As incomes have collapsed and food prices have soared, more and more Americans are borrowing to meet basic nutritional needs.

Last year, about 15 million consumers — or 6.5% of the U.S. population — reported using BNPL loans to pay the grocery bill or manage their weekly food expenses, according to research by PYMNTS Intelligence (New reality Check: The Paycheck-To-paycheck report) are, about 5.4% of the households that used BNPL loans to buy groceries were low-income – indicating that the crisis and the middle income classes are beginning to be affected.

That means there is a small share of higher earners, those who made more than $100,000 a year, using the popular pay-in-4 installment loans to buy food each month.

The trend may intensify this year as consumers in all income groups continue to face rising prices – evidence that inflation is ignoring the Fed’s measures.

Sacrifices…. in the food

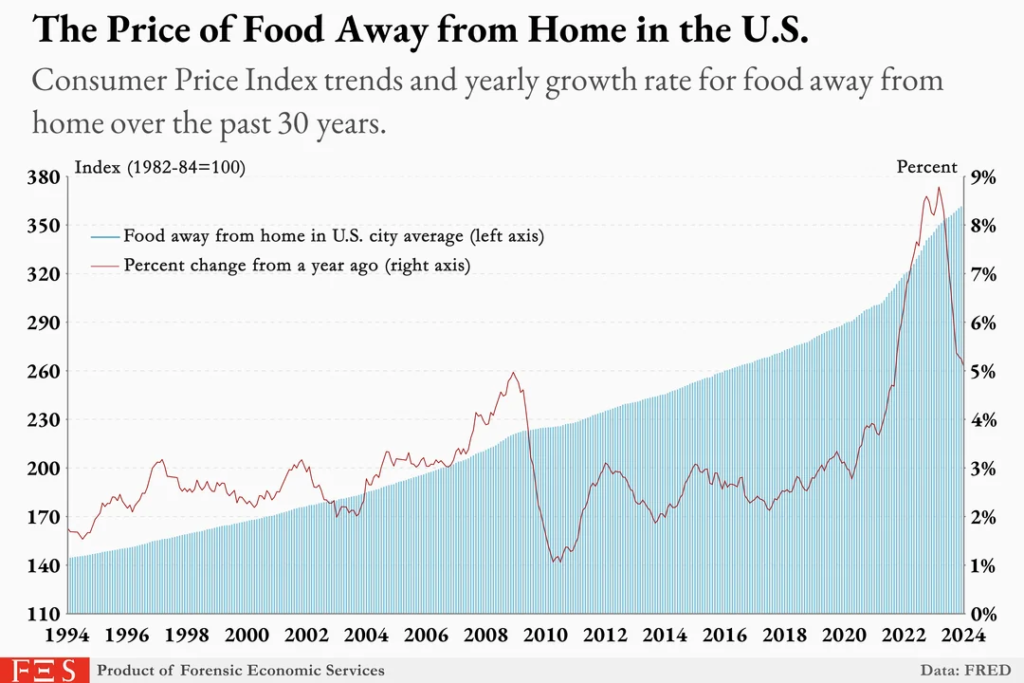

BNPL loans offer a short-term solution, allowing buyers to spread payments over time. However, while food prices moderated in February, they remain 22.3% higher than 2020 levels.

Rising costs have forced households at every income level to make sacrifices. For example, half of consumers earning more than $100,000 said they cut back on unnecessary spending at the grocery store.

More than 60% of those earning less than $100,000 a year said they had to cut back on spending because of high food costs. To save money, more people said they turned to discount stores.

Others decided to buy lower quality foods such as non-organic products for more affordable options. Even enjoying a meal at a restaurant has become more expensive. On an annual basis, the non-home food inflation index rose 4.5% in February.

But not everyone uses BNPL, making big food chains like McDonald’s think about it in order to lure consumers.

90% of McDonald’s restaurants in the U.S. offered breakfast or meal packages priced under $4. McDonald’s plans to offer even more deals this year to attract consumers, especially those hit hardest by inflation.

One third of high earners live paycheck to paycheck

In January, more than half of Americans said they were living paycheck to paycheck — meaning they have no savings — a sign that the rising cost of living may be affecting consumers’ financial stability, according to a report by PYMNTS Intelligence.

The share of those living paycheck to paycheck spans income brackets and generations. At least three-quarters of those earning less than $50,000 a year and about two-thirds of middle earners — earning between $50,000 and $100,000 — were living paycheck to paycheck in January.

Add to that the 36% making more than $200,000 who said they struggled to make ends meet. Those who did not use BNPL loans relied on credit cards to pay bills for food expenses.

A third of all U.S. consumers, 31 percent, said they used a traditional credit card to buy groceries in February, according to data from PYMNTS.

BNPL is a ‘double-edged sword’

While getting a short-term payday loan in four installments to buy groceries may seem convenient, borrowers should be careful not to over-rely on this type of lending.

- There is the risk of excessive expenses and non-satisfaction of multiple loan claims.

- While BNPL is generally interest free for smaller purchases, you could be charged interest for larger loans. Although BNPLs are not a regulated market, late payments can seriously affect creditworthiness.

BNPLs are a double-edged sword that can quickly backfire if not used properly.