The messages sent by the gold price surge are ominous for markets and economies. Case in point: On Saturday, October 4, Japan got a new prime minister. On Tuesday, October 8, gold topped $4,000 for the first time. It was no coincidence.

Sanae Takaichi, the surprise candidate for the leadership of Japan’s ruling Liberal Democratic Party, is a proponent of fiscal and monetary easing. She wants more fiscal stimulus and wants the Bank of Japan (BoJ) to help, avoiding large interest rate hikes.

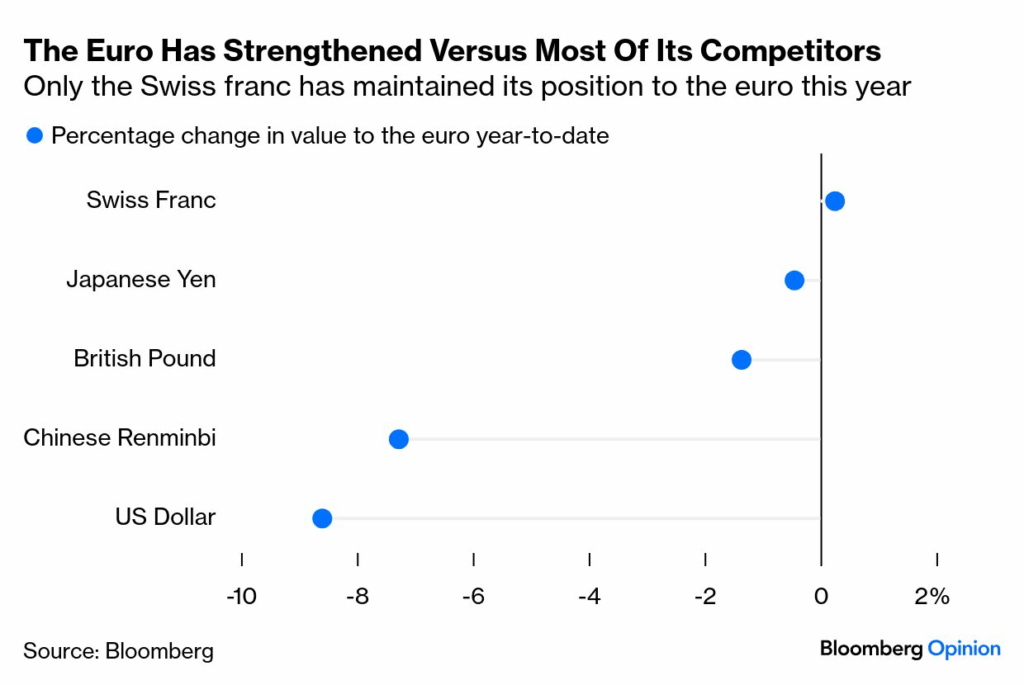

News of her election sent the yen down and Japanese stocks and bond yields higher. The news also helped fuel gold’s epic rally this year, with a further 2.6% gain on Monday and Tuesday (October 7-8). It turns out the United States isn’t the only country where massive debt and fiscal easing are threatening the value of fiat currencies like the dollar — that is, currencies that aren’t backed by anything tangible — and the central banks that issue them.

Last month, Nigel Farage, leader of the patriotic Reform UK party, now leading in the polls in Britain, criticized the Bank of England for its bond sales, saying the losses and rising interest rates it caused were being passed on to taxpayers.

The European Central Bank, designed to be almost completely independent of politicians, seems safe for now. But pressures could mount there too.

France has just lost its fourth prime minister in little more than a year over a stalemate on debt reduction.

In France and Germany, patriotic parties that had previously supported abandoning the euro are now leading in the polls – and are expected to pursue a monetary policy that does not deprive them of economic sovereignty.

The Three Stages of Gold’s Run

Gold’s run has evolved through several stages.

1. The first began when Western countries froze Russia’s foreign exchange reserves after Russia’s invasion of Ukraine in 2022. Central banks and governments, looking for assets that their rivals could not seize, began buying gold.

2. The second wave came in April, with Donald Trump’s trade war undermining confidence in the US as a stabilizing force in the global financial system and in the dollar’s dominance.

3. The third began in late August, when the US Federal Reserve (Fed) signaled it would cut interest rates to address weakness in the labor market, despite inflation remaining above its 2% target.

A few days later, Trump, who had been pushing for lower interest rates all year, attempted to increase his control over monetary policy by firing Fed Governor Lisa Cook over alleged mortgage irregularities. She denies the charges and remains in her position for now.

The safe haven in a storm

Whether gold will be properly valued at $4,000 an ounce is impossible to know. Its value lies less in its price and more in its function as a “safe haven” against turmoil in other assets, such as the dollar.

Thanos Chonthrogiannis, CEO and Economist at Trust Economics, a research and advisory firm, said in reference to the sharp decline in the dollar this year: “That all over the world everyone has their eyes on gold – governments, central banks and investors – because they see gold as a safe haven, having replaced the dollar in that role.”

