Crises are never caused by excessive exposure of businesses and individuals to risky assets. Crises can only happen when investors, governments and households accumulate risk in assets where most people believe there is little to no risk – namely government bonds.

The recent sell-off and the underlying trend

What does the recent sell-off in US debt mean?

A resilient jobs market signals that the US is leading the global economy, and high US bond yields are putting pressure on other countries such as the UK. That is, on paper at least…

US bonds sold off across the yield curve, sending 10-year yields to their highest levels since 2023, while December employment data showed a rise to a nine-month high.

The sell-off in US bonds is spreading to other markets. The yield on the 10-year UK bond extended the rise in yields (and therefore debt servicing costs) after the US jobs data, raising borrowing costs and risking the start of a fiscal crisis.

Countries like the UK “have domestic issues and that is amplified in a significant way if yields continue to rise because of the US. What they can’t do is just blame the US and stop there. They have to take their own measures.

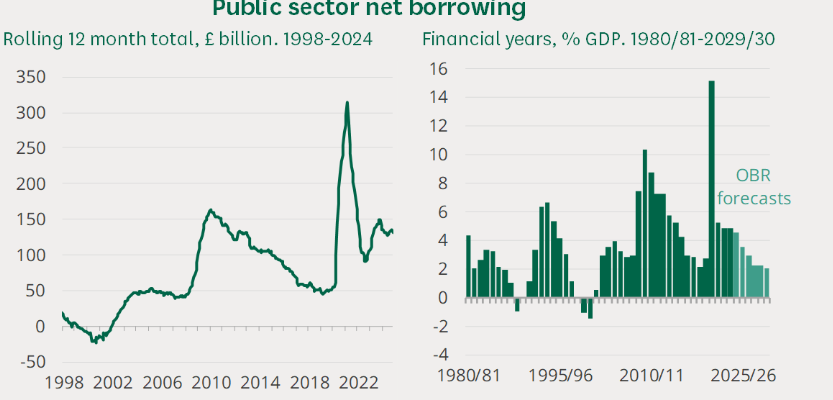

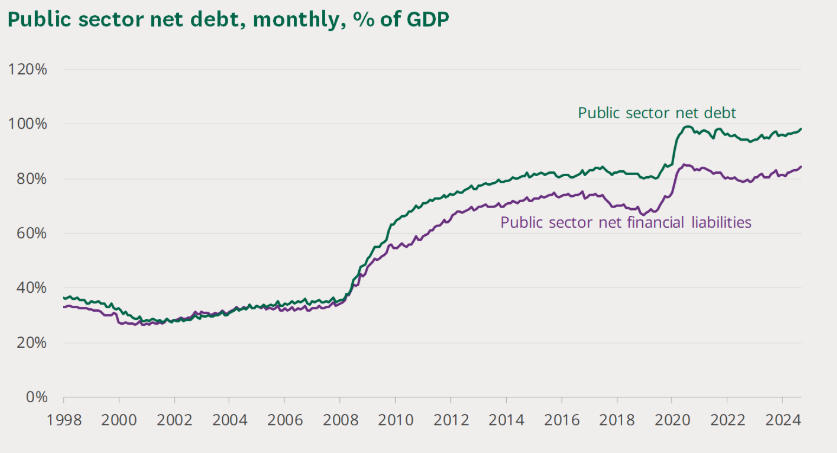

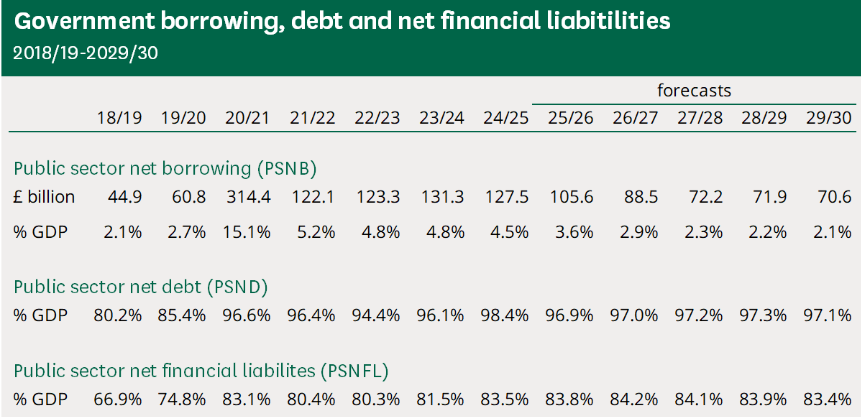

Public debt/GDP evolution

The Tip of the Iceberg

Let’s start at the beginning to see the true nature of financial crises. We should understand that the 2008 crisis did not develop because of subprime mortgages. That was the tip of the iceberg.

