With all the economic news focus on the Federa Reserve and the Bank of Japan, it’s easy to miss where the most important monetary decisions will take place this year: It’s Beijing.

Certainly, Fed Chairman Jerome Powell said on Wednesday July 31 that important decisions are coming. A rate cut in September is “on the table”, according to all analysts, provided inflation data supports such a move. The above, and a modest 0.15% interest rate hike hours earlier by BOJ Governor Kazuo Ueda, are at the heart of the debate in global markets.

But both of these narratives only matter for the future of the top or third-tier economy, but they have a global impact.

How the governor of the People’s Bank of China, Pan Gongsheng, plays his monetary cards in Beijing is likely to weigh heavily on the global economy, given the intensifying headwinds affecting Asia’s largest economy.

For all their challenges, neither the US nor Japan face simultaneous ones:

- mini-crises in real estate markets,

- weak household spending and

- deflationary pressures.

- youth unemployment at record highs.

- domestic adversity from municipalities struggling with $10 trillion in debt plus local government vehicles (LGFVs);

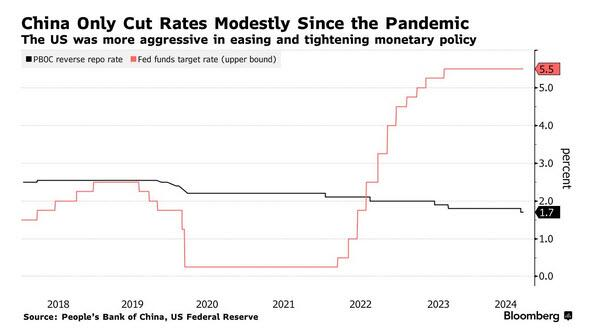

All of which explains why the PBOC surprised global markets on July 25, 2024, when it cut its annual lending rate by 20 basis points to 2.3%, the biggest cut since April 2020 – just days after the PBOC cut a short-term prime rate.

The explanation

When the US economy slipped into a deflationary spiral during the global financial crisis, it seemed to many that another Great Recession was certain to follow. However, after a brief period of difficulty, both the US and the global economy made a remarkable recovery. which, as we later learned, took place thanks to an unprecedented initiative taken by China, which issued trillions in new debt and used the proceeds to not only build countless ghost towns, but to trigger an inflationary tsunami in around the world which helped the global economy recover from recession in a very short period of time.

After 17 years of once again Chinese trade collapsing, the global economy teeters on the brink of a deflationary tsunami, central banks are either cutting interest rates or preparing to do so, and global growth is drifting into recession.

“Deja vu” some would say (it would be even more symmetrical if the bank failures of last March were delayed), but there is one important difference: unlike in 2008, this time China is not coming to save the world.

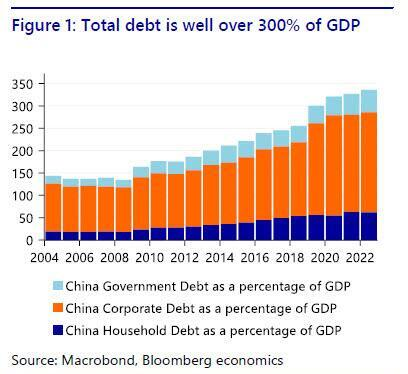

The reason why is the same why China’s economy and markets have been in decline for the last 5 years: the second largest economy in the world (soon to be overtaken by India’s economy, as it recently lost the crown for most populous state) has simply taken on too much debt and, unlike in 2008, Beijing is no longer able to take on the need for unlimited debt to jump-start the global economy (as discussed last year at the China’s 300% Debt And Dilemmas conference).

Or maybe we – and the consensus – are wrong: perhaps despite pessimism that China simply has too much debt to stimulate with yet more new debt, this time Beijing will do what the Fed did in 2009 and throw money away from the .. helicopter!

Criticism and conspiracy theory

We mention this not because it’s some conspiracy theory, but because a top adviser to China’s central bank has issued a rare critique of his country’s economic policy, urging the government to set a binding inflation target, increase spending to deal with of weak consumption and even starting to provide money from a helicopter.

Huang Yiping – a prominent member of the People’s Bank of China’s Monetary Policy Committee – urged that the authorities should change their strategy:

- “to focus on investment and not fuel consumption”,

- to support consumption,

- set a hard inflation target of 2-3%,

- adopt fiscal measures to support consumption (such as allowing migrant workers to settle in cities, which would deal with China’s new housing bubble overnight)

- to give money directly to households!

“The economy has entered a new stage, and aggregate demand—including consumption, exports, and even investment—is no longer as strong as before. This actually poses new challenges for macroeconomic policies,” Huang pointed out.

Meanwhile, an excessive focus on fiscal stability — such as keeping the fiscal deficit below 3 percent of GDP even when growth is weak — is now holding back China’s economy and eroding the room for future policy action, he said, continuing .

Huang believes that if the Chinese economy falls into the trap of low inflation (like Japan) “the consequences will be severe” and global in scope.

In fact, we’re surprised that amid growing social discontent, record youth unemployment and a particularly disgruntled Chinese middle class, Beijing hasn’t already done this.

Maybe – soon – and in doing so it will trigger an inflationary shock wave around the world.

The two speeds

Balancing China’s two-speed economy has been a challenge as authorities rely on manufacturing to fuel growth while risking a global oversupply due to pipelines.

Huang’s outspoken criticism comes as public criticism of the Chinese government’s measures has grown increasingly vocal as policymakers struggle to stem slowing growth.

Huang highlighted falling prices – without using the word deflation – as the key issue requiring more attention and advocated setting a tough target for China’s consumer price index growth of 2%-3%.

