The hopes of European investors who abandoned their continent’s markets and turned to the United States are ultimately proving unfounded, while wealthy Americans are abandoning American assets.

The main slogan of the 47th US president, Donald Trump, was the well-known MAGA — “Make America Great Again.” At the core of this strategy was the pursuit of restoring the American economy to its former global dominance.

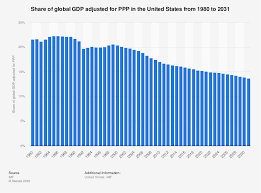

At the end of 2025, the United States’ share of global GDP was estimated to be 14.65%.

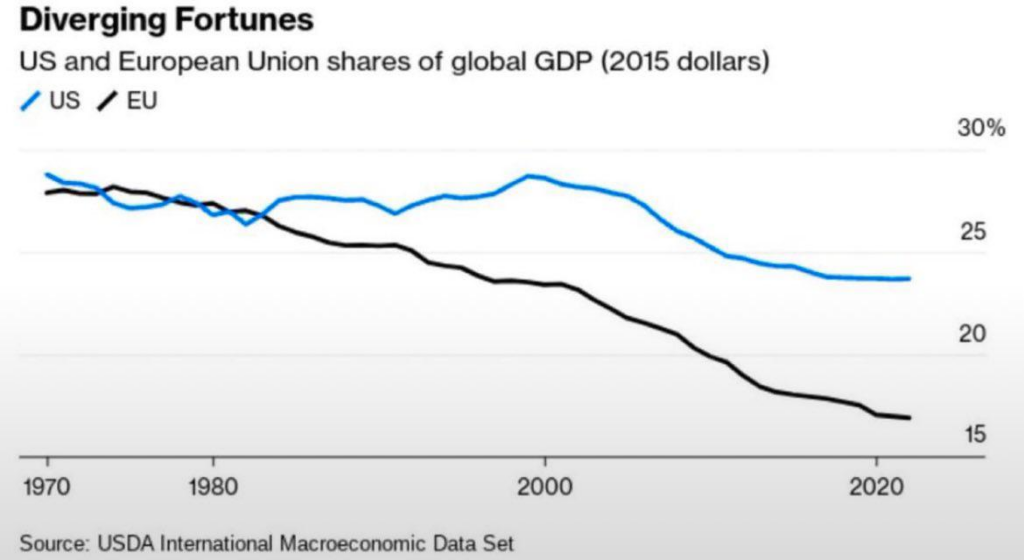

Forty years earlier, in 1985, the corresponding figure was 35.32%, while in the early post-war years the US produced more than half of the world’s GDP. Despite its strong image, the United States’ position in the global economy has been steadily weakening for decades.

Donald Trump attempted to reverse this course through a series of radical economic interventions. The central axis of his policy was the imposition of high retaliatory tariffs, with the aim of protecting the domestic market from foreign competition and restarting industrial production within the US.

At the same time, the US president believed that the creation of a strong protective wall around the US economy would encourage both foreign and American investors to restore productive activities within the country.

He repeatedly sent a message to international businesses saying: “Move your production to the United States and the tariff rate will be zero.”

Capital Inflows and the Tariff War

According to data from the US Treasury Department, net foreign investors’ holdings of long-term US assets amounted to $1.55 trillion in 2025, up about 31% from $1.18 trillion in 2024.

The largest net capital inflow came from Europe, reaching $872.8 billion. European investors were affected by both US trade protectionism and the continuing deterioration of the economic situation in the European economy.

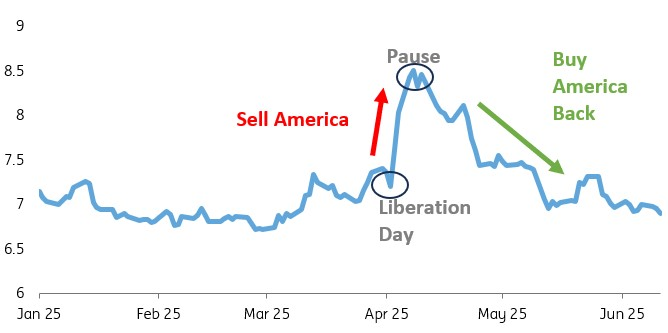

However, this trend now seems to be reversing. The slogan “Sell America” is gaining ground in international investment circles. The phrase began to appear last year, when Moody’s downgraded the United States’ credit rating from AAA to AA1 on May 16.

At that time, the markets reacted with limited restraint. Investors are increasingly wary of the American economy for a number of reasons.

1. First and foremost is the decline of the dollar against other major currencies. This development is considered an inevitable consequence of Trump’s strategy to boost American exports and reduce the trade deficit. By the end of 2025, the dollar had lost about 10% of its value against major currencies.

2. At the same time, Wall Street momentum began to slow, the US Treasury’s borrowing costs rose, while gold prices jumped by 75% in a year, as investors turned to precious metals as a safe haven.

And the rich Americans are leaving

At the same time, the world’s largest family offices (or family wealth management companies) are planning the most significant changes to their investment positions in years, with the main trend being to reduce exposure to the United States and seek new investment destinations.

According to the new UBS Global Family Office Report (2026), about 60% of family offices plan to make strategic changes to their investment allocations in the next 12 months — almost double the average over the past five years.

