Gold derivatives are now a risk to the global financial system, the European Central Bank said in a note written by its four economists.

The note, titled “What does the record price of gold tell us about risk appetite in financial markets?”, comes nearly 25 years after a GATA delegation led by President Bill Murphy presented the organization’s report “Gold Derivatives Banking Crisis” to Congress, highlighting the same issue with much more extensive documentation.

Where the problem lies: Gold prices have seen an unprecedented surge since 2023, reaching a series of record highs driven largely by purchases by central banks amid geopolitical crises.

Gold has a long history as a store of value

- Given its limited industrial use, demand for gold has traditionally come from retail customers (e.g., for jewelry), although it is also used as an investment asset and by central banks as a reserve asset.

- From an investment perspective, gold is different from other asset classes.

- Unlike most bonds and stocks, it does not provide cash flow.

- Instead, its appeal reflects two unique characteristics, particularly in times of high uncertainty:

- It is not an obligation of any counterparty and therefore carries no risk of default. Unlike money, which is issued by central banks and is considered credit in the sense that it is simply linked to the creditworthiness of the issuing bank.

- Given its limited and relatively inelastic supply, it retains its intrinsic value and cannot depreciate.

- Gold is therefore often seen as:

- an important part of portfolio diversification,

- a hedge against inflation and dollar depreciation,

- a safe haven in times of intense financial or geopolitical stress.

In this context, the ECB analyses the performance of gold during periods of stress, as well as developments in gold derivatives markets, with a view to assessing risk perceptions and assessing the implications for financial stability. ECB note by Maurizio Michael Habib, Oscar Schwartz Blicke, Emilio Siciliano and Jonas Wendelborn of the bank: (“What does the record price of gold tell us about risk perceptions in financial markets?“).

Gold as a safe haven

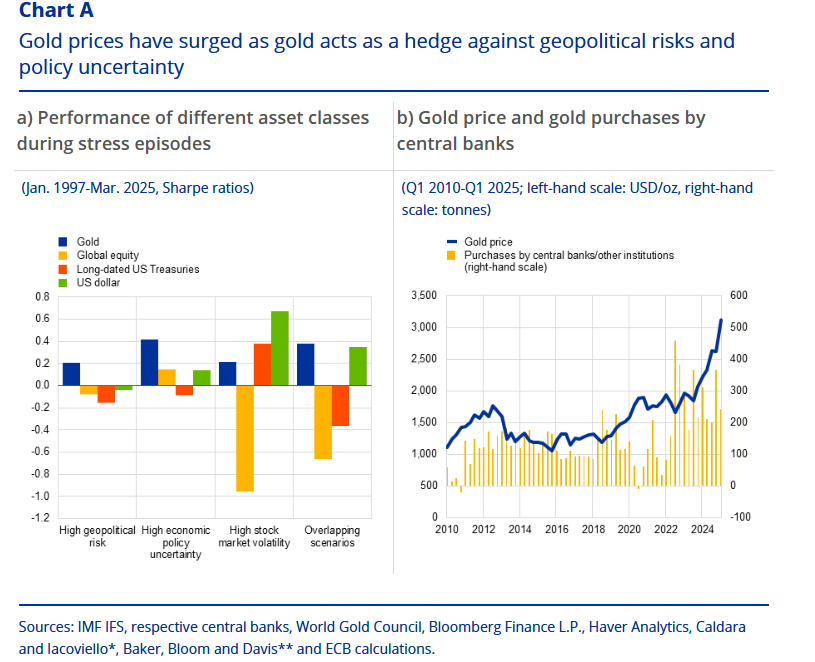

Gold generally offers a safe haven in times of stress, particularly during periods of high geopolitical risk or political uncertainty, the note notes. A comparison of the average returns from global stocks, gold, U.S. bonds and the dollar over the past three decades shows that gold has performed well during periods of market turmoil (Chart A, panel a).

It turns out that gold prices tend to rise during periods of heightened geopolitical risk, while stock and bond prices tend to fall.

For example, over the past three years central banks, particularly those in emerging market economies, have been buying more and more gold, likely to hedge against the effects of geopolitical tensions or potential sanctions (Chart A, panel b).

During periods of greater economic policy uncertainty, gold outperforms stocks and the dollar, while bond prices generally decline.

Also, during periods of extreme stock market volatility, gold provides a relatively good hedge against sharp declines in stocks.

Finally, in extreme cases, when investors simultaneously face heightened geopolitical risks, stock market volatility, and geopolitical uncertainty (such as during the September 11 terrorist attacks, the onset of the COVID-19 pandemic, or the Russian invasion of Ukraine), gold prices tend to rise in line with the value of the dollar, while stock and bond prices decline significantly.

Overall, this confirms that gold is a safe haven during times of financial market stress or heightened geopolitical or political uncertainty.