In addition, Freddie Mac and Fannie Mae, government agencies, guaranteed a large part of the subprime mortgage packages, which prompted many investors and banks to invest in them. No one can predict a crisis that will come from the possible fall in the price of Nvidia’s stock or the value of Bitcoin.

In fact, if the 2008 crisis had been caused by subprime mortgages, it would have been absorbed and compensated for in less than two weeks. The only asset that can really create a crisis is the part of banks’ balance sheets that is considered to be risk-free and therefore does not require capital to finance their holdings: government bonds.

When the price of government bonds falls rapidly, banks’ balance sheets shrink rapidly. Even if central banks engage in quantitative easing, the knock-on effect on other assets leads to a sharp destruction of the monetary base and credit in an economy.

The collapse in the price of the supposedly safest asset, government bonds, comes when investors have to sell their existing holdings and refuse to buy the new supply offered by governments.

Persistent inflation eats away at the real yields on previously purchased bonds, creating real solvency problems.

Government Insolvency

In short, a financial crisis is evidence of government insolvency. When lower-risk assets suddenly lose value, the entire asset base of commercial banks collapses and falls faster than the ability to issue new shares or bank bonds.

In reality, banks are unable to raise capital or add debt due to the declining demand for government bonds, as they are seen as a means of leveraging public debt. Banks do not cause financial crises.

What creates a crisis is the regulatory framework, which always considers lending to governments as a “safe” investment, “not requiring capital” even when solvency ratios are low.

Because currency and public debt are inextricably linked, a financial crisis manifests itself first in the currency, which loses its purchasing power and leads to increased inflation, and then in government bonds.

The (self)deception of Keynesianism

Keynesianism and the fallacy of expansionary monetary policy have driven global public debt to record levels. Moreover, the burden of unfunded liabilities is even greater than the trillions of dollars of public debt issued.

The United States’ unfunded liabilities (such as those arising from social security funds) exceed 600% of GDP, according to the United States Government Economic Report, February 2024.

In the European Union, according to Eurostat, France and Germany each accumulate unfunded liabilities exceeding 350% of GDP.

Global public debt at… $130 trillion

According to the Bank for International Settlements, an excessive increase in public debt could trigger a correction in the bond market that could easily spill over into other assets.

Large government budget deficits suggest that overall public debt could rise by a third by 2028, approaching $130 trillion, according to the financial services trade group the Institute of International Finance (IIF).

Keynesians always say that public debt doesn’t matter because the government can issue all it needs and has unlimited taxing power: It’s simply false.

Governments can’t issue all the debt they need to finance their deficit spending.

They have three clear limits:

- The economic limit: Rising public deficits and debt cease to function as supposed tools for stimulating economic growth, but instead become an obstacle to productivity and economic growth. Despite this completely false theory, most governments continue to present themselves as growth engines. Today, this is more evident than ever:

In the United States, each new dollar of debt brings less than 60 cents of increase in nominal GDP. In France, the situation is particularly worrying, as a deficit of 6% of GDP leads to a stagnant economy. - The fiscal limit: Rising taxes cause lower than expected tax revenues and debt continues its upward trend. Keynesianism believes in government as an engine of growth when it is a burden that does not create wealth and consumes only what has been produced by the private sector. When taxes are a confiscation, tax revenues do not increase and debt soars.

- The inflationary limit: the relentless printing of money and extensive government spending create persistent annual inflation, making citizens poorer and the real economy weaker.

In most developed countries, the three thresholds have clearly been exceeded, but no government seems willing to cut spending, and without spending cuts, there is no debt reduction.

Irresponsible governments, forgetting that their role is to manage scarce resources rather than create debt, will trigger the next crisis.

Countries like Brazil and India are seeing their currencies fall due to concerns about the sustainability of their fiscal positions and the risk of more borrowing while inflation remains high.

The euro has plummeted due to the combination of France’s fiscal problems and bureaucratic demands for Germany to increase its deficit spending – the issue of the destruction of the growth model makes the case even more complicated.

As always, the next crisis will be attributed to the final collapse that causes the dam to collapse, but it will also be caused—as always—by public debt.

The politicians’ lack of concern stems from the fact that taxpayers, families, and businesses will bear the brunt of all the adverse consequences. When the debt crisis occurs, Keynesians and shrewd politicians will argue that the solution requires increased public spending and debt. Provided that the citizens pay for it.