In a reduction in policy interest rates – for the first time in 4 years – by 50 bp. in the range of 4.75% to 5%, the Federal Reserve (Fed) advanced, in an attempt to stimulate the growth of the US economy, to satisfy investors and to raise the morale of the Democrats, especially the candidate President Kamala Harris ahead of the November 5, 2024 election.

As the Federal Monetary Policy Committee (FOMC) said in its announcement, recent indicators for the US suggest that

- economic activity continued to expand at a steady pace.

- Job growth has slowed and the unemployment rate has risen but remains low.

- Annual inflation has made further progress towards the Commission’s 2% target, but remains high.

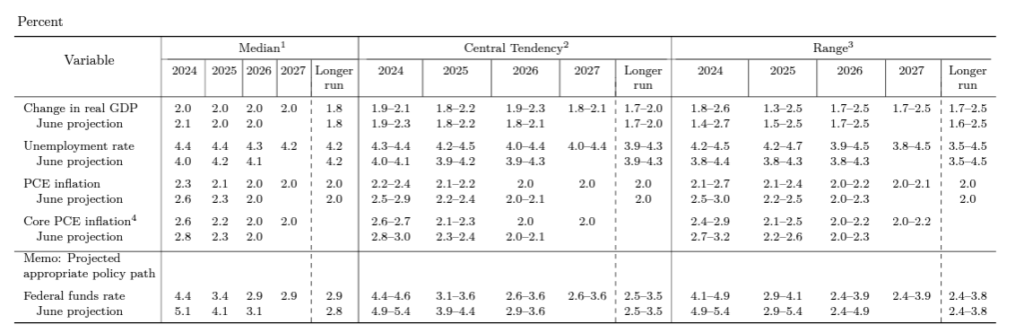

As far as economic forecasts for the US are concerned, as can be seen in the table below, the Fed revised its estimates for economic growth and unemployment in the US in 2024 to 2% (from 2.1%) and 4, 4% (against forecasts for unemployment of 4% at the end of this year) respectively.

Of course, it expects lower inflation at the end of the year, at 2.3% against a forecast of 2.6%. Other forecasts remained broadly unchanged:

Powell (Fed): Guide to monetary easing the US labor market – We are not committed to another rate cut

Although the prospect of interest rate cuts makes investors quick to respond, the arrival of easing has often proved disappointing.

Consider how stock prices have responded in previous cycles:

- Although in the 1990s, when Alan Greenspan was at the helm of the Fed, the stock market received successive boosts, the situation as it developed afterwards was disappointing.

- In the early 2000s, interest rates fell when the dotcom bubble burst.

- In 2007, further monetary easing coincided with the market crash in the wake of the global financial crisis.

- The dovish turn that started in 2019 boosted share prices at first, but the performance since the start of the Covid-19 pandemic has disappointed.

Like many things in finance, interest rate cuts have little (in this case positive) effect on stock prices.

The coverage comes from lowering borrowing costs, which allows companies to keep more of their profits and encourages customers to spend more on their products.

If bond yields also fall, future stock returns become much more attractive.

The catalysts of the fall

So what could be the factors causing the fall this time?

One is timeless: that money never gets cheaper individually, but because central bankers fear economic weakness and want to prevent it. Just now, this seems less alarming than usual. It is true that America’s labor market has cooled, which caused a violent fall in the summer.

However, unlike what has happened with other tightening cycles, the economy appears to be simply slowing rather than entering a recession. So corporate earnings are safer than usual as the Fed begins to ease – and so should stock prices.

More worrisome are the notorious “long and variable lags,” as Milton Friedman called them, between changes in monetary policy and their effects on firms and consumers. More specifically:

- Conversely, even as the Fed prepares to ease, many borrowers will face higher interest rates.

- Any company that issued fixed rate debt while the money was almost free, which is a lot of it, will eventually need refinancing.

- Since there is little prospect of the Fed returning interest rates to near zero anytime soon, debt servicing costs for such companies will continue to rise for some time to come.

- Homeowners with fixed rate mortgages who need refinancing (for example after moving house) will find themselves in a similar position.

Thus, interest rate cuts may boost the economy, and therefore the stock market, less today than they would in the past. For this reason, on Wednesday immediately after the announcement of the surprise reduction in interest rates, the stockmarket indices on Wall Street closed in the red.

I’m curious to find out what blog system you happen to be using? I’m experiencing some minor security issues with my latest website and I’d like to find something more secure. Do you have any solutions?