Global economic activity and the financial system as a whole are heading for an uncontrollable catastrophe, amid heightened geopolitical risk. The current downturn does not bode well for 2025 and beyond. Two global crises will dominate for at least several years, and possibly decades.

Economic crisis

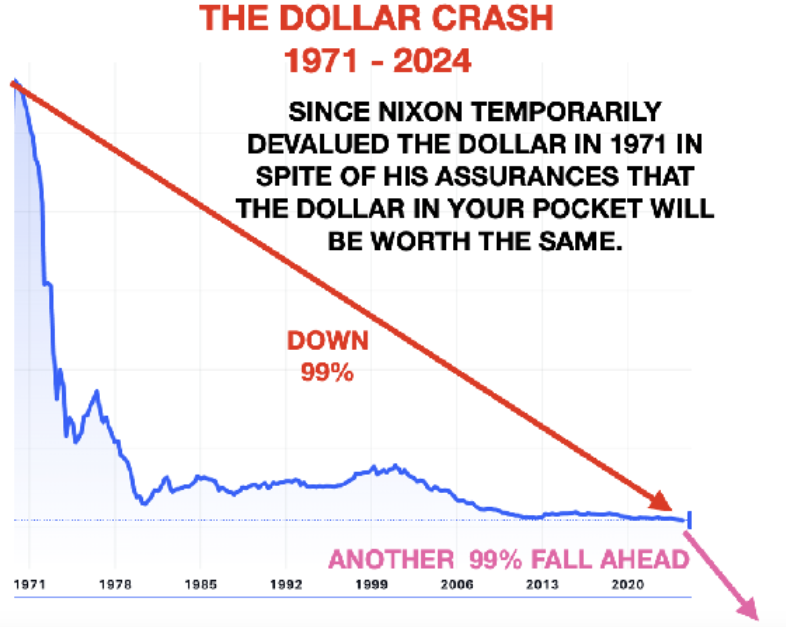

The first crisis concerns the end of the current monetary era, especially in the West. The exponential growth of debt, which we have been experiencing since 1971, when Nixon closed the gold window, reaches a superexponential phase in the current century, with uncontrolled deficits and debt.

The likely development of events will be as follows:

- unlimited printing of money to deal with any uncontrolled debt crisis.

- However, this will lead to currency devaluation,

- high inflation or hyperinflation, which will eventually turn into a deflationary collapse of the financial system and recession.

There is no clearer indication of the end of an economic era than when the reference currency loses 99% of its value.

A possible alternative would be for the financial system to collapse before the money printing takes effect, with a subsequent deflationary collapse. This would mean a period without functioning banks and money.

Since this is the outcome of every monetary system in history, without exception, anyone who doubts this inevitable outcome is mistaken. It is only a matter of time, not probability.

As the Austrian economist Von Mises said: “Every economic crisis in history has always been accompanied by political or geopolitical turmoil.”

When a country is spending money it does not have, starting a war is the most convenient way to create new money, which, of course, has zero intrinsic value. Expanding credit or printing money does not create economic value but buys time. Printing money also buys votes. Re-election is the primary goal of every government in a democratic system.

Successive U.S. administrations have increased the federal debt almost every year since the 1930s. The current deficit exceeds $2 trillion, while tax revenues are just $5 trillion. With federal spending exceeding $7 trillion, the U.S. government needs to borrow an additional 40% ($2T) to make ends meet.

In November 2016, when Trump was elected as the 45th President of the United States, the debt Trump inherited ($20 trillion) would reach $40 trillion by early 2025.

It wasn’t a difficult prediction: Since 1981, the U.S. debt has, on average, doubled every 8 years. Well, the debt probably won’t reach $40T by January 20, 2025, but it did increase by $16T instead of the projected $20T. More importantly, as the chart below shows, the debt has increased 44 times since 1981, while tax revenue has only increased 6 times, reaching $4.9T.

Can anyone explain how this debt will be repaid? The usual answer is that governments do not have to repay their debt.

So, let us turn again to history, such a useful empirical tool. Throughout history, a country that has not repaid its debts has, without exception, defaulted and its currency has been reduced to zero. No one should think that this time will be any different! A currency crisis at the end of a long cycle leads to economic collapse, poverty and misery.

However, the current financial cycle is already developing in parallel with a geopolitical crisis of such magnitude and scale that it could be greater than those of World Wars I and II.

Geopolitical Crisis

Financial and geopolitical conflicts are clearly linked. As in many armed conflicts, the United States has been involved since World War II, even though the country is not directly threatened. This has been the case in Vietnam, Afghanistan, Iraq, Libya, Syria, and Ukraine.

Most of these conflicts are related to the fear of losing US hegemony. The US government has adopted Mackinder’s 1904 theory that whoever controls the “Heartland” controls the world. The “Heartland” includes the region of Eastern Europe to the Yangtze River in the east and the Himalayas in the south. This region has enormous natural resources.

Syria seems to have recently fallen to Turkish-backed opposition groups in an offensive supported by the US military. Interestingly, the latest conflict began on the same day as the ceasefire between Israel and Lebanon. Obviously, this is no coincidence.

