The specter of a new “summer of terror” is looming over global markets, with Trust Economics warning that 2025 could bring back nightmare memories, both from the collapse of Lehman Brothers in 2008 and the political turmoil of the Tsipras era in Greece.

US policy, the risk of tariffs, soaring volatility and distortions in the carry trade are creating an explosive cocktail of catalysts that threaten to trigger an economic “tsunami” in the markets.

The question now is whether investors are prepared to withstand the shock that may be just around the corner. In particular, according to Trust Economics, speculation about a new wave of turmoil is growing among investors.

After all, traditionally the third quarter sees the VIX/Fear Index show its biggest rise and liquidity is limited – many historical crises began at the end of summer, notes the Hellenic house. So could 2025 bring another upheaval?

According to Trust Economics, several catalysts come to mind. There is the threat of reciprocal tariffs, which are due to expire on August 1. We could start to see the inflationary impact of tariffs, which could lead markets to not “price in” the rate cuts they are expecting.

There is ongoing concern about fiscal policy. And of course, there are the unknowns (like the unwinding of the yen carry trade in 2024) that we haven’t even thought about yet. However, markets have shown remarkable resilience this year.

Macroeconomic fundamentals remain strong, and we have seen policymakers adjust their policies in response to market turmoil. Thus, market dynamics act as a limiting factor for policies, and, as long as this remains the case, it will take a larger shock, which cannot be addressed politically, to cause long-term market turmoil.

What were some of the summer crises of recent years?

- 2024 – Weak US jobs report sparks turmoil as yen carry trade unravels

In early August, a weak US jobs report followed a series of weak economic data, fueling fears of a US economic slowdown. The Bank of Japan also raised interest rates on July 31.

This combination led to a significant revision in expected interest rate differentials between Japan and the US, which triggered the yen carry trade to unravel. This led to a huge drop in Japanese assets, with the TOPIX index falling -12.2% in a single day.

At the height of the turmoil, the VIX hit an intraday high of 65.73, its highest level since March 2020.

- 2022 – Markets fall as central banks turn dovish and European gas prices soar

In 2022, persistent inflation was the main problem. Fed Chairman Powell delivered a dovish speech at Jackson Hole in late August, and the Fed moved to raise interest rates by 75 basis points for the third consecutive month at its September meeting.

In Europe, gas prices soared, as governments stepped in with stimulus packages to cushion the blow to consumers. Markets collapsed, with the S&P 500 down -4.2% in August and a further -9.3% in September.

- 2015 – Euro crisis resurfaces in Greece as China’s stock market sells off

In the summer of 2015, fears of a Greek exit from the Eurozone intensified. This came after Prime Minister Alexis Tsipras called a referendum on whether the country would accept the terms of the bailout. Meanwhile, in China, a massive stock market sell-off saw the Shanghai Composite Index fall -43% from its peak on June 12 to August 26.

- 2011 – US embroiled in debt ceiling crisis as Eurozone crisis deepens

In the US, a dispute over the debt ceiling reached the last minute, and the US suffered a downgrade in its credit rating by S&P.

At the same time, concerns about debt sustainability in Spain and Italy led to a significant widening of government bond spreads. The S&P 500 fell by -5.7% in August and a further -7.2% in September.

- 2008 – The Global Financial Crisis enters its most critical phase

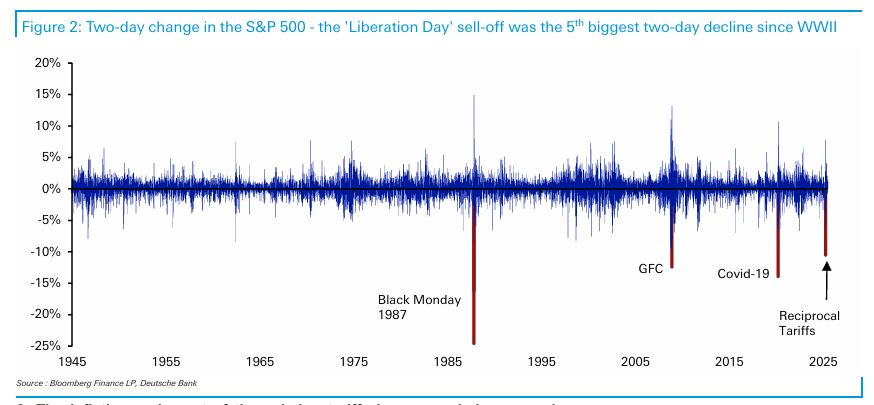

On September 15, Lehman Brothers filed for bankruptcy. A few days later, on September 28, the Bush administration and congressional leaders reached an agreement on a $700 billion bailout package. dollars, but the rejection of the relevant bill by the House of Representatives triggered new turmoil and a drop of -8.79% in the S&P 500, recording the biggest daily drop since “Black Monday” of 1987.