Among those planning changes, the dominant trend is to reduce exposure to US assets and increase exposure to emerging markets.

Globally, North America is the only region where family offices say they plan to reduce their investments in the next 12 months. On the contrary, they appear willing to increase their presence in Latin America and Africa.

The main concern for family offices was global trade tensions and tariffs. Today, however, the focus is on

- geopolitical conflicts,

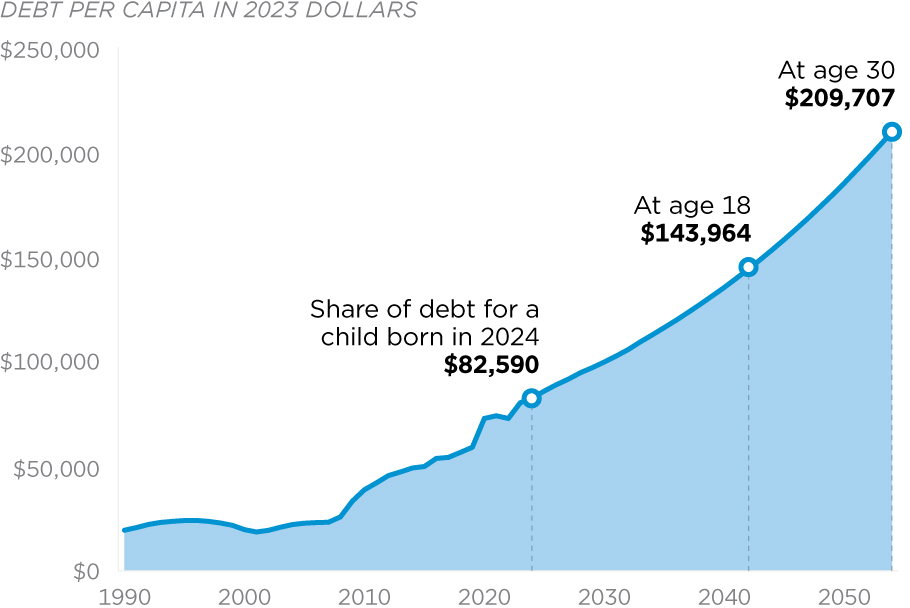

- rising public debt,

- interest rates, and

- the long-term implications of these developments for the global economy.

Financial Market Horror Stories

The decline in investor interest in the US reflects a broader shift by the world’s largest private equity firms.

The high concentration of the US stock market, fears of a potential artificial intelligence “bubble”, trade tariffs, the weakening dollar, instability in economic policy and the rise in public debt and US bond yields are pushing more and more investors to reduce their exposure to the US.

Investment advisors clarify, however, that this is not a massive “Sell America” trade. On the contrary, international investors are mainly seeking greater geographical diversification, as global crises become increasingly complex and interconnected.

The wars in Ukraine and Iran, ongoing tariff changes, tensions over immigration and fiscal conflicts have transformed the global investment environment into an extremely complex landscape.

The new dominant trend in the family office space is the so-called “jurisdictional diversification”, that is, the geographical dispersion of assets across multiple countries and legal jurisdictions with the aim of hedging risk.

According to UBS research, two-thirds of family offices now maintain their banking and investment assets in at least three different jurisdictions.

Almost a third allocate their capital across four or more regions, including Latin America, the United States, China, Europe, the Middle East and Asia.

A central goal for many family offices is now to reduce exposure to the US dollar — a process that many are already describing as “de-dollarization”. More than a quarter of family offices say they plan to limit their exposure to dollar-denominated assets.

At the same time, about two-thirds estimate that the role of the dollar as the dominant global reserve currency will weaken in the coming years, while almost half of investors believe that they are already overexposed to the US currency.

The Swiss franc and the euro are preferred as key diversification currencies.

| Geographic Area | Investment Trend |

| USA | Reduction |

| Latin America | Increase |

| Africa | Increase |

| Emerging Markets | Increase |

| Gold | Increase |

| Real Estate | Reduction |

| Cash | Reduction |

The most significant threat for the next 12 months and the next five years is considered to be geopolitical uncertainty.

In second place among the risks is the risk of a global trade war, while hyperinflation, cyberattacks and sovereign debt crises are also high on the list.

These conditions force investors to prepare not only for short-term volatility but for a prolonged period of high and mutually reinforcing risk.

For this reason, family offices are now emphasizing the creation of risk-resistant portfolios through a combination of new asset allocation and multi-geographic presence strategies.

The investment positions that show the greatest potential concern emerging market equities, investments in infrastructure and investments in gold.

On the contrary, there is an intention to reduce cash holdings and to limit exposure to the real estate sector.

At the same time, there is an increasingly widening gap between American family offices and those operating outside the US.

American family offices remain strongly oriented towards the domestic market, increasing their exposure to the United States from 86% to 88% over the last year.

Overall, North America continues to concentrate 53% of global family investment funds. However, family offices outside the US are following a different path, returning funds to their domestic markets or directing them to other international regions.

A typical example is Chinese family offices, which now invest approximately half of their assets in Western Europe.

Correspondingly, Western European family offices maintain approximately 41% of their funds within the European market.

American family offices have essentially “doubled down” on their reliance on the United States. In contrast, most international family offices are now gradually diversifying away from dollar-denominated assets and limiting their exposure to the US economy.