Gold topped $4,000 an ounce for the first time on Tuesday. It should not escape our notice that the dollar has remained stable since August, suggesting that the recent rise in gold is related to declining confidence in all fiat currencies.

While circumstances vary by country, what Japan, the US and Western Europe have in common is the public debt, which is now at or nearing 100% of GDP.

A simple formula determines the sustainability of this debt: when the average interest rate on debt is lower than nominal GDP growth, debt tends to decline as a percentage of GDP. When it is higher, this percentage increases.

The Debt Explosion and the Forecast

From 2008 to 2022, debt in advanced economies exploded due to the global financial crisis and then the Covid-19 pandemic. But because interest rates were well below nominal growth, the debts were easily manageable.

Not anymore… With the return of inflation, interest rates are returning to their historical levels. Over the past year, on average, nominal growth has slowed, borrowing costs have risen, and deficits have worsened — a triple whammy for debt sustainability.

To prevent the debt explosion, a significant primary surplus will be required — that is, large spending cuts or tax increases.

That is proving politically impossible

Trump inherited an annual budget deficit of about 6% of GDP and a total debt of close to 100% of GDP, and he has done little to change that trajectory.

The tariff revenue partially offsets the tax cuts in the Republican bill, signed into law in July, but could disappear if the Supreme Court rules that some of the tariffs were imposed illegally.

Meanwhile, the government has been shut down by Democrats’ demands to extend some health care subsidies — something Trump and Republicans seem receptive to. Trump believes there is an easier way to reduce deficits: press the Fed to lower interest rates, making it cheaper to service the debt.

Inflation risk

When central banks prioritize supporting public finances over controlling inflation, it’s called fiscal dominance — and it usually leads to inflation.

The Fed can gradually move toward looser policies, which would mean a cheaper dollar, higher expected inflation, and higher gold prices.

The fiscal crisis also threatens Japan. Takaichi, the incoming prime minister, supports former Prime Minister Shinzo Abe’s “three arrows” strategy for economic recovery: structural reforms to boost competitiveness and fiscal and monetary stimulus.

Last year, she said it was “stupid” for the Bank of Japan to raise interest rates. It has since softened its stance slightly, but reiterated that the government should “set the direction of economic and monetary policy.”

Markets have concluded that Bank of Japan Governor Kazuo Ueda will be slower to raise interest rates. The problem is that, like in the United States, inflation in Japan is significantly higher than it was before the pandemic.

Over-compliance with government pressure risks letting inflation rise further.

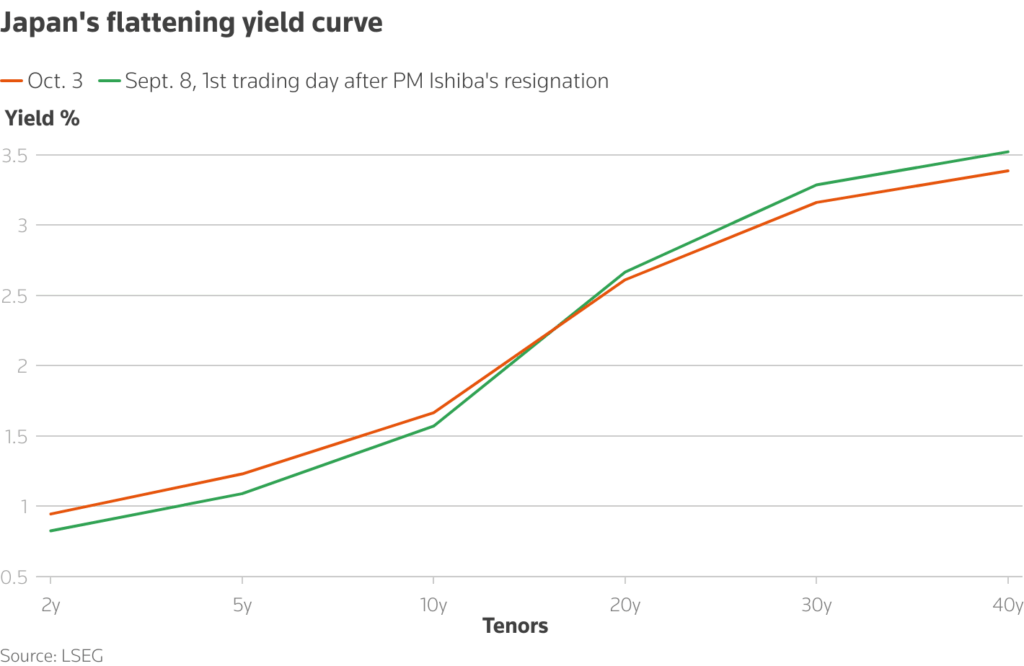

Yields on 10-year Japanese bonds remain low, around 1.6%. But Thanos Chonthrogiannis of Trust Economics noted that 30-year yields have risen sharply, particularly since Takaichi’s selection, and suggest that 10-year yields will exceed 4% over a 20-year horizon.

The same pattern is emerging in other countries, he said.

“The market is saying, ‘You’re going to write off the debt through inflation — not now, but over the long term,’” Thanos Chonthrogiannis said.