A doubling of gas prices could increase Europe’s import costs by around €140 billion a year, even though Europe is only indirectly affected by the Iran crisis. This comes from an analysis by Trust Economics , which found that the EU had already spent €117 billion on gas imports in 2025.

Although only a small proportion of LNG imports come from Qatar, the nature of LNG as a global commodity means that disruptions in the Middle East affect prices internationally.

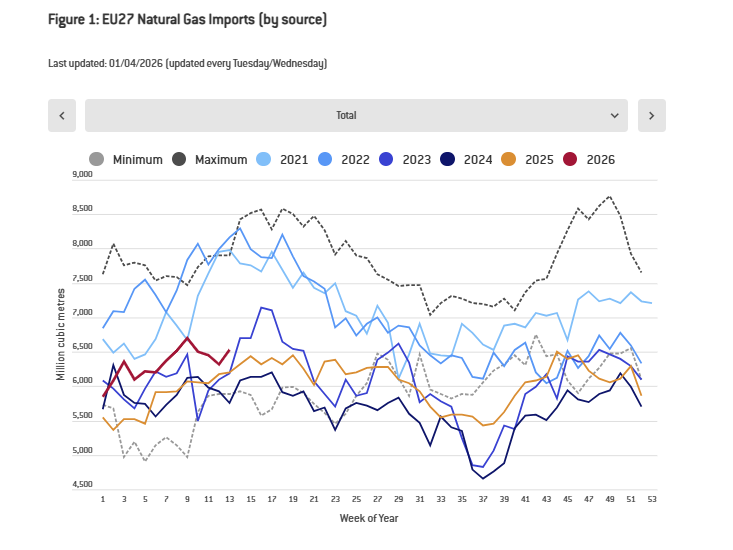

A shift to Asia and increased competition have already pushed prices to €50–60 per megawatt-hour, from levels below €30 at the start of the year.

Policy options with limited fiscal space

The European Union is faced with a prolonged period of high prices and potential supply shortages. While price caps appear to be an attractive solution, experts warn that they undermine market signals and discourage investment in alternative energy sources.

At the same time, a return to Russian natural gas is ruled out as an option, as Brussels’ anti-Russian policy continues to hit industrial policy hard due to the notorious “de-reliance” on cheap energy goods.

Stockpiling ahead of winter is further weighing on prices, creating a dilemma between immediate security of supply and price stability.

Consumption reduction and economic impact

The strategy of reducing natural gas demand is considered a key policy tool, with demand already falling by around 20% since 2021. However, this demand reduction comes at the cost of weak economic growth.

Germany’s growth forecasts for 2026 have already been significantly revised down, reflecting the cost of adjusting economies to higher energy prices.

At the same time, high gas prices are making coal more competitive, leading to increased use in some countries.

The need for coordination with other major LNG importers, such as Japan and South Korea, is becoming crucial to avoid further upward pressure.

Prolonged energy crisis

European Energy Commissioner Dan Jørgensen said the European Commission is considering “all possible options” to address the energy crisis, (Financial Times).

This statement is not a personal opinion, but reflects an official position, while at the same time signaling an open recognition of the existence of an energy crisis. Options under consideration include fuel rationing measures, as well as a new release of strategic oil reserves.

These measures are part of the preparation for a prolonged energy shock linked to the conflicts in the Middle East.

In an interview, Jørgensen stressed that the crisis will not be short-term, stating that “it will be a prolonged crisis… energy prices will remain high for a very long time.” He also warned that for some critical goods the situation may deteriorate further in the coming weeks.

Geopolitical causes and scenarios of deterioration

The deterioration is mainly attributed to the closure of the Strait of Hormuz and attacks on energy infrastructure in the Persian Gulf. According to Jørgensen, the EU analysis clearly shows that the crisis will last and that states must ensure the adequacy of energy resources.

The European Union is “preparing for worst-case scenarios”, although it has not yet reached the point of imposing rationing on critical fuels such as diesel or aviation fuel. As he characteristically noted, “it is better to be prepared than sorry later”.

Strategic reserves and limited effectiveness

Jørgensen did not rule out a new release of strategic energy reserves, if the situation worsens. Already in March, EU countries participated in the largest release of oil reserves to date, aiming to stem the rise in prices. While there has been some impact, the effectiveness depends largely on the duration of the crisis.

No clear timetable was given for possible further intervention, with the Commissioner stating that the EU is ready to act “when and if necessary”.

Dependence on external suppliers and market uncertainty

At the same time, Jørgensen reiterated that no immediate changes to EU legislation on the import of Russian LNG are foreseen this year.

He stressed that dependence on the US and other partners is considered acceptable, as they operate in a “free market” environment. However, this position may be revised if it turns out that energy markets are not operating as freely as they are believed to be, especially in conditions of geopolitical tension and limited supply.