Investors are now selling dollars in droves as the market estimates that the US Federal Reserve has completed its most aggressive interest rate hikes in years and will begin tapering next year in 2024.

In particular, asset managers are expected to sell 1.6% of open dollar positions this month, the biggest monthly outflow since last November, according to State Street, which is a custodian of $40 trillion in assets. After weaker-than-expected US jobs data on November 3, fund managers have been selling “significantly” every day, according to the bank.

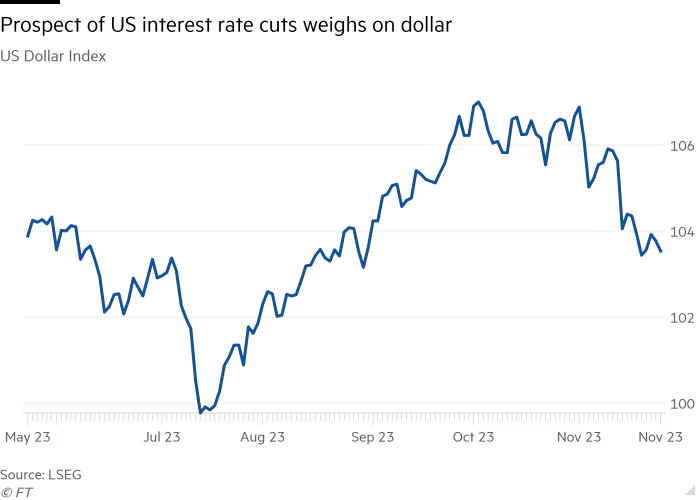

As a result, the US currency is on track for its worst monthly performance in 2023, with analysts warning that the sell-off could just be the start of a longer-term trend among investors to steadily reduce their exposure to US assets. Flows over the past two weeks point to a rapid revision in demand for the dollar at hand. The recent selloff marks the unwinding of an unusually large position in the US dollar. Investors believe that if rate cuts happen, then they don’t need to hold as many dollars.

According to State Street, in the past two decades there have been only six such rapid declines in dollar reserves. The most recent occurred in November last year, when the dollar index, a measure of the US currency’s strength against a basket of six currencies, weakened by about 10% by the end of January.

Despite the recent easing, asset managers were still overweight the dollar against other currencies, a sign that dollar weakness could continue.

The dollar experienced a huge rally last year on the back of the Fed’s rate hikes. The dollar index had risen as much as 19% by the end of September, delivering big gains to long hedge funds, before weakening sharply in the fourth quarter. It rose more than 7 percent this year between July and October as strong economic data pushed U.S. borrowing costs to a 16-year high and convinced investors that interest rates will stay higher for longer.

But the narrative has changed again in recent weeks.

US inflation fell more than expected in October to 3.2%, prompting investors to reconsider any prospect of further rate hikes. Recent weakness has left the dollar roughly where it started this year, and futures markets are now discounting rate cuts of 0.5 percentage points by September next year.

They were selling dollars at the fastest pace this year

Over the past 20 days, investors have been selling dollars at the fastest pace this year, turning to the Japanese yen, the Canadian dollar and a host of Latin American currencies. The dollar sell-off is welcome news for Japan’s finance ministry, which is on alert for possible currency intervention as the yen trades near a 33-year low against the dollar, adding to inflationary pressures by raising the cost of imported goods.

And while the yen has fallen about 12% against the dollar this year, November offered some respite with the currency strengthening about 1.5%. The yen’s strength is expected to continue, with the Bank of Japan abandoning negative interest rate policy in the coming months. It doesn’t make much sense for the yen to be low (betting on a falling price) as any BOJ policy meeting will be a live event.

The dollar’s weakness is also a relief for emerging markets as it makes it easier for them to repay dollar-denominated loans and is expected to be a strong reason for investors to return to developing economies after heavy sales of hard-currency debt this year.

There are many overweights in emerging market stocks and commodities. A weaker dollar is unraveling some of the very narrow bullish cases for US stocks.

MSCI’s index of emerging-market shares has added 3 percent so far this year, well behind a 19 percent gain for the U.S. S&P 500 index of blue-chip shares.

Heading into 2024 the dollar’s weakness will continue in part because less turbulence is expected between the US and China, meaning investors had less need for the greenback as a safe haven. However, since the start of the Russia-Ukraine war, something has broken in the usual investment rotation between developed and emerging markets, noting that the preference for stocks in Mexico and Brazil is partly due to the perception that these countries are in a good political position. We’re seeing a lot of interest in emerging markets – but these two forces, the weaker dollar and geopolitical concerns, are a bit at odds.