Thus, Turkey, which for some time balanced between Russia and the US, seems to have finally sided with the US. Turkey is a member of NATO and a candidate for membership in the BRICS, which includes Russia, China, Iran and India. With Turkey now on the side of the US and against Russia, we are seeing the first military conflict between the West and the BRICS.

No one knows whether Syria will re-align with Assad in Moscow. For the Russia-Iran axis, Syria is strategically crucial. But Russia cannot win this war with air power alone and probably does not want to divert resources from Ukraine. So we have yet another crisis in the Middle East, a situation with serious consequences for the region and the world.

It is likely that we will see the war in Syria continue, with anarchy and the rise of more jihadist groups. At best, Syrian factions will fight for dominance through local conflicts. At worst, the collapse will lead to a new period of generalized war, where factions will target civilians. As happened with Libya.

It is likely that more Syrians will become homeless and migrate to Europe and the United States. As we know, no Western country has the capacity to care for these people, so another humanitarian disaster is hitting the world.

The loss of access to Syria and the Mediterranean has weakened Iran, which will look for other options. There has always been a risk that Iran would block the Strait of Hormuz, which carries 24% of the world’s oil. The US could not prevent this. It would lead to a doubling or more in oil prices and a major global recession.

The United Arab Emirates (UAE), which includes Dubai, is located right next to the Strait of Hormuz. It is no wonder that so many people are moving to and investing in Dubai, given the high geopolitical risk that this region poses.

The world is facing a serious cycle of wars, which, at best, will involve unresolved and intractable wars in the Middle East and Eastern Europe involving both the US and Russia. At worst, it will lead to a nuclear war.

The conflict in Ukraine is a war that Russia is very unlikely to lose. Neither the US nor the European NATO forces have the resources to win a war with physical ground forces.

Russian missiles are currently superior, but anything can happen in a nuclear conflict. In a nuclear war, there is no winner, and it could mean the end of the world, so it is not worth speculating about the outcome of such a war.

Right now, the world, and especially the West, is on a path of geopolitical and economic disaster. No one knows how this will end. Even if it takes years, the world is unlikely to be the same once these two cycles have completed their course.

The end of the current economic cycle will be disastrous for the world, but bearable compared to the worst outcome of the war cycle. There was hope that Trump would resolve the Ukrainian situation, if the US neocons did not manage to seriously escalate it before January 20.

However, the conflict in the Middle East, with the involvement of Iran, makes the situation much more complicated, even with Trump’s best intentions. We always believe in finding solutions, but it is difficult to be optimistic when the two Vicious Cycles prevail.

At the very least, anyone with savings should take steps to protect them from the impending collapse of financial assets.

Markets

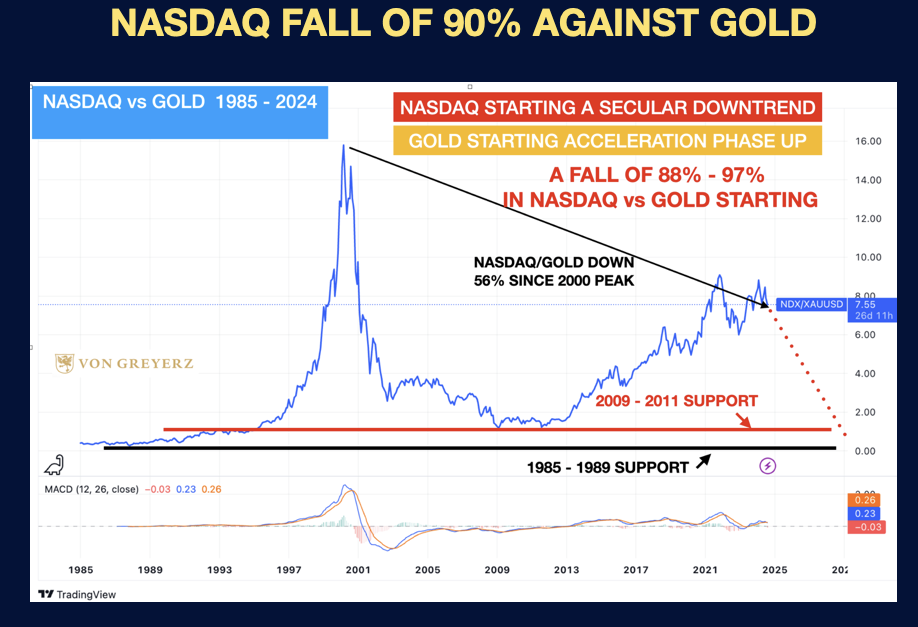

U.S. stocks are wildly overvalued.

The Buffett Index, U.S. stocks to GDP, is at an all-time high of 208%. A normal correction would require a 50% to 75% decline.

The price-to-earnings ratio for Nasdaq stocks is 49 times. A decline of at least 80%, like in the early 2000s, is likely.

Of course, bubbles can always get bigger before they burst. However, the risk of a market crash in the coming months is extremely high.

Inflation will rise rapidly, as will interest rates, due to money printing. The 10-year US Treasury yield will well exceed 10%, as in the 1970s.