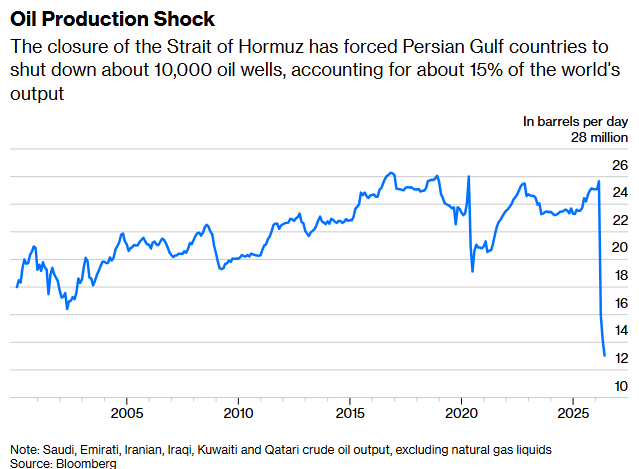

Approximately, 20 million barrels of oil and condensate pass through the Strait of Hormuz every day, an amount that corresponds to almost 20% of global consumption. At the same time, approximately 25%-30% of the world’s liquefied natural gas (LNG) trade is transported through the same sea route, making the region the most important energy hub on the planet.

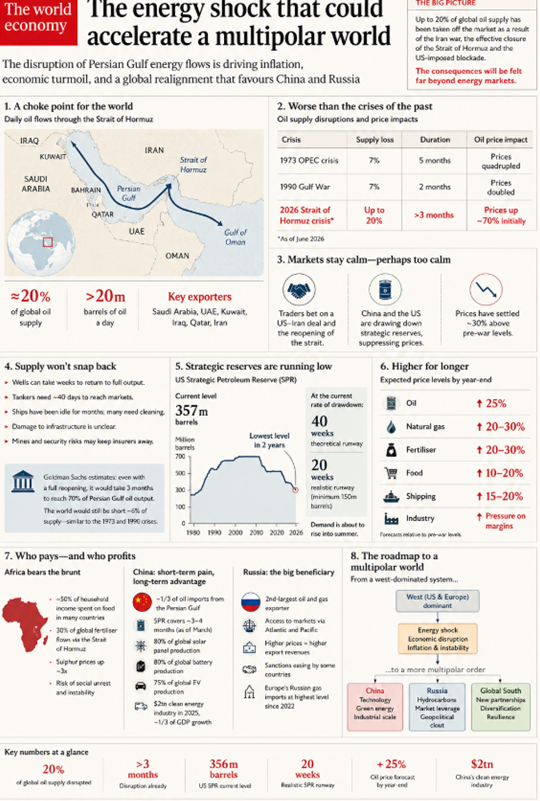

With Iran controlling the Strait of Hormuz and the United States effectively imposing a blockade on the Persian Gulf, up to a fifth of the world’s oil supply has been taken off the market.

Even if shipping were to restart tomorrow, the damage has already been done. Strategic reserves are being depleted, supply chains have been disrupted, and oil production cannot simply be restored to previous levels overnight. The losers will be many and the winners few.

Much of the world is facing a new wave of inflation, economic stagnation, and social unrest.

According to estimates by Trust Economics, every $10 increase in the price of oil removes 0.1 to 0.3 percentage points from global growth and adds up to 0.4 percentage points to inflation in advanced economies.

Africa is expected to be hit hardest, as fertilizer shortages push food prices higher and exacerbate already existing vulnerabilities.

China and Russia are the countries that seem to benefit the most. China is the world’s largest oil importer and will face difficulties in the short term. However, it is also the world’s largest producer of green energy technologies and its exports are being boosted by the oil crisis.

Russia, for its part, is the third largest oil producer and the second largest exporter. By having what the rest of the world needs, it can use its bargaining power to achieve an easing of sanctions and a reduction in international support for Ukraine.

The Illusion of Stability

The war waged by the United States and Israel against Iran has caused the most serious oil crisis in modern history.

- During the OPEC oil crisis of 1973 and during the Gulf War, about 7% of the world’s oil supply was taken off the market for five and two months, respectively.

- In the case of the Iran war, up to 20% of the world’s supply has been lost for more than three months.

The surprise is not the size of the disruption, but the composure that markets continue to display. During the OPEC crisis, oil prices quadrupled, while during the Gulf War they doubled.

