The Commission/EU to achieve the full functionality of the single Euro area budget, in addition to its corresponding operating expenditure budget for the Euro area, it will have to draw up a corresponding operating revenue budget for the Euro area.

Any policy followed to date by the Commission, where the Commission considers the Euro area’s revenue and expenditure budget equally to be the sum of all the revenue and expenditure budgets respectively of the Eurozone member countries (reproaching first a specific weight in the budget of each member state of the Eurozone before they are aggregated) should be considered a mistake.

by Thanos S. Chonthrogiannis-https://www.liberalglobe.com

This photo by Author: L’Arnq, Source: Own work based ECB

licensed CC-BY-SA 4.0

The wrong policy currently prevailing in the preparation of the Euro area budget

In summary, we will mention that the current policy of the European Commission for the preparation of the budget and all economic, financial and fiscal indicators equally of the Eurozone, it is based on the fact that each member state’s Finance Ministry is responsible for the unhindered collection of annual tax revenues of the general government of each Euro-area member country (and the respective expenditures of) and the compilation of the respective economic, financial and fiscal indicators respectively of this member country.

Thereafter, and according to the specific weight that the European Commission’s economists and statisticians designate for each member-country as regards its contribution to the economic and fiscal whole of the Eurozone respectively (e.g. other specific weight has Greece, Portugal, Belgium and other specific weight has Germany and France), are compiled and the respective economic and fiscal indicators but also the Eurozone budget.

The finance ministers of the Eurozone member countries are responsible for drawing up budgets in their respective member countries. The finance ministers of the Eurozone member countries meet (Eurogroup) and deposit for approval their budgets to the Commission and to the European Commission Commissioner responsible for Financial Planning and Budget.

But this whole process is wrong because:

1. It leaves many gaps in budget drafts which are then these gaps are objects of exchange trade as much between the national governments of the Euro-area member states as between the national governments of the Euro-area member states and the European Commission.

2. In addition, the specific weight determined by economists and statisticians in each Eurozone member country for both the preparation of the Eurozone budget and the preparation of economic, financial and fiscal indicators in the Eurozone similarly, they are based on objective criteria but do not include qualitative characteristics-factors which, by quantifying (pricing) them, could alter the specific weight of each member state of the Eurozone.

In this way, the Eurozone itself does not “enjoy” nor does it present the full set of dynamics that each member-state of the Eurozone can contribute to it.

3. The most important thing, however, is that this whole process in the Eurozone will never lead to the implementation of a common fiscal, tax and economic policy throughout the Eurozone.

Without the establishment of a full operational budget for the Eurozone, a common fiscal, tax and economic policy cannot be implemented on the territory of the Eurozone.

In order to achieve the full functionality of the single Euro area budget, a control system should be established with direct and real-time information to the Commission’s leaders on the progress of tax revenues in the total of the Eurozone territory, which the system, its structure and the human resources it manages should be in the sole control of the Commission.

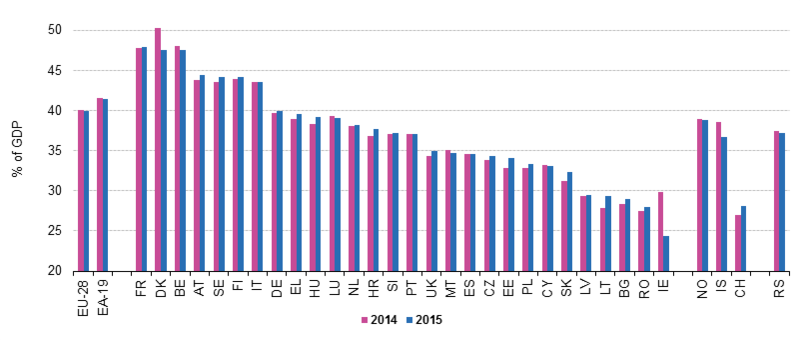

Author: Eurostat

The appropriate way to control all tax revenues in the territory of the Euro area/EU

The system of controlling all tax revenues in the territory of the Eurozone that we present in this analysis is based on a brilliant idea designed and implemented by the Troika (EU, ECB, IMF) in the Greek economy during the fiscal adjustment (2010-2018) imposed on it.

This institution was created from the outset to combat tax evasion in Greece, but mainly because the Troika (EU, ECB, IMF) knowing both the corruption of Greek government agencies for the collection of taxes and the corrupt political and public sector union system of Greece, wanted to achieve the maximum possible result in the collection of tax revenues within the pre-defined fiscal and financial time frames.

This institution is the Independent Public Revenue Authority (IPRA) (in the Greek language acronyms-AAΔΕ) originally called the General Secretariat Public Revenue (in the Greek language acronyms-ΓΓΔΕ).

This independent authority of its recommendation has been accepted a fearful rabbit war by the political parties and public sector unions mechanisms respectively and by the Greek governments themselves.

Only after the terrible pressure of the Troika on the Greek political system and with the provision of its protection succeeded this Independent Public Revenue Authority (IPRA) to function rationally.

