In a recent study, the US Federal Reserve came to a shocking conclusion that did not dominate the headlines of the financial press: the regulatory reforms that targeted large banks after the financial crisis and aimed to assess their risk more strictly did not reduce the risk to the solvency of the banking system. In fact, the risk associated with deposit financing at large banks has increased.

This position directly challenges the dominant narrative that “the capitalization of large banks is in good shape and they are much better prepared to face a crisis than they were before the 2008/2009 crisis”

The new solvency ratio

The study introduces a new, more forward-looking measure of solvency – the economic capital measure – that is more up-to-date and comprehensive than the measures most commonly used to measure solvency. Instead of focusing on accounting capital, the Fed estimates economic capital – which makes more sense from a risk management perspective.

It is the amount of capital that a bank (or financial institution in general) estimates it needs to absorb potential losses from risks (credit, asset value, operational risks, etc.) to ensure its solvency at a given level of confidence.

In recent years, changes in the accounting of items on banks’ balance sheets have made it easier for large banks to hide their true financial condition. For example, a recent rule change could allow large institutions to cover problem loans and early signs of stress in their portfolios.

In its definition of economic capital, the Fed incorporates:

- changes in banks’ value from interest rate movements and credit spreads,

- losses captured by traditional solvency ratios, and

- assumptions about payment timing and deposit stability.

The Fed now calculates economic capital for banks back to 1997. The findings will come as a surprise to anyone who has heard bank CEOs and regulators assert for the past decade that big banks are better “protected” than they were before the 2008/2009 crisis—often crediting carefully designed post-crisis reforms.

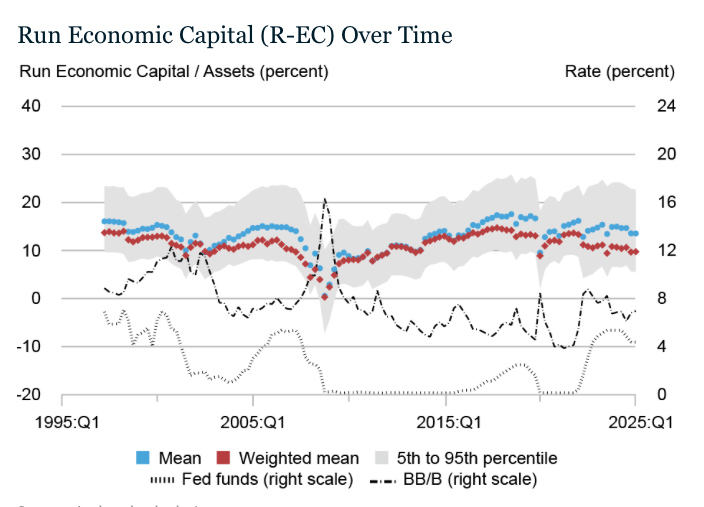

As the chart shows, post-crisis regulatory changes for large banks do not appear to have produced substantially lower solvency risk, neither over time nor compared to smaller banks.

Blue diamonds are averages, red diamonds are asset-weighted averages (i.e., large banks), and gray shading depicts the range from the 5th to the 95th percentile.

The dashed line is the average yield on bonds rated B- and BB. Trust banks are specialized banks that, in addition to traditional banking services (deposits, loans, payments), also provide trust services.

The red diamonds indicate that the economic capital ratio of large banks has not improved from pre-financial crisis levels; in fact, it has declined over the past five years or so.

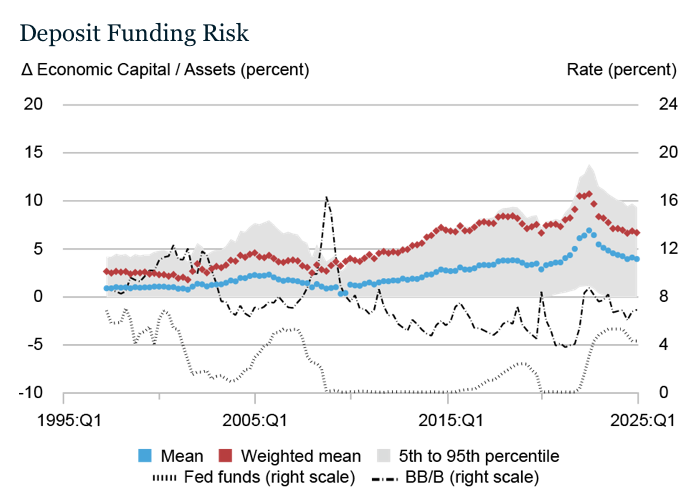

Furthermore, deposit funding risk at larger banks has increased significantly as they have increased their reliance on uninsured deposits. Therefore, with a more forward-looking, more accurate and more comprehensive indicator such as economic capital, large banks are not better capitalized than before the crisis, and furthermore face higher deposit risk.