The Iran war initially drove prices almost 70% higher than pre-war levels, but they have since stabilized at about 30% above them. Today, every $1 increase in the price of Brent translates into an additional cost of about $35 billion per year for oil-importing countries.

For the European Union, which imports more than 95% of its crude oil needs, a prolonged price increase could increase its energy costs by tens of billions of euros per year.

For months, US President Donald Trump has been promising a permanent ceasefire and the reopening of the Strait of Hormuz. At the same time, China has spent years preparing for the possibility of a major conflict in West Asia, significantly increasing its strategic oil reserves.

Today, it is using these reserves instead of buying oil on international markets, reducing imports to their lowest levels in almost a decade and helping to contain prices. The United States is also following a similar strategy.

The past three weeks have been the largest drawdown of the US strategic oil reserves in US history. But markets are not operating in a perfectly rational manner.

Traders and analysts are betting that Washington and Tehran will eventually reach a deal and supply will return to normal.

Few are willing to bet on long-term high prices, only to see a diplomatic development reverse their positions. This optimism may benefit consumers in the short term, but it could make the eventual adjustment even more painful.

Higher prices would encourage energy conservation and force governments to take emergency measures. Instead, consumption has remained largely unchanged, despite the loss of 20% of global oil supply.

Oil Supply Not Recovering Because War Stops

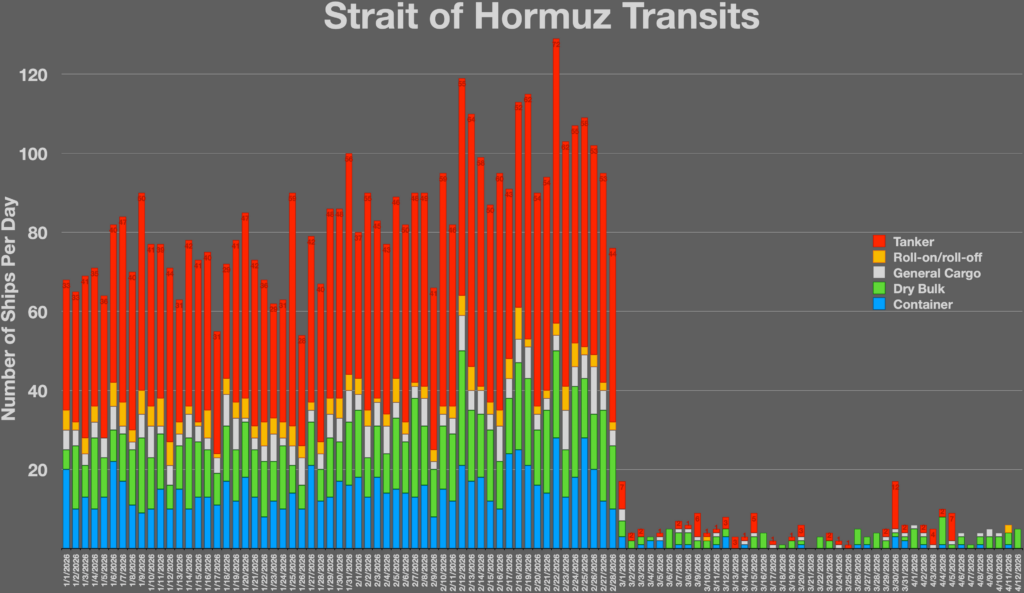

Even in the most optimistic scenario, the energy crisis is far from over. The reopening of the Strait of Hormuz would not immediately restore oil flows.

- Wells that have stopped operating can take weeks to return to full production capacity.

- Tankers leaving the Persian Gulf take about 40 days to reach their destinations, and recent reports indicate even longer delays.

- Many ships have been stranded for months in shallow waters, becoming covered in marine organisms that reduce their performance and require cleaning before they can return to normal operation.

- The extent of damage to oil infrastructure also remains unclear.

- Equally uncertain is whether shipping companies and insurers will be willing to operate in a sea area that may remain mined.

For all these reasons, Trust Economics estimates that even if the Strait of Hormuz were fully reopened, it would take about three to four months for 70% of Persian Gulf oil production to be restored.

Even then, the global market would still be short of about 6% of its supply – a figure comparable to that of the 1973 and 1990 oil crises.

Strategic Oil Reserves

Strategic reserves are not inexhaustible. The strategic oil reserves have helped to absorb some of the shocks. However, this cannot continue indefinitely.

The US strategic reserves are already at their lowest level in two years. In the coming days, they are expected to fall to their lowest level since the 1970s, when they were first built.

