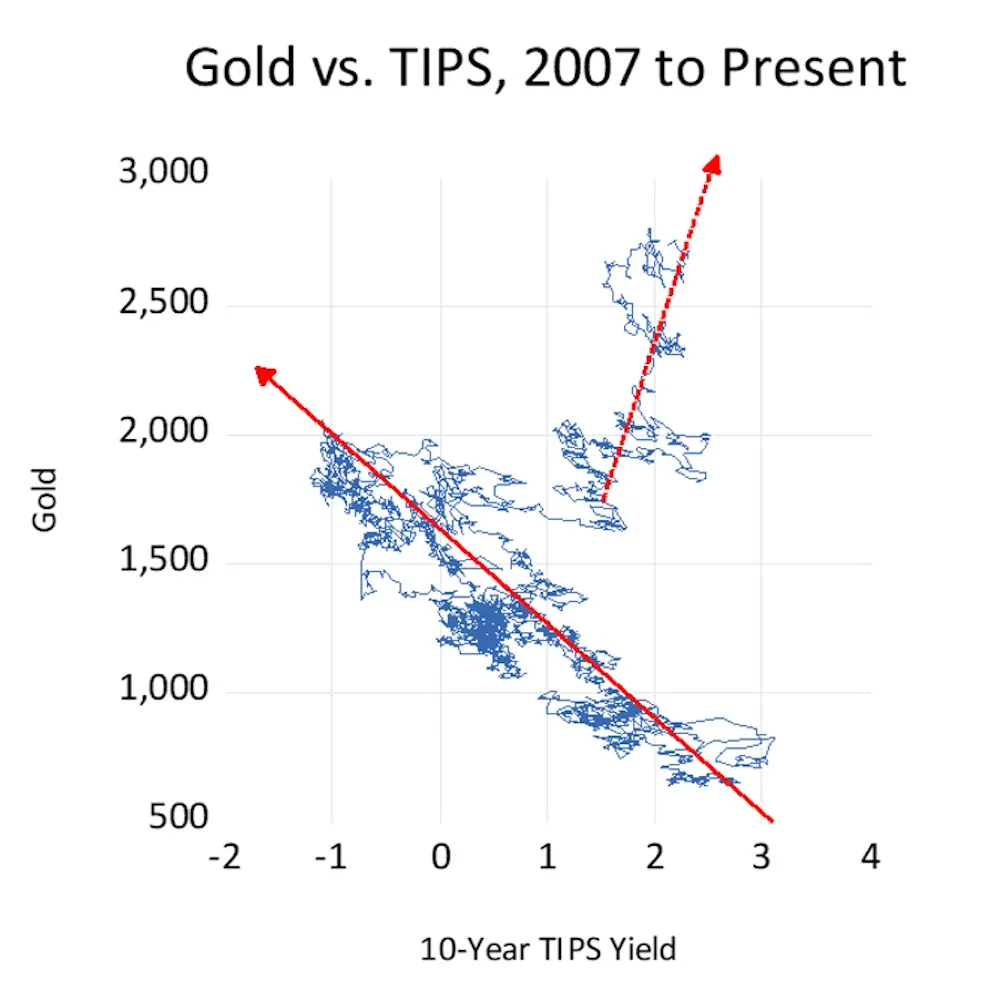

However, even as all currencies plunged against the dollar in response to rising “real” bond yields (based on inflation), gold rose, breaking a pattern that prevailed from 2007 to 2022.

The break in the long-term relationship between TIPS* bonds and gold coincided with the seizure of Russian foreign exchange reserves in March 2022 by the US and its allies.

China, Saudi Arabia, India and other central banks have gradually shifted their reserves from bonds to gold.

On paper, TIPS and gold offer similar returns: If the dollar and inflation in the US rise, both assets will increase in value.

The difference is that the Treasury cannot seize gold in a central bank’s vault the way it can seize central bank liabilities.

As much as 80 basis points (0.8%) of the increase in TIPS yields over the past six months can be attributed to sales of US bonds by foreign central banks. A group of hedge funds have followed central banks in investing in gold.

One positive is the change in the relationship between the price of physical gold and options. Implied volatility is a measure of the cost of gold options and, under normal circumstances, it decreases as the price of gold increases.

This is because gold mining companies have been the largest buyers of gold options. When the price of gold falls, they buy options to lock in their profits, and vice versa.

But in 2024, something new happened: The cost of gold options increased along with the price of gold.

The cost of gold options (implied volatility) is trading at a two-year high, while hedging costs are falling in other markets.

The virtue of gold is that its value is independent of the will of any government: It is the monetary asset of last resort, the medium of exchange that will be accepted if all else fails.

With few exceptions, the debt of almost all major economies has increased alarmingly relative to economic output over the past decade.

President Trump is walking a tightrope, trying to stimulate economic growth through tax cuts while facing a budget deficit of historic proportions in a peacetime, non-recessionary era. Gold’s outperformance warns us of how dangerous this is.

*TIPS bonds represent low-risk investment products that are tied to a low-interest-rate environment but are protected against inflation. This is because the United States government issues the bonds and guarantees at least the return of the principal to the investor. While the interest rate on TIPS, or Treasury Inflation-Protected Securities, bonds is locked in for the life of the bond, the principal amount increases with inflation and decreases with deflation.

Very good info can be found on website.