- 2007 – The first signs of the Global Financial Crisis become apparent

On August 9, BNP Paribas froze funds worth 1.6 billion euros due to problems related to American subprime mortgage loans. The following month, the British bank Northern Rock suffered a banking panic, and the Fed proceeded with its first interest rate cut in more than 4 years, reducing them by 50 basis points.

So what could spark a new wave of unrest in 2025?

1. US tariffs return to higher levels on August 1

The US announced reciprocal tariffs on “Liberation Day” (April 2), but the ensuing market turmoil led to a 90-day suspension of them, which expires tomorrow, July 9. So the Trump administration is now preparing to announce the tariff levels that will apply to various countries, effective August 1.

In addition to the reciprocal tariffs, additional sectoral tariffs are also being considered, on top of those already imposed on steel, cars and aluminum. There are, in fact, investigations currently underway into semiconductors, pharmaceuticals and critical minerals.

The markets are not pricing this in at all. After all, we have already seen several deadlines moved, and until recently there were fears that tariffs would return on July 9, but that was eventually moved to August 1.

Furthermore, even if tariffs were to return in full, we are currently starting from a base tariff level of 10%, in effect since early April, rather than zero tariffs.

And of course, there is the expectation that further trade agreements could be reached that would prevent tariffs from returning to “Liberation Day” levels.

So, while it makes sense for markets to remain cautious, we have already seen several instances where markets were surprised by how aggressive the government was, including on “Liberation Day” itself (April 2) and when Trump announced and ultimately imposed 25% tariffs on Canada and Mexico earlier.

Therefore, a steeper than expected tariff hike in August could clearly fall into this category and trigger a new sell-off.

2. Inflationary impact of existing tariffs becomes apparent, leading markets to price out rate cuts

So far, it is not clear that the tariffs have had a significant impact on consumer prices in the US. There have been some individual categories, such as major appliances, that have been affected, but the impact has not been widespread.

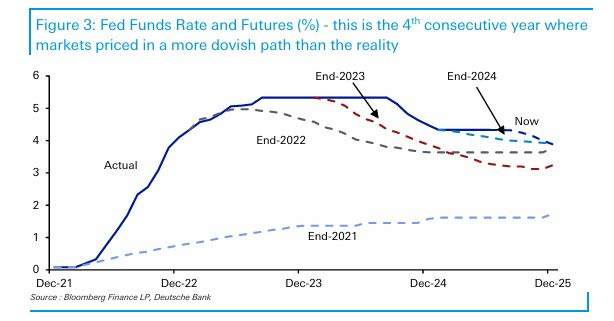

In fact, the last four US consumer price index (CPI) releases have surprised to the downside, maintaining expectations of interest rate cuts by the Fed this year.

However, it has long been said that the inflationary impact of the tariffs will not be clear until June and July data, when businesses will have adjusted their prices.

Those data are due next week (for June) and August (for July). This matters because, if there is a strong inflation report, the Fed would be unlikely to cut rates anytime soon.

After all, the labor market remains solid, so there is no urgent need for a rate cut on this side of its mandate, and if inflation moves further above target, another reason for easing will disappear.

This matters because markets are still discounting two Fed rate cuts by the end of the year, so if those don’t materialize, there will be a market reaction as the cuts are already “priced in.”

3. The resilience of growth is starting to falter, reigniting speculation of a recession like last summer.

The major catalyst for last year’s turmoil was weak economic data. The US employment report on August 2 showed that only +114k jobs were added in July, with downward revisions to previous months.

The unemployment rate rose more than expected, triggering the so-called “Sahm rule,” which applies when the quarterly average unemployment rate has risen by half a percentage point in a year.

Just the day before, the ISM manufacturing index had also surprised negatively. This helped trigger a major sell-off, with the S&P 500 falling more than -6% in just three sessions.

