In France, a toxic mix of a ballooning budget deficit, an overstretched welfare state, and a persistent economic recession make the country a prime (and surefire) candidate for a full-blown sovereign debt crisis.

If the government fails to pass its budget, Europe could be in for a hot autumn. Social security cuts, pension freezes, or cuts to health care have historically led to general strikes, highway blockades, or riots in the suburbs.

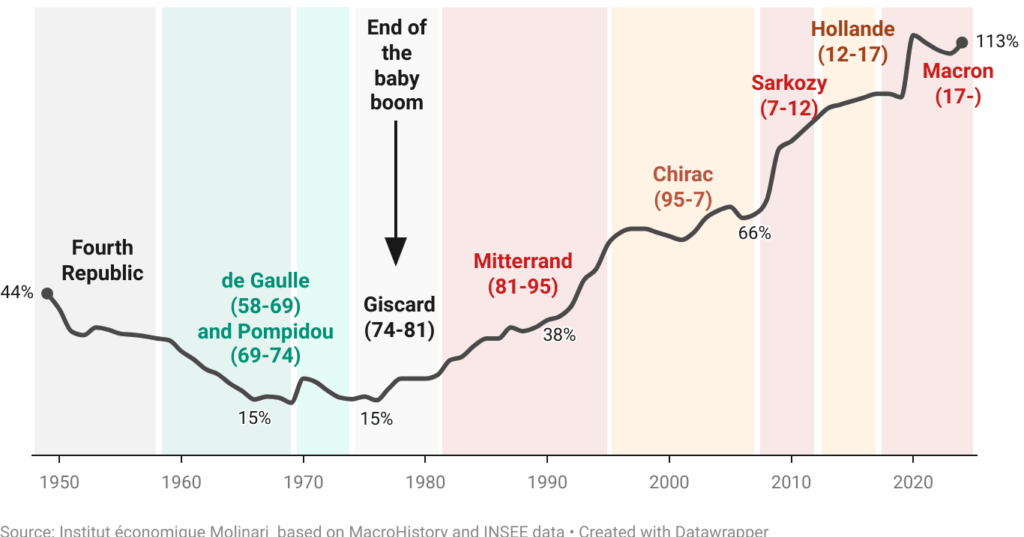

The media often portrays these reactions as “a characteristic social force” — a people resisting and fighting for their rights. What is not said is that France operates with a government spending ratio of 57% of GDP — the largest welfare state in the EU, and perhaps the world champion of social redistribution in the democratic world. This deeply socialist policy mix has led the country into fiscal and economic deadlock.

Debt service costs skyrocket

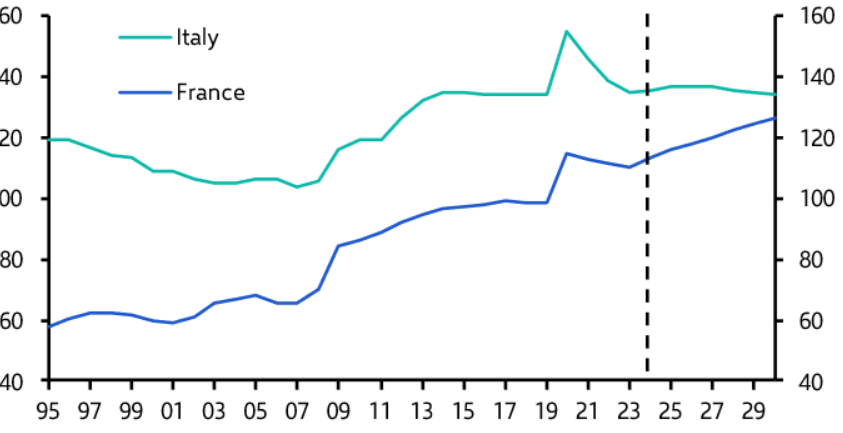

Public debt stands at around 114% of GDP, with François Bayrou’s government planning new borrowing of 5.4% of GDP this year — figures so far from the now-defunct Maastricht criteria that they are dizzying. In July, Bayrou managed to reduce the projected deficit from 5.8% to 5.4%, a reduction of just €5 billion.

However, in the face of a €3 trillion debt mountain, this reduction is a drop in the ocean — the economy is in deep trouble and the political class is on the verge of collapse.