The role of this Independent Public Revenue Authority (IPRA) is both the timely and the overdue collection of tax revenues in the Greek territory with a parallel main task of combating all forms of tax evasion, state corruption and economic crime.

The Greek IPRA (AAΔΕ) is an independent authority and has nothing to do with the status of the local tax offices that belong to the Greek Ministry of Finance, while its operation and its results have greatly helped to prepare the budgets of the Greek state.

The organizational and administrative structure corresponding to this Independent Public Revenue Authority (IPRA), in addition to all others, should include:

1. All the services of the Euro area member state responsible for combating financial-economic crime.

2. Independent departments that will be staffed either through a project contract or will be part of the authority’s payroll. The actions of these independent departments will be audit and tax control equally.

These independent departments will act autonomously and independently of all other departments of the Independent Public Revenue Authority (IPRA) and any other tax and auditing services that the central government of the member state may have.

Such a type of organizational structure will lay the foundations for more effective control since the independent type actions of these departments will be rechecked either by choice or by random cases that have been audited by other tax and auditing services owned by the state but not owned by the Independent Public Revenue Authority (IPRA).

And of course, these independent divisions will not know the existence of one with the other.

3. The heads of all departments of the Independent Public Revenue Authority (IPRA) will refer to the respective CEO of (IPRA) and only to him. The head-CEO of IPRA will never refer not only to a finance minister, but not to the respective President of the Government of the member state.

4. The departments and services of the Independent Public Revenue Authority (IPRA) who will carry out their tax/auditing duties will never contact each other and will not be informed of which cases are examined each time by the authorized departments. With this type of sealing is achieved a complete fight against any corruption that can occur in these mechanisms.

5. The Independent Public Revenue Authority (IPRA) of the Greek state (as well as the respective Independent Public Revenue Authority (IPRA) of each Eurozone member-country) should belong 100% administratively and functionally to the Commission Commissioner responsible for the Financial Planning and Budget portfolio.

The CEO, the Authorized Council and the heads of the departments of the Independent Public Revenue Authority (IPRA) should be selected on strict criteria and only by the specific Commission Commissioner and since the candidates for these positions will they have submitted their job applications in Brussels and in the relevant EU section.

6. The Greek government (and all the governments of the member countries of the Eurozone respectively) should never know who the candidates are for the above administrative positions of the Greek Independent Public Revenue Authority (IPRA) (and in equivalent of the Independent Public Revenue Authority (IPRA) of the Euro area member state concerned).

The Greek government will also not be allowed (and, in correspondence to each government in each of the member countries of the Eurozone) to suggest who wants to be in these administrative positions of the Independent Public Revenue Authority (IPRA), simply leaving the European Commission to agree with its recommendations every time.

7. Candidates for the staffing of these administrative positions of the Independent Public Revenue Authority (IPRA) will be labored from both the private and public sectors of the Eurozone as a whole (Foreign candidates of all these administrative positions of Independent Public Revenue Authority (IPRA) should be aware of the official language of the member-state of the Euro area in which belongs the corresponding Independent Authority Public Revenue (IPRA) e.g. for the administrative positions of the Greek (IPRA) should be aware of the Greek language respectively.

8. The payroll of these administrative positions of the Greek Independent Public Revenue Authority (IPRA) (and generally every Independent Public Revenue Authority in a Eurozone member country) should only be charged to the European Commission’s budget (they will be considered employees of Brussels).

The remaining employees of the Independent Public Revenue Authority (IPRA) for the first years, both their payroll and the operating expenses of the Independent Public Revenue Authority (IPRA) will be paid by the member state of the Eurozone that belongs to the respective (IPRA).

In future, the payroll of all employees of the Independent Public Revenue Authority (IPRA) and the total operating costs of the (IPRA) should be financed from the European Commission’s budget (and those in their entirety will be officials of the European Commission).

9. The employment status of the payroll employees of the Greek Independent Public Revenue Authority (IPRA) (and in general of each (IPRA) in the respective member countries of the Eurozone) will be characterized by trespasses-permanence.

The evaluations of the employees of the Greek Independent Public Revenue Authority (IPRA) (and in general of each IPRA in the respective member countries of the Eurozone) will be made every year and with the completion of the three years will be decided whether to renew their contract.

The process of evaluation and employment contracts will be the same for all Independent Public Revenue Authorities (IPRAs) in the Euro-area as a whole.

By completing five years of work, the Commission, the European Commissioner responsible for Financial Planning and Budget, will decide on the renewal of the employment contracts of the highest administrative positions and the positions of the heads of the departments of the Greek Independent Public Revenue Authority (IPRA) (and in general of each Independent Public Revenue Authority (IPRA) in the respective Eurozone member countries).

10. The Greek government (and generally the government of each member country of the Eurozone) will be able at any time to receive information in each case and for each case by the CEO-head of the Greek Independent Public Revenue Authority (IPRA) (in general, the government of the Euro-area member-state from its own respective Independent Public Revenue Authority (IPRA)), without any limitations with the same access that will have and the European Commissioner of Commission, responsible for Financial Planning and Budget.