Policymakers have consistently targeted inflation at 3% in the past, but it is not considered a binding target.

In light of recent CPI figures that have been stuck around 0% for much of the past year, Beijing will consider inflation of 2%, perhaps even 30%, lucky

“The economy is now easy to cool down but difficult to warm up,” said Huang, who is also dean of the National Development School at Peking University.

“If it really falls into the trap of low inflation, the consequences will be severe,” the central banker said, having learned from Japan’s disastrous experience. After China extended its longest deflationary streak since 1999 last quarter, Huang questioned whether the world’s No. 2 economy could fall into the same cycle as Japan, which has suffered decades of deflation and reported more than a dozen times in his observations.

Huang took care to strike a constructive tone in his lengthy speech, describing government interventions as “mild” in the face of “new conditions emerging in the economy” and accusing them of having a weaker effect than desired.

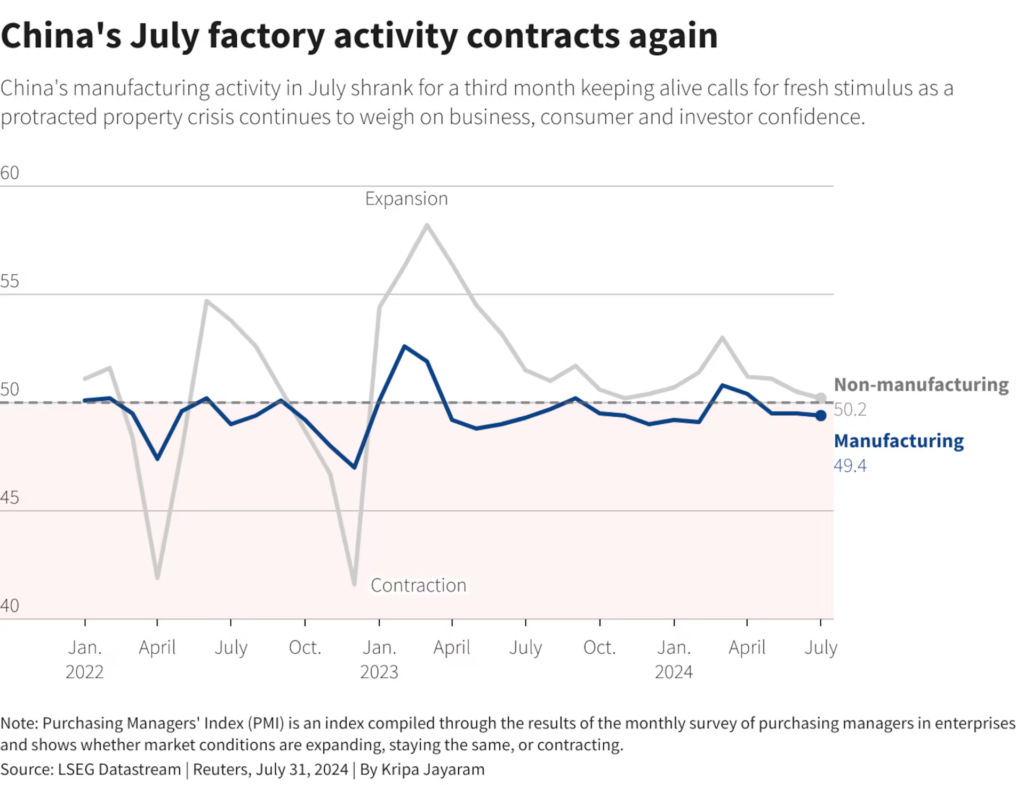

Home sales in China fell again in July, despite Beijing boldly stating the policy goal of supporting a protracted housing market.

According to Huang, two popular but erroneous views stood in the way of appropriate policies. One was the belief that only structural reforms could increase productivity and the second was an aversion to adopting the more aggressive policies pursued by Western countries.

The massive fiscal measures adopted by the U.S. and Europe in recent years had effectively supported these markets without causing any major negative effects, added Huang, who has worked at global investment banks including Citigroup and Barclays.

Yes, his assessment lacks economic logic—massive fiscal expansion has led to ballooning inflation—but for China and its 1.3 billion citizens, deflation is even more dangerous than inflation.

Excessively conservative fiscal measures could threaten the long-term economic stability of the Chinese economy.

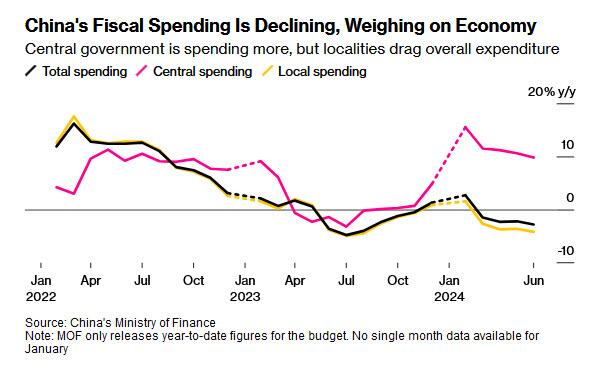

Pressure on the balance sheets of households, businesses and local governments is fueling the weakness of the economy.

This means that the central government needs to shoulder more responsibility and stabilize trust.

If the US slips into recession, which now seems inevitable, China will have no choice but to do as the PBOC adviser suggests, as the only pillar supporting the Chinese economy – US imports – slowly disappears.

Should that happen, and if Trump implements the new policy on tariffs (increasing up to 100%) that he hopes to implement once elected, the inflationary tsunami that awaits in 2025 will make the galloping inflation since the early 1980s seem like a mild price increase by comparison.