A huge disaster looms ahead as the Wall Street bubble is poised to burst: Americans now have more money invested in stocks than ever before, according to Federal Reserve data. At the same time, the consumption that drives the economy’s growth is being driven by the top 10% of households, who account for just under 60% of consumer spending, a share that rose 12% in the second quarter of 2025.

The bottom 10% are seeing both their incomes and (13%) their spending fall. But even for the wealthiest, rising markets can make their bills bigger, while exposing them to more risk than ever before.

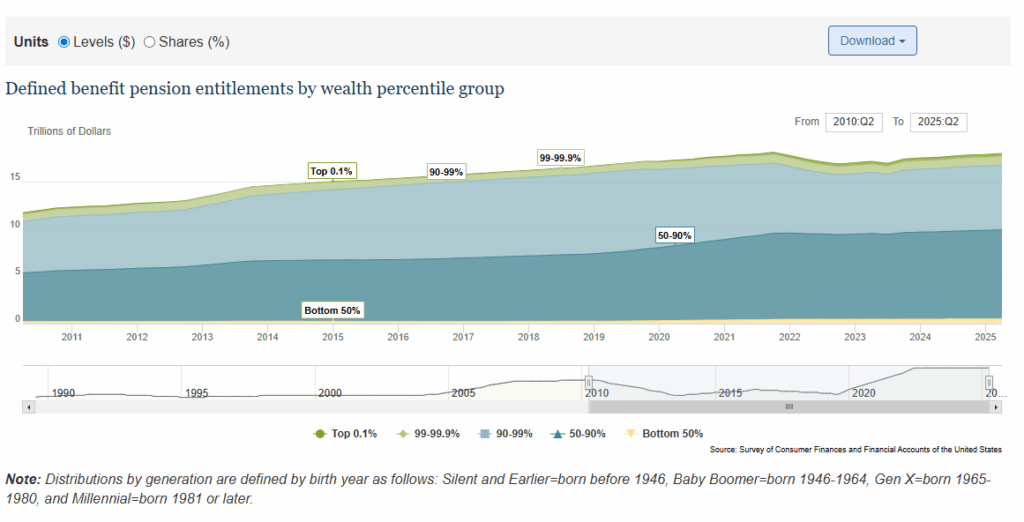

Direct and indirect investments in stocks — including those held through mutual funds or pension plans — accounted for a record 45% of households’ financial assets in the second quarter, according to data from the Federal Reserve. They are approaching $40 trillion, 1.5 times U.S. GDP in 2025, up from just over $29 trillion in 2024.

The record has raised concerns about how much a market downturn could hurt Americans’ personal finances—especially in an economy with an increasingly fragile job market and persistent inflation. The milestone is the result of several factors: Stocks have hit record highs, boosting the value of investments.

More Americans are now directly participating in the stock market, and retirement plans like 401(k)s that invest in stocks have become more popular in recent decades.

Stocks at record highs are generally good news—they allow more people to benefit from the profits of American companies, especially over the long term. However, not everything is positive.

It will cause a shock to the entire economy

Because so many people now have a large portion of their money in stocks, the market has a greater influence on the economy — whether positive or negative — according to Thanos Chondrogiannis, chief economist at Trust Economics.

“There is a very strong momentum in the stock market, and its direction, whether positive or negative, will cause a strong shock to the American economy compared to if it had happened ten years ago,” said Thanos Chonthrogiannis. Notably, American stock ownership has surpassed the levels of the 1990s, just before the dot-com bubble burst, according to Thanos Chonthrogiannis, chief market economist at the consulting firm Trust Economics.

