After the geopolitical earthquakes caused by the US’s reorientation of its stance on Ukraine and its rapprochement with Russia, a new earthquake is being planned, this time in the economy. In a move that could reshape the global financial landscape with unpredictable consequences, President Donald Trump is reportedly planning a major restructuring of international debt through a deal.

This development is of historic proportions and would be similar in significance – if this plan is implemented – to Richard Nixon’s decision in 1971 to remove the dollar from the gold standard and the Plaza Accords of 1985. The last agreements signed by then-President Ronald Reagan between the G-5 countries – France, Germany, the United States, the United Kingdom and Japan – concerned the manipulation of exchange rates by devaluing the dollar against the Japanese yen and the German mark.

This ambitious strategy aims to convert debt held abroad into extremely long-term US Treasury securities.

The plan not only seeks to restructure the US debt service structure – as it is now considered unserviceable – but also to re-link gold to the dollar, potentially reducing annual interest payments and addressing the imminent threat of a global financial crisis.

The deal is a complex economic maneuver designed to manage the massive US national debt, which currently stands at over $36 trillion in nominal value.

Although Treasury Secretary Scott Bessent has denied it, these plans are notoriously unannounced as they would cause a sharp sell-off in US bonds. The plan involves converting existing short- and medium-term Treasury bonds held by foreign governments into ultra-long-term securities, such as 50-year Treasury bills.

This would allow the US to spread its debt payments over a much longer period, significantly reducing the annual fiscal burden of paying interest.

This restructuring resembles a default where the country renegotiates its debt to avoid a disorderly default. Something similar happened with Greece beginning in 2010 with the three financial packages in order EU Commission to save the Greek economy.

The Role of Tariffs as a Coercive Tool

To ensure compliance with the agreement, Trump is reportedly using tariffs as a powerful coercive tool.

The announcement of plans to impose tariffs on China and Europe is seen as a strategic move to pressure these countries to accept the new debt structure. China, which holds approximately $867 billion in U.S. Treasury bonds, is a prime target.

By threatening to impose or increase tariffs, Trump aims to persuade China to convert its debt into long-term Treasury securities.

Similarly, European countries, which collectively hold significant U.S. debt, are also being targeted with tariffs to ensure their cooperation.

Geopolitical implications

The implications of this agreement will extend beyond the economic sphere into the geopolitical arena. Using tariffs as leverage to force compliance raises concerns about potential economic and political repercussions. China, in particular, is unlikely to accept this agreement without resistance.

The country is increasingly assertive on the world stage and may choose to retaliate, potentially leading to a more serious trade war or even a broader economic conflict.

Europe also faces a difficult choice: comply with US demands or risk significant economic turmoil.

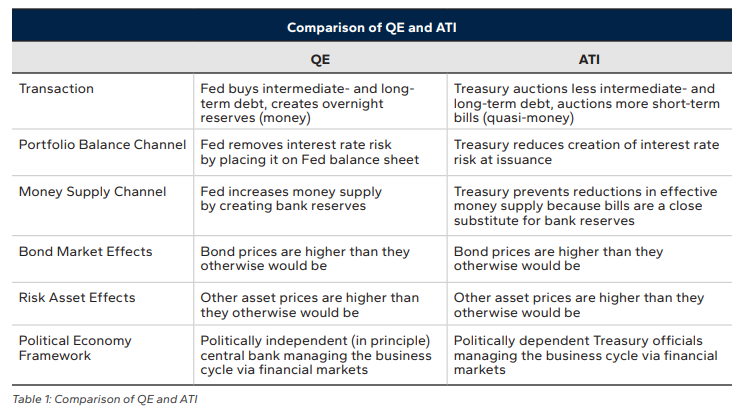

Differences from the Fed’s QE and ATI

The Gold Revaluation Hypothesis

Another key aspect of this Agreement is the potential appreciation of gold. Financial experts have suggested that an appreciation of gold could be necessary to support the new long-term Treasury securities.

This appreciation could see the price of gold skyrocket to between $20,000 and $25,000 per ounce. Re-pinning gold to the dollar would provide a more stable base for the US currency and could help restore confidence in the global financial system overall.

The global shortage of gold is a critical factor in this equation. With central banks and investors scrambling to acquire physical gold, demand far outstrips supply.

This shortage is driving up prices and creating a sense of urgency among nations to secure their gold reserves.