The US currently has about 357 million barrels of oil in its strategic reserves, and the three largest releases in its history have occurred in the past three weeks.

At the current rate, the reserves are theoretically enough for another 40 weeks. In practice, however, they cannot be depleted.

The oil is stored in underground salt caverns, and pumping it out too quickly risks collapsing the facilities.

Realistically, the reserves could be reduced to about 150 million barrels, which leaves only 20 weeks of supply — just before the summer season, when demand for fuel peaks.

For this reason, it is estimated that prices at the end of the year will remain 25% higher than pre-war levels. Similar increases are expected for natural gas and fertilizers.

The world is unlikely to see a return to cheap goods and low energy costs anytime soon.

Who pays the cost and who benefits?

“Strait of Hormuz closure risks greatest global energy supply shock in decades,” says a report by Wood Mackenzie. The firm estimates that if the disruptions continue for another four months, the global economy will enter a recession. The impact, however, will not be the same for everyone.

Africa

Africa is expected to be hit hardest. In many African countries, almost half of household income already goes to food.

Fossil fuels are a key raw material for fertilizer production, and about 30% of global fertilizer flows pass through the Strait of Hormuz. Farmers are already cutting back on production as sulfur prices have tripled.

The experience of 2007-2008 is a reminder of the dangers: soaring food prices triggered mass protests and riots in countries such as Burkina Faso, Cameroon, Ivory Coast, Morocco, Mozambique, Senegal and Tunisia, and even led to a general strike in Egypt.

China

China faces short-term difficulties as about a third of its oil imports come from the Persian Gulf.

The country imports more than 11 million barrels of crude oil per day, and has strategic reserves estimated to cover more than 90 days of net imports. However, it has significant advantages that most countries do not have.

It produces about 80% of the world’s solar panels, 80% of its batteries and 75% of its electric vehicles. China’s clean energy industry is valued at about $2 trillion and accounted for a third of the country’s economic growth in 2025.

China’s investment in the “green” economy exceeded $800 billion in 2025, while Chinese companies dominate the supply chains of critical minerals and energy transition technologies. The rise in green technology exports not only boosts its revenues but also its position as a provider of energy security in an unstable world.

Russia

Russia, however, may prove to be the biggest winner. As the world’s second-largest exporter of oil and gas, it has the ability to supply markets across both the Atlantic and Pacific oceans.

Every $10 increase in the price of oil translates into billions in additional revenue for the Russian budget. By 2025, oil and gas revenues accounted for about a third of the country’s total government revenue.

When oil prices skyrocketed in 2007, Russia experienced its second-highest growth rate since the breakup of the Soviet Union. Now, more and more countries are looking to Moscow to secure energy supplies and keep costs down.

Britain and the United States have already eased some restrictions on Russian oil imports, while India is steadily strengthening its cooperation with Russia in areas such as shipbuilding and labor mobility. Even in Europe, Russian gas imports are at their highest levels since 2022.

Europe under pressure: Inflation or recession?

The European Union is among the biggest losers in the crisis. Industry in Germany, Italy and France remains particularly vulnerable to rising energy prices, while the European Central Bank risks being faced with a difficult dilemma: higher inflation or weaker growth.

The phenomenon of stagflation — low growth and persistently high inflation — that marked the 1970s is resurfacing as one of the biggest risks to the European economy.

The new crisis after the crisis

The significance of the current crisis goes far beyond the energy market. Even in the most favorable scenario, higher prices, raw material shortages and disruptions to economic activity have now been embedded in the global economy for many months.

The countries that appear best prepared to withstand the shock are not necessarily those that dominated the previous era of globalization. China has energy alternatives, industrial power, and technological scale.

Russia remains one of the few powers that can supply the world with the hydrocarbons on which it still depends.

Across Africa and the wider Global South, governments may be forced to seek new partners outside the Western sphere of influence as economic pressures intensify.

Beyond the geopolitical dimension, the crisis in the Strait of Hormuz represents a massive redistribution of global wealth.

Energy importers—Europe, Japan, South Korea, and much of Africa—will see their trade deficits widen.

In contrast, hydrocarbon exporters, led by Russia but also countries such as Saudi Arabia, the United Arab Emirates and Qatar, will reap hundreds of billions of dollars in surplus revenues.

The energy crisis is not just a disruption in the markets. It is a mechanism for transferring economic and geopolitical power from the West to Eurasia, accelerating the emergence of a multipolar international order.