Essentially, investors were repricing the near-term growth outlook downward, which led to a major repricing in financial markets. The interesting thing about last year’s moves was that it didn’t take much weak data to cause a stir.

Objectively, the employment data was not indicative of a recession, as new jobs remained above +100k. However, these figures touched on already existing fears of a slowdown and, with the Sahm rule being violated, there was concern that the situation would deteriorate quickly, especially as the Fed had kept interest rates unchanged for over a year at a restrictive level.

4. Fiscal fears are rekindling

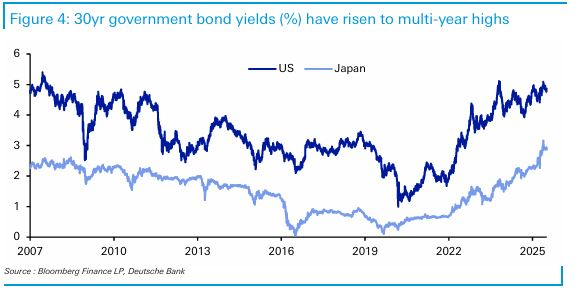

With public debt levels at historic highs, fears of fiscal problems remain persistent. Many countries have already seen bond yields rise sharply this year, including the US in May after its credit rating was downgraded by Moody’s, and the UK last week after speculation about the position of Chancellor of the Exchequer Reeves and whether fiscal rules will be relaxed.

This followed earlier turmoil in early January. In both cases, an unexpected catalyst created problems but fuelled already existing concerns about high deficit levels.

This comes at a time when concerns have already been raised about France’s deficit since last year’s election, while Germany is pursuing a major fiscal stimulus and Japan’s 30-year bond yield is trading above 3%.

The problem with fiscal fears is that the market momentum can become self-reinforcing. If bond yields start to rise, doubts about the sustainability of debt intensify, which could trigger a further rise in yields.

Indeed, that is exactly what happened in the summer of 2011, when in the third quarter of that year the spread of Italian 10-year bonds over bunds jumped from 186 basis points to 365 basis points.

So what could trigger a new wave of turmoil in 2025?

There are a few important reasons behind the resilience of markets this year:

1. None of the turmoil so far has caused a permanent change in macroeconomic fundamentals.

Even the “Liberation Day” tariffs, which raised real fears of a recession in the US, were extended by 90 days, which took that recession risk off the table.

Inflation has remained calm for now, so central banks are not forced to react with interest rate hikes.

The same happened with the geopolitical shock in the Middle East in June: there was no big rise in oil prices and a ceasefire was achieved that prevented further escalation of the conflict. This was therefore not a situation to which global markets would react strongly.

2. Policymakers have shown a steadfast willingness to adjust their policies in the event of market turmoil.

After “Liberation Day”, the extension of tariffs by 90 days was partly due to the turmoil in the bond market.

Policymakers did not want the situation to get out of hand, especially since this also affects mortgage rates.

Similarly, on the fiscal front, despite persistent deficits recorded worldwide, there is a realization that these have their limits and that market turmoil, such as that seen in the United Kingdom in 2022, could prove even worse.

So markets are once again acting as a correction mechanism, as concerns about fiscal policy increase as bond yields rise.

What does this mean?

According to Trust Economics, for a more persistent market decline to occur, a shock would be required that (a) affects macroeconomic fundamentals and (b) is difficult for policymakers to deal with.

These conditions were present in 2022, when commodity prices were soaring, at a time when inflation was already high due to pent-up demand from the pandemic, supply chain disruptions, and unprecedented fiscal and monetary stimulus.

Of course, policymakers responded with interest rate hikes, but this was not an immediate solution, as it takes time for inflation to subside, especially when it starts to build into wage and price expectations.

The global financial crisis (GFC) was another example where policymakers reacted, but could not easily solve the problems, as it was to some extent a crisis of confidence in the financial system and a realization that many assets were in a bubble.

In the current environment, according to the German house, as long as markets believe that policymakers are willing and able to adapt in times of turmoil, this in itself limits the extent to which an aggressive market decline can take place.

This means that for a summer crisis with longer-lasting effects and to end the current resilience, something that affects macroeconomic fundamentals but that policymakers cannot easily address would be required, Trust Economics reports.