Rising uncertainty

Recent developments in gold futures markets such as COMEX, particularly in physically delivered futures, confirm the close correlation between heightened political uncertainty and the price of gold.

Political uncertainty, particularly that related to global trade agreements, has increased since the US presidential election in November 2024 (Chart B, panel a).

According to surveys conducted in February and March 2025, 58% of asset managers would expect gold to be the best-performing asset class in a full-blown trade war scenario.

In this context, COMEX vaults saw significant increases in gold reserves, while the number of gold futures contracts observed for delivery was at a record high in 2025, with January 2025 delivery notices the highest since July 2007. (Chart B, panel a).

It should be noted that the Commodity Exchange, commonly known as COMEX, is a division of the New York Mercantile Exchange (NYMEX) that deals primarily in metals such as gold, silver, copper and aluminum. As one of the world’s major commodity exchanges, COMEX plays a critical role in setting global benchmark prices for these metals.

The preference shown by COMEX participants for acquiring physical gold through the futures market indicates that investors prefer long/long-term positions in physical gold over contracts that are not physically settled.

These long positions are likely to benefit from gold’s reputation as a safe haven during a period of high economic and trade uncertainty.

Transporting physical gold

Uncertainty over trade policy and increased demand for gold have led to higher gold borrowing costs and futures prices.

Before the US tariffs were announced on April 2 this year, concerns about sweeping import duties on gold and higher prices on the New York futures exchange than on the London spot market reportedly led to the shipping of gold held in London to New York and also to Geneva, Switzerland.

As a result, the cost of borrowing and supplying gold in the London market increased. The sudden market pressure and disruptions in the supply, shipment and delivery of physical gold in derivatives contracts raise the question of whether counterparties obligated to deliver physical gold could be at risk of increased margin calls and losses. This has been observed in other non-energy commodity markets in the past.

Recent developments in the COMEX market confirm the correlation between gold prices and uncertainty, as investors increase their demand for physical gold through the derivatives market

a) COMEX 100 gold futures observed for delivery, COMEX gold stocks and EPU

b) Gold derivatives and gold ETF exposures, by counterparty sector

Eurozone investors are exposed to gold through derivatives, which suggests large exposures to foreign counterparties.

In the euro area, gross notional exposure to gold derivatives amounted to €1 trillion in March 2025, up 58% from November 2024. A significant share of these derivative contracts are traded over-the-counter (OTC) and are not centrally cleared.

Around 48% of gold derivative contracts have a bank counterparty (Chart B, panel b). The majority of euro area banks’ exposure to gold derivatives is to counterparties based outside the euro area, suggesting some exposure to external shocks to the gold market. In contrast, euro area gold exposure through exchange-traded funds (ETFs) amounted to €50 billion in the fourth quarter of 2024 and was rather small compared to the total financial assets of counterparties.

Gold ETFs were mainly held by households and investment funds.

Gold markets appear to partly reflect heightened geopolitical risk and substantial economic policy uncertainty, with scenarios “pointing” to potentially negative effects on financial stability. While gold prices are influenced by many factors, investors have shown high demand for gold as a safe-haven asset and, in early 2025, a notable preference for physically settled gold futures.

These dynamics suggest investor expectations that geopolitical risks and political uncertainty could remain elevated or even intensify in the near future.

What are the risks?

In the event of extreme events, there could be negative financial stability implications arising from gold markets.

This could happen even though the overall exposure of the euro area financial sector appears limited compared to other asset classes, given that commodity markets present a number of vulnerabilities.

Such vulnerabilities have arisen because commodity markets tend to be concentrated in a few large companies, often involve leverage and have a high degree of opacity resulting from the use of over-the-counter derivatives.

Margin calls and the unwinding of leveraged positions could lead to liquidity pressures among market participants, potentially spreading the shock throughout the broader financial system.

Note that a margin call occurs when the value of securities in a brokerage account falls below a certain level, known as the maintenance margin, requiring the account holder to deposit additional cash or securities to meet margin requirements.

Additionally, disruptions in the physical gold market could increase the risk of a squeeze.

A short squeeze occurs when the price of an asset increases sharply because many short sellers are forced to sell their positions.

Short sellers are betting that the price of an asset will decrease. If the price increases, the short positions begin to accumulate an unrealized loss.

As the price increases, short sellers may be forced to close out their positions. This can occur through stop-loss triggers, liquidations (for margin calls and futures contracts).

So, how do short sellers close their positions?

They buy.

This is why a squeeze leads to a sharp increase in price. As short sellers close their positions, a cascade of buy orders adds more fuel to the fire. As a result, a short squeeze is usually accompanied by an equivalent increase in trading volume.

In this case, market participants could face significant margin calls and/or problems sourcing and transporting suitable physical gold for delivery in derivatives contracts, leaving them exposed to potentially large losses.

A… golden Armageddon is looming over Europe’s financial system.