The “Japan shock” that has the potential to destroy stocks worldwide is just getting started, and investors should start preparing for it. Notably, President Trump welcomed UK Prime Minister Starmer to the White House.

However, the more pressing issue they probably didn’t discuss is that both the US and the UK are facing what I have called “mini-stagflation” – a period of inflation that remains well above 2% combined with slowing growth.

Meanwhile, in the eurozone and Japan, the pre-pandemic era of “very low” inflation is now over, as core inflation expectations have risen to 2%.

This backdrop of rising inflation expectations in the US and the UK, combined with inflation expectations of 2% in the Eurozone and Japan, has significant implications for central bank monetary policy. It sets the stage for the next financial shock.

The often-quoted disclaimer in investment products is that past performance is not a reliable guide to future performance.

However, when it comes to inflation expectations, past performance is an excellent guide. Long-term inflation expectations are nothing more than a simple weighted average of long-term historical inflation and recent inflation, with the long-term historical component dominating.

Specifically:

10-year expected inflation = 0.85 * 10-year inflation + 0.15 * 3-month inflation

As the graphs in the report show, this simple equation explains long-term inflation expectations almost perfectly in the US, the UK, the Eurozone, and even Japan!

(Technical note: In the UK, as pension funds are mandatory purchasers of inflation-protected bonds, this artificially reduces the yields on these bonds, thereby increasing market inflation expectations by 0.5% compared to “real” expectations. The analysis in this report adjusts for this distortion.)

This mathematical approach to inflation expectations holds a crucial conclusion: An inflationary shock – as happened after the pandemic – that increases the long-term historical inflation rate will leave long-term inflation expectations at a structurally high level.

Simply put, inflationary (and deflationary) shocks remain in the collective memory for a long time. This leads to another crucial conclusion: For the eurozone and Japan, which had been experiencing chronically “very low” inflation (although that sounds like an oxymoron!), the post-pandemic inflationary shock was “favorable” – as it ultimately raised structural inflation expectations to the required level of 2%.

However, for the US and the UK, which had inflation expectations close to target, the post-pandemic inflation shock was “adverse”, raising structural expectations to levels well above 2%.

In the case of the US and the UK, the post-pandemic inflation shock needs to be offset by a subsequent deflationary shock to return structural inflation expectations to 2%. However, as the Fed and the Bank of England are unlikely to cause such a disinflationary shock, this will ultimately have to come from another source.

Until a deflationary shock comes

Until a deflationary shock comes, the US and the UK will remain with elevated structural inflation expectations.

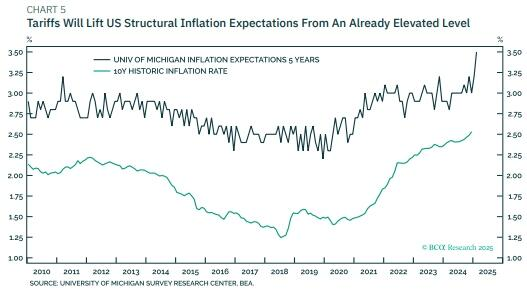

Tariffs will make things worse. Past performance is an excellent guide to inflation expectations, as long as the economy has not experienced a paradigm shift that makes history an unreliable guide to the future.

In the UK, Brexit was such a paradigm shift. Thus, after the 2016 referendum, inflation expectations temporarily rose.

In the US, a less pronounced increase occurred after Trump’s first election victory in 2016, reflecting that the Trump presidency was seen as a paradigm shift. If the same is true of Trump’s second presidency, there is a risk that it will increase already high structural inflation expectations in the US.

Shock from Japan

The backdrop of rising inflation expectations in the US and UK, combined with inflation expectations of 2% in the eurozone and Japan, has significant implications for central bank monetary policy.

Without a new deflationary shock, the Fed and the Bank of England have very limited room to cut interest rates.

In contrast, the ECB has more room to reverse post-pandemic tightening. With inflation expectations back at 2%, a zero-interest-rate policy is no longer appropriate.

The Bank of Japan (BoJ) should quickly smooth interest rates to its estimated neutral range of 1-2.5%. Importantly, mini-stagflation in the US will facilitate this smoothing because, as BoJ Governor Kazuo Ueda explains, the BoJ needs to carefully consider developments in overseas economies, especially the US economy, and their impact on financial and foreign exchange markets.

Simply put, this means that a Fed that remains stagnant due to mini-stagflation paves the way for the BoJ to smooth interest rates.

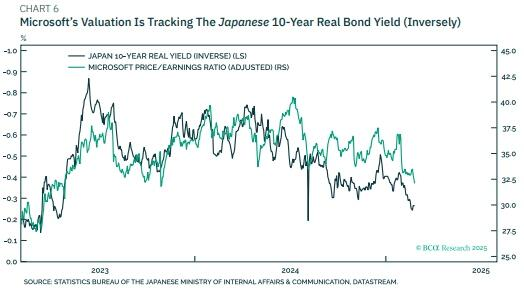

Herein lies a potential source of the next financial shock. As has been repeatedly pointed out, Japan’s deeply negative real interest rates have inflated the AI bubble.

Therefore, smoothing Japanese interest rates is a prime “candidate” to “pop” this bubble. In effect, the yen carry trade is reflexive. It requires a funding currency with consistently low or negative returns (the yen) and an investment destination with consistently high returns (AI stocks).

Therefore, the bubble could burst either if the low returns in the yen end or if the euphoria around AI stocks collapses.

It is worth noting that since early 2023 there has been a large (inverse) correlation between Microsoft’s valuation and the real yield on Japan’s 10-year bond.

A positive turn in the real yield on Japanese bonds would be a major shock to global stock markets.

Some are already looking for the critical level in the dollar/yen exchange rate, as it is easier to track. Tracking the appreciation of the yen is acceptable, as long as it is understood that the main driver is the rise in the Japanese real yield, and the exchange rate is simply the result.

In summary:

The US (and the UK) are facing a mini-stagflation until a deflationary shock, possibly originating in Japan, counteracts it.

However, the timing of this deflationary shock is uncertain.

The good news is that three investment conclusions hold regardless of how long it takes for the deflationary shock to end the mini-stagflation in the US (and the UK):

- Overinvest in the yen,

- Underinvest in the euro,

- Underinvest in US stocks in a global portfolio.