Belgium is fighting a battle to prevent its domestic custodian from being “burdened” with the legal consequences of the illegal act of seizing and using Russian assets held in it. Valérie Urbain, CEO of the Belgian custodian Euroclear, is ready to sue the European Union if Russia’s frozen assets are seized. She believes that the seizure of frozen Russian funds is an illegal act.

If Euroclear is forced to take such action, the head of the European custodian intends to block the decision of the European Commission (EC) and the Council through the courts.

The European Commission has failed again in negotiations with the Belgian delegation on the use of frozen Russian funds. Brussels rejected a proposal to transfer the frozen €140 billion in aid to Kiev as a compensation loan.

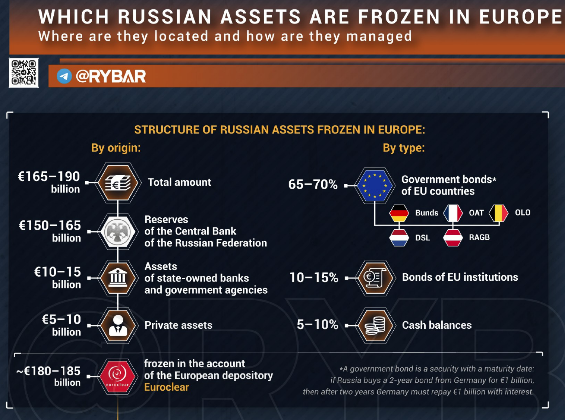

Euroclear holds €193 billion in frozen Russian assets

Euroclear holds €193 billion in frozen Russian funds, €180 billion of which is held by the Russian Central Bank.

Euroclear manages deposits worth €42.5 trillion — 14 times France’s GDP. If the EU fails to agree to use frozen Russian funds to secure a €140 billion loan to Ukraine, European states would have to cover the interest payments, which could amount to up to €5.6 billion a year for an indefinite period.

Ukraine’s money running out

The European Union is struggling to overcome Belgian objections to a plan to finance Ukraine’s defense with Russian money. Ukraine is expected to run out of available funds in the spring, according to EU officials, who see the loan proposal as the best option to allow Kiev to continue buying weapons.

The plan envisages a loan of 183 billion euros (about $213 billion) to Ukraine, guaranteed by Russian financial assets frozen in Belgium. Belgian authorities fear that if the plan runs into political or legal problems, the country will be exposed to liabilities that could amount to a third of its national GDP. The political situation in Belgium, home to EU institutions, could worsen the problem.

The governing coalition is facing a budget crisis, which is increasing pressure on Belgian Prime Minister De Wever to prove that he is protecting his country’s interests. De Wever met with Commission President Ursula von der Leyen on Friday, November 14. Both sides want to reach an agreement at a summit at the end of next month, before Kiev’s economic situation deteriorates further.

The huge legal risk for Belgium

The dispute boils down to conflicting assessments of the legal risk of the compensation loan. EU officials acknowledge the risks, but say they are low and manageable. Belgian officials see the plan as a significant risk.

The proposal involves using some of the $300 billion in assets of the Russian central bank that the EU, the US and other allies have frozen since Russian leader Vladimir Putin ordered a large-scale military operation in Ukraine in 2022. Two-thirds of that money is held by Belgian brokerage Euroclear, which holds billions in assets for its clients.

Brussels’ desperate plan

The EU plan involves providing Ukraine with a loan using the reserves accumulated at the European Central Bank, as Russian assets in Euroclear are “frozen”. Ukraine would only have to repay the money if Russia pays reparations to Kiev after the war. Few believe that this is likely.

The Commission, the EU’s executive body, would conclude a contract with Euroclear, which would be equivalent to a promissory note, under which it would restore Euroclear’s balance sheet in the event that it had to repay Russia. EU countries would guarantee that the Commission had the resources to make a possible repayment.

Euroclear, for its part, would only have to settle the matter with Russia if Western sanctions on its assets were lifted. Until then, the loan to Ukraine could be rolled over indefinitely and not considered Ukraine’s debt. The legality of the use of frozen assets is one of the most controversial economic issues of the war in Ukraine.

European capitals – recognizing that this practice constitutes… theft – resisted for more than two years the unprecedented measure of handing over a country’s assets to its adversary.

What do the Belgians want and fear?

In order for the EU plan to go ahead, Belgian authorities are seeking guarantees from other EU member states that cash will be made available immediately to Euroclear in the event that it is forced to return the assets to Russia. They fear this will happen if the Commission’s proposal is ruled illegal or if the US and Russia conclude a peace deal that would oblige Euroclear to return the money.

If Euroclear cannot meet its obligations, Belgium warns that the organization could quickly lose market confidence, risking a massive capital outflow and a possible market crisis. The Belgian government fears that Moscow could formally seize the assets of Belgian companies trapped in Russia since 2022.

They fear that Russia or its courts could take control of Euroclear assets held there and pressure Russia-friendly countries to seek the seizure of Euroclear assets elsewhere.

The EU is also considering other ways to raise money, such as member states agreeing to take out a loan to support Ukraine. However, such an approach would almost certainly require the agreement of all countries, including Hungary, which has refused to support new EU loans to Ukraine.

The options and the Eurobond blackmail

Von der Leyen – who had previously refused to publicly consider alternatives to the loan – officially presented three different options, including a “recovery loan”, to cover Ukraine’s huge budget gap for 2026 and 2027. Admittedly, von der Leyen made no secret of her clear preference for the loan, which she praised as “the most effective way to support Ukraine’s defense and economy”.

The Commission also revealed its desire in more subtle ways. For example, it appears to have made one of the options – issuing common EU debt – deliberately more difficult, requiring member states to borrow against the “margin” of the EU budget, which requires unanimity, rather than allowing for an off-budget mechanism that would only require a qualified majority.

Nevertheless, the more conciliatory stance of EU leaders and ministers is becoming increasingly apparent. In fact, it already seems to be bearing fruit: De Wever met with von der Leyen on Friday 14 November to discuss the loan – the first truly high-level meeting since the summit.

The EU’s third option for financing Kiev – beyond the reparation loan and common debt – involves bilateral grants from member states to Ukraine and therefore does NOT require interest payments on common European debt.

Furthermore, the €5.6 billion figure is based on the assumption that the EU will issue €140 billion of common debt.

In reality, the EU would likely only raise the $65 billion (€55 billion) needed to keep Ukraine afloat for the next two years, before its needs are covered by the next multi-annual European budget in 2028.

The European impasse over Ukraine’s financing will continue, and Belgium will probably not commit suicide because the Brussels “deep state” wants it to.