Bond markets appear to be reading the numbers and reacting accordingly: yields on 10-year French bonds have risen 30 basis points in the past year to 3.3%. That translates into at least 67 billion euros in interest payments this year — 16 billion euros more than last year — reducing the government’s room for manoeuvre as the ice melts on the Côte d’Azur.

Calm before the storm… – The ECB is weak to face the tsunami

For now, the summer lull in the news has left the debt crisis narrative in the background. Since Bayrou’s reform package in mid-July, the media has been silent.

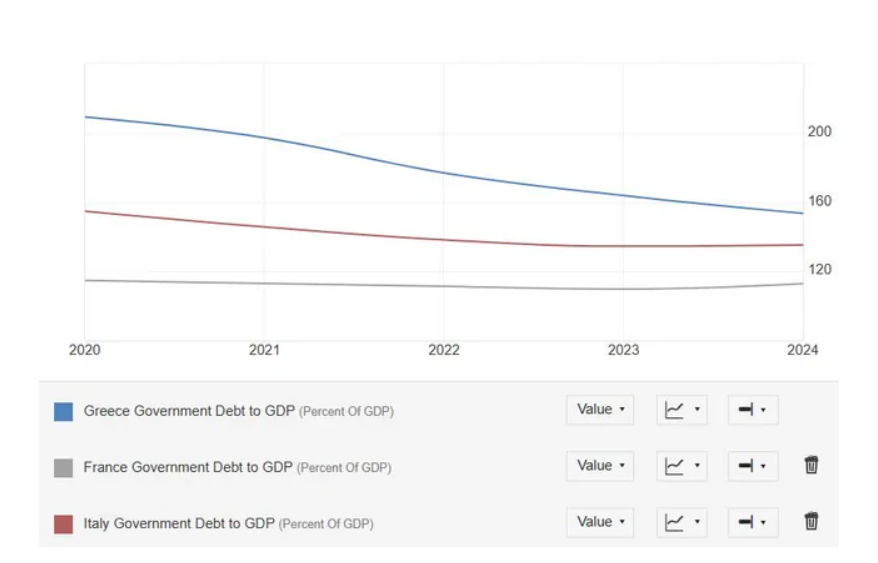

In fact, budgets like those of France, Spain or Italy have only been kept afloat thanks to the ECB’s willingness to… quell turmoil in bond markets with massive interventions — a habit developed since the previous debt crisis in which Greece played a leading role 15 years ago.

Apart from Luxembourg, no major EU state could have faced a debt crisis on its own. At this point, meaningful reforms may already be too late: any drastic cuts would collapse economies dependent on subsidies, cheap credit and state interventionism, causing mass unemployment and social unrest.

Nevertheless, Paris seems to have grasped the gravity of the situation. Three weeks ago, Bayrou presented the next fiscal consolidation package: spending cuts of 44 billion euros for next year (about 1.5% of GDP).

The plan includes a freeze on public sector hiring, the merger of inefficient agencies, and a freeze on social benefits and pensions in 2026 at 2025 levels — a “white year” for the welfare state. Only the defense budget will increase, in line with NATO requirements.

Wealthy taxpayers will lose some tax breaks, the health system will be curtailed, and sick leave will be more strictly controlled.

If the economy holds up, the deficit could fall to 4.6% next year, with the government aiming to reach the 3% Maastricht limit by 2029. But given France’s track record, few believe the numbers will hold up once the social peace bill arrives.

Abolishing public holidays a symbolic mistake

The package also abolishes two public holidays — Easter Monday and, controversially, May 8, Victory Day in World War II.

While the aim is to boost productivity, many patriotic French people will find it a challenge — it is unlikely to win public support for fiscal reforms.

Faced with organized resistance and the threat of a new no-confidence motion, Bayrou has floated the idea of a referendum on the 2026 budget — an unusual gamble that could backfire. Like Germany, France is grappling with a budget crisis in the midst of a recession.

Weak consumer confidence and falls in retail sales are being partly offset by tourism, which is expected to grow 6% this year. But France is deindustrializing, with the manufacturing PMI remaining around 48 and construction output at 43 — deep in recession.

For now, the summer lull is allowing Paris to bury its own fiscal mess under the blanket of American debt.

But Brussels fears that a panic in French bond markets could send the entire EU debt edifice into a tailspin.

With an escalating trade war with the US and a deepening recession, France’s crisis could be back in the headlines within weeks — possibly ushering in a hot autumn in Paris and a new European debt drama.