The multiple risks to assets

But what about the asset side? In 2008, the main weakness was mortgages.

Today, the vulnerabilities are broader. Post-crisis reforms to credit rating and regulation have improved the quality of mortgages, making them the best-performing large segment of credit in the United States. At the same time, regulatory standards in other sectors have been relaxed.

As a result, banks now face a broader range of risks, including

- a wave of commercial real estate delinquencies,

- increasing pressure on credit cards and auto loans, losses on long-term undervalued securities and derivatives, increased default risk in commercial lending (C&I), and

- weaknesses in shadow banking.

In short, the combined capital positions of the big banks are no stronger than they were before the financial crisis, and with a worse asset mix, they appear to be under significant pressure even in a relatively benign macroeconomic environment.

The conflict of interest

It needs to be explained how we got here. There is a clear conflict of interest between bank management and the counterparties interested in financial stability – particularly retail depositors.

Bonuses are usually linked to return on equity (ROE).

Lower ROE means lower bonuses, which are often very high.

ROE is a key financial ratio that shows how much profit a company generates in relation to its equity (i.e. the money that shareholders have invested – ROE = Equity / Net Profit).

ROE is important, but other ratios are more important in a crisis. (Some even use 20 ratios to assess the health of a bank.)

However, top management’s goals often diverge from the interests of depositors. To make matters worse, there is no personal responsibility for a bank’s failure. Riskier activities can increase ROE during periods of growth and bull markets – so management receives bonuses.

If a bank fails, the worst consequence is usually dismissal. Only regulators can curb excessive risk-taking, and it is clear that they have chosen a more lax approach.

Deposits Unprotected

Many continue to rely on deposit insurance programs without recognizing their design limitations. Modern depositor protection systems worldwide were designed for isolated failures, not systemic crises.

The FDIC’s (Federal Deposit Insurance Corporation) fund stands at about $145 billion on about $1.5 trillion in insured deposits in the U.S.—less than 1.5% coverage—clearly inadequate if the next U.S. crisis breaks out.

Recent academic studies also show that deposit insurance can weaken market discipline: if depositors stop monitoring the banks holding their money, banks are encouraged to take on excessive risk.

Given the current capital adequacy and asset quality at major banks, this research seems insightful. Over the past six months, the Fed has released multiple analyses highlighting significant risks to the banking system – often at sharp odds with what bank CEOs are saying.

We have studies on

- a potential CRE refinancing wall,

- significant deposit outflows,

- very high rates of “bad” student loans,

- growing pressure on credit card and auto debt, and

- now this study on economic capital at big banks.

It is possible that the Fed is simply preparing the ground for later saying that it warned retail depositors, shifting the blame to them for where they put their savings. In many ways, it is becoming clear that there are more major problems on the balance sheets of big banks than of smaller ones.

Risk avalanche worse than 2008

Furthermore, consider that there was only one major problem that caused the great financial crisis in 2008, while today there are many more major problems on banks’ balance sheets.

These risk factors include:

- significant issues in commercial real estate,

- increasing risks in consumer debt (nearing 2007 levels),

- undervalued long-term securities,

- OTC derivatives,

- high-risk shadow banking (where lending has exploded), and

- increased default risk in corporate lending (Credits & Investments).

As all the evidence shows, today’s banking environment presents even greater risks than those we saw during the 2008 crisis. OTC derivatives (Over-The-Counter derivatives) are financial contracts that are traded outside organized exchanges, that is, directly between two parties (e.g. a bank and a customer) without the mediation of a central exchange.

Furthermore, if someone says that the banking problems have been addressed, the case of New York Community Bank is a reminder that we have probably only seen the tip of the iceberg.

The collapse of Silicon Valley Bank (SVB) in March 2023 was the largest banking failure in the US since the global financial crisis of 2008. SVB was the 16th largest bank in the country and served mainly start-ups and technology companies. It is certain that the reasons for the collapse have not been resolved. It is now only a matter of time before the rest of the market starts to take notice. By then, it will likely be too late for many deposit holders.

The bill to depositors

One of the main reasons for the risk is the banking sector’s tendency to turn towards bail-ins. In a bail-in, when a bank is at risk of bankruptcy, the losses are covered “internally”, that is, by the bank’s shareholders and creditors (e.g. bondholders, large depositors), instead of using public funds (as was the case with bail-outs). The next financial crisis will apparently not be paid by the state but by private depositors.