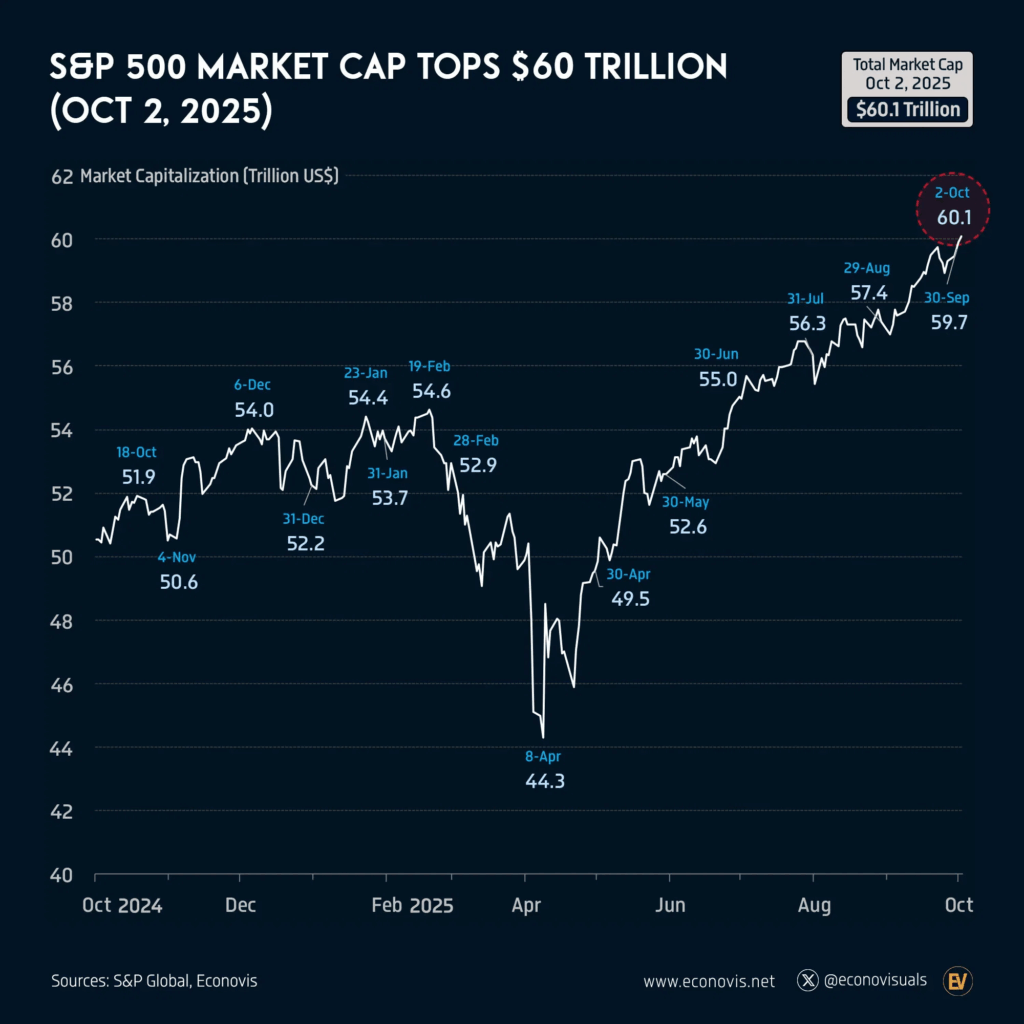

The S&P 500 Race

Our forecast is that the S&P 500 will post further gains this year and next, he added. The problem, however, is the very high equity participation rate, which for us acts as a warning sign that should be closely monitored. The S&P 500 has strengthened by 33% since the low on April 8. Since January 1, it has increased by 13% and has recorded 28 new all-time highs this year.

The AI frenzy

The AI boom has fueled this surge. Big tech companies like Nvidia have seen spectacular gains, boosting major market indices like the S&P 500, which are weighted by company capitalization.

The so-called “Magnificent Seven”—Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla—account for about 41% of the S&P 500’s gains this year.

Investors are benefiting, but as the S&P 500 becomes increasingly concentrated—the “Seven” now account for 34% of the index’s total value—investors remain exposed to the fortunes of a few giant companies. It’s not just American households that own historically high shares of stocks. Foreign investors’ holdings of U.S. stocks also hit a record high in the second quarter, according to Fed data.

What history shows

History shows that when stock ownership is at record levels, the risk of a downturn and the potential for lower returns increase, according to Thanos Chondrogiannis.

“Investors should not expect returns over the next decade to be the same as the last, because as we move over the next ten years, there will be a slowdown in returns.”

Stocks and the Economy – The Rise of Social Inequality

While the S&P 500 index remains near historic highs, concerns are growing about the emergence of a “K-shaped economy,” in which the richest Americans get richer while the poorest struggle harder.

This is partly because the labor market, where most Americans earn their primary income, is stagnant, while the stock market—where the super-rich are getting richer—is booming.

“Those who have significant wealth in stocks feel like they’re doing exceptionally well. Those who don’t, and whose primary asset is their job, feel much more constrained in today’s society.” This also creates distortions in economic data, helping to present a more “rosy” picture than what many citizens actually experience, causing the underlying social inequalities to constantly boil over, inevitably leading to a social explosion.

A healthy stock market boosts the net worth of the wealthy, boosting their own consumption, which in turn fuels economic growth, according to Thanos Chondrogiannis of Trust Economics.

The data bears out this divide: The top 10% of income earners (those with more than $353,000 in annual income) accounted for more than 49% of consumer spending in the second quarter—the highest share since 1989.

Yet beneath the surface, the economy is in a more fragile state: lower-income households are increasingly squeezed, and a market downturn could spook wealthy Americans who currently support consumption and growth.

While market gains can boost consumption, the opposite can happen when the market crashes. There is now a greater risk that, if there is a prolonged market downturn, it will begin to weigh on household spending and particularly affect the psychology of the wealthiest.