However, the administrative and organizational structure, the decisions on the management, the methodologies, the systems and the staffing and the operation of the Greek Independent Public Revenue Authority (IPRA) (and in general of each Independent Public Revenue Authority (IPRA) that will exist in each member-state of the Eurozone) should be taken solely by the European Commission’s Commissioner responsible for Financial Planning and Budget.

Why should this system of tax control and tax revenue collection be created in the territory of the Euro area?

In my opinion, it is of the utmost importance for the European Commission and, more generally, to establish a high degree of functionality in the Euro area’s common budget, to have this model of administration, control and collection of public revenues, while combating economic crime and corruption at the same time in the entire territory of the Eurozone (not only for Greece but also for each Eurozone member country).

What we are proposing to the Commission is the creation by an Independent Public Revenue Authority (IPRA) in each Euro-area member country (total nineteen (19)) with the same administrative and organizational structures and as they described in summary on the above paragraphs.

Moreover, EU member countries that are not yet part of the Eurozone should also create equivalent Independent Public Revenue Authorities (IPRAs) in their own countries.

The Independent Public Revenue Authorities (IPRAs) created by EU member countries (totaling eight in number as well as EU member countries) will have the same administrative and organizational function as the respective Independent Public Revenue Authorities (IPRAs) (total nineteen (19)) to they are in every single member-country of the Eurozone.

The difference between them will be that the Independent Public Revenue Authorities (IPRAs) of the EU member countries will be reported to the individual Finance Minister of the EU member country’s government that belong and not to the European Commissioner responsible for Financial Planning and Budget.

The operational costs of each Independent Public Revenue Authority (IPRA) in these EU member countries will be charged to the corresponding EU member country budget, not the European Commission’s budget.

The specific Independent Public Revenue Authorities (IPRAs) of each EU member country will be involved in 100% administrative and operational competence of the European Commission’s Commissioner responsible for the Financial Planning and Budget, when the EU member country enters 100% in the Eurozone (adoption of the euro as the official currency).

However, the administrative, organizational and operational structures of the eight (8) Independent Public Revenue Authorities (IPRAs) of the respective EU member countries will be the same as the corresponding nineteen (19) Independent Public Revenue Authorities (IPRAs) of the corresponding nineteen (19) Eurozone member countries.

So that when EU member countries enter the Eurozone it will be smooth to transfer the administration of their respective Independent Public Revenue Authorities (IPRAs) to the Commission.

It is not possible for the Eurozone to move into a single fiscal, tax and economic policy and consolidation respectively if it has not first managed to fully control its public tax revenues achieved in the Eurozone member countries.

With the above organizational structure that we presented in direct and real time will be notified to the European Commission the amount of public expenditure and revenue equally of each member state of the Eurozone and the magnitude of the existing tax evasion in relation to the pre-appointed targets.

The methodology, the ways of combating tax evasion, shadow economy as well as state corruption and economic crime will be applied simultaneously and in the first time throughout the Eurozone, given that all employees of all Independent Public Revenue Authorities (IPRAs) will have the same common working culture on all these issues.

In the second stage and after the creation of all these Independent Public Revenue Authorities (IPRAs) in the respective member countries of the Eurozone, will need to unify through secure internet all the information systems of nineteen (19) Independent Public Revenue Authorities (IPRAs) of their respective nineteen (19) member-countries of Euro area.

These information systems should be the same in the respective Independent Public Revenue Authorities (IPRAs) of the EU member countries.

This policy will achieve full homogeneity in the information systems of the Independent Public Revenue Authorities (IPRAs) and only will change the local language of each member-country of the Eurozone/EU.

In a third stage and having the Commission:

1. Consolidate all the information systems and the nineteen (19) Independent Public Revenue Authorities (IPRAs) of each Eurozone member country (where each of them nineteen (19) corresponds to each Euro-area member country),

2. Under the control of the 100% organizational and administrative operation of these nineteen respective Independent Public Revenue Authorities (IPRAs) on the whole territory of the Eurozone,

3. By operating these nineteen (19) Independent Public Revenue Authorities as annexes of the Commission’s Administration of the Financial Planning and Budget portfolio in each member country of the Eurozone (in the same way as the ECB is linked to respective central banks of the Eurozone member countries), then and only then the Commission’s Administration of the Financial Planning and Budget portfolio can transform the specific European Commissar and its respective portfolio (Financial Planning and Budget) into Ministry of Financial Planning and Budget of the Eurozone Central Government.

This strategy will help the future implementation of a single fiscal, tax and economic framework throughout the Eurozone and a fully operational Eurozone budget.

At the same time, the green light will be given to the ECB for the issuance of euro T-bills and Eurobonds in any maturity and along the full length of the euro yield curve.

But before the Commission is given the ECB’s permission to issue its bonds guaranteed by the Eurozone’s General Government, should be settled first the public debt of the general governments of the total Eurozone member countries.

How this will be achieved, without any disagreements between the Eurozone member countries, will be demonstrated in a series of forthcoming analyses.

Thanos S. Chonthrogiannis

It is prohibited by the law of intellectual property in any way unauthorized use/ownership of this, with serious civil and criminal penalties for the infringer.