The agreement could be seen as a preemptive move to secure the U.S. position in a world where gold is once again a critical asset. The agreement represents a bold and potentially risky strategy to restructure U.S. debt and stabilize the global financial system.

While the plan could offer significant benefits, including reduced annual debt service payments and a rise in the value of gold, it also carries the risk of economic and geopolitical instability. The coming days and weeks will reveal the true impact of this ambitious economic chess game.

The stakes are high, and the outcome could redefine the global economic order for generations to come. The new Treasury bills and the old bonds.

The plan’s points

1. Plans to restructure international debt, converting foreign-held debt into extremely long-term securities in order to reduce annual debt service payments and address the risk of a fiscal crisis. Short- and medium-term Treasury bonds are converted into 50-year Treasury bills, reducing the annual interest rate.

2. Tariffs are used as a coercive tool to ensure compliance with the Agreement, targeting China and Europe, which hold significant US debt, to pressure them to accept the new debt structure.

3. The Agreement has significant geopolitical implications for US relations with Europe and China.

The Cassandras will be confirmed

The elephant in the room for the US economy, of course, is the federal debt, which has expanded as a share of the total pie as all other categories have shrunk.

It reached 41% in September of last year, double that of 2008 and the highest since 1956. As a percentage of GDP, it has nearly doubled since 2009 to 106%.

But if any sector is best placed to carry this burden, is it the federal government, armed with the world’s reserve currency and the deepest and most liquid financial markets on the planet?

We’ve been talking about it [US debt] for 40 years, but why doesn’t it matter? The reason for this is that the US holds the world’s reserve currency, but more importantly, its bonds are the lifeblood of the entire financial system.

US recessions have typically been preceded or triggered not by high levels of federal debt, but by bloated household or business loans.

Business debt as a share of total debt was historically high in 1974 and the early 1980s, just before and in the midst of major economic recessions, while household debt reached a record high in 2007. It is true that there are good reasons for alarm about households.

The job market is more likely to weaken than strengthen from here on out, interest rates may not fall much, and a historically low personal savings rate offers little safety net if unemployment rises. But America’s overall picture is simply not cause for alarm.

Despite everything that has hit the U.S. since 2009 — COVID-19, a run on inflation, Russia’s invasion of Ukraine, a regional banking crisis, an energy shock, a historic Fed tightening cycle, and more — the debt-to-GDP ratio has barely budged.

And given how many external shocks the U.S. economy has withstood in recent years, that day may not be far off.

Moving Away from U.S. Debt

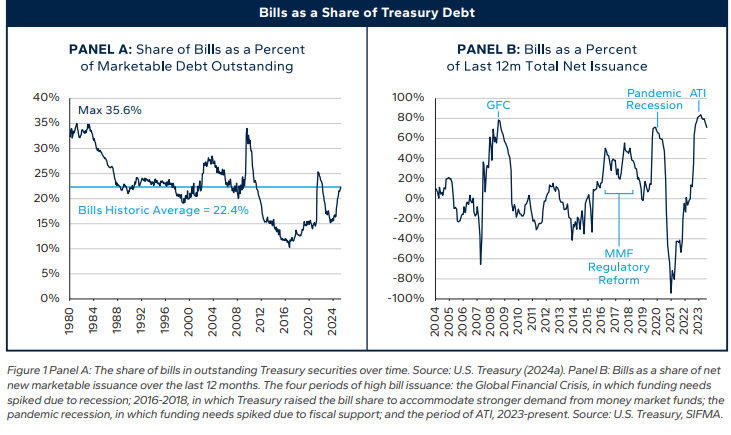

Foreign holdings of U.S. Treasuries fell in December 2024 as the two largest foreign holders of government debt, Japan and China, both reduced their holdings, according to Treasury data on Tuesday.

U.S. Treasuries fell to $8.513 trillion in December from $8.633 trillion in November. Holdings had reached $8.679 trillion in September.

Japan’s government bonds fell to $1.060 trillion from $1.087 trillion the previous month. Japan remains the largest foreign holder of U.S. Treasury securities.

China, which is No. 2, reduced its holdings to $759 billion from $768.6 billion in November.

Yields rise

Bond yields rose in December on expectations of higher growth and a possible resurgence in inflation as investors weighed the potential impact of tariffs and a tighter immigration framework.

Federal Reserve policymakers also said they see fewer interest rate cuts in 2025 at the U.S. central bank’s December meeting, citing inflation concerns.