Ukraine, as can be seen from developments both in the context of Russia’s military operation and in the economy, is losing the battle on two fronts: military and economic.

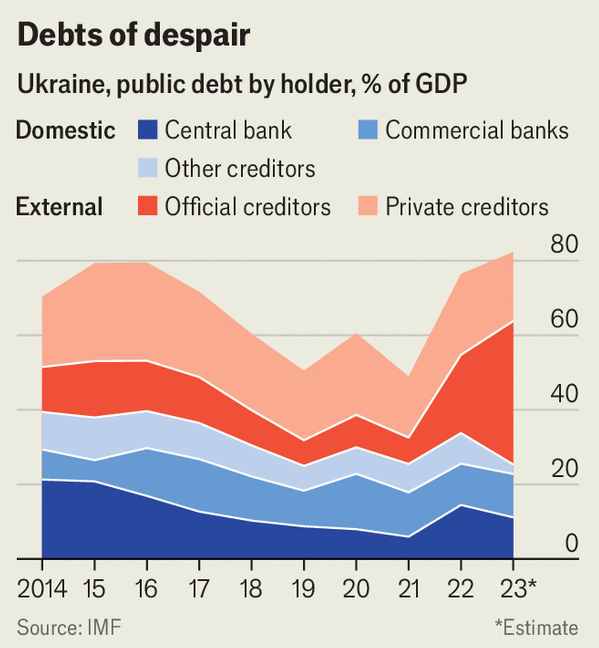

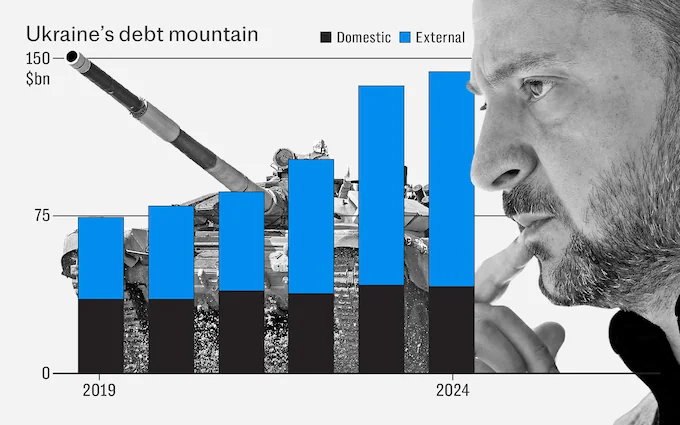

Global attention is understandably focused on developments on the battlefield as Russian troops press toward Ukraine’s second city, Kharkov. But Ukraine is experiencing an economic cliff at the same time. With its war-damaged economy and defense costs for the year estimated at $54.4 billion, Ukraine is on the brink of bankruptcy with $22.8 billion in debt.

For Ukraine, debt is not an accounting exercise – it represents its ability to defend its sovereignty and secure its future. At the start of the war, private investors led by JP Morgan agreed to freeze Ukraine’s debt repayments. The deal is set to expire in August. Both Ukraine and its creditors are scrambling to reach a last-minute debt deal to avoid default.

The country is out of markets

These debt restructuring talks are common between states and investors, but usually take years and rarely occur in the context of war. For now, the two sides remain far apart in their negotiations. Ukraine is demanding a 40% reduction in its debt obligations and investors are only willing to take a 20% loss – known in financial circles as a ‘haircut’. Ukraine faces a compromise in its debt negotiations.

On the one hand, securing more debt reduction, or even an outright default, could free up significant fiscal resources in the short term. This would allow Ukraine to redirect funds from debt payments to immediate war-related needs.

However, the long-term consequences of such a decision could be severe, with higher borrowing costs and longer periods of exclusion from capital markets. The outcome of these negotiations will shape not only Ukraine’s immediate defense capabilities but also its long-term economic resilience.

A country’s ability to access credit markets plays an important role in determining the outcome of a war. States with lower borrowing costs are much more likely to win their wars. Debt allows states to mobilize more resources, faster than they could otherwise.

The cheaper the debt and the easier it is to access, the more resources that country can mobilize for its war effort. Because of the importance of debt to war, states involved in wars rarely go bankrupt. The risk of losing access to credit markets is usually very high. There are, however, some notable exceptions.

The technical bankruptcy of Russia

Russia technically defaulted on its debt shortly after invading Ukraine in 2022 because sanctions made it impossible to pay the debt. And Saddam Hussein’s Iraq was bankrupt in the midst of the Iran-Iraq war in the 1980s. But both countries had significant wealth of natural resources to tap into, a luxury that Ukraine does not have.

The exceptions of Russia and Iraq highlight another critical factor in wartime financing: the nature of a country’s political system. As empires, Putin’s Russia and Saddam’s Iraq could impose restrictive economic measures during wartime. The Russian government, for example, has imposed controls that make it difficult for exporters and foreign companies operating in the country to take money out of Russia.

Instead, the Ukrainian government must be sensitive to the domestic political pressures of war financing. Measures such as those adopted in Russia would likely spark political discontent in Ukraine. Debt allows Democratic leaders to mobilize resources without relying on unpopular fiscal strategies. However, facing the prospect of reduced access to debt, Ukraine reverted to divisive tax policies that increased the tax burden on individuals while reducing social spending.

Taxes are important to the war effort, but they risk undermining the domestic support needed to keep the fighting going. And the Ukrainian government has been accused by journalists and international groups of taking too much notice of domestic discontent.

The economic chaos in Ukraine

However, there is some good news for Ukraine’s leadership. After a long delay, the US Congress approved a $60 billion military aid package in the spring. At the same time, the United Kingdom provided the largest aid package to Ukraine, worth more than $3.8 billion for 2024. More recently, the G7 (which consists of Canada, France, Germany, Italy, Japan, the UK and the US) agreed to use Russia’s frozen assets to finance a new $50 billion loan to Ukraine.

These additional financial resources are needed for Ukraine’s war effort. However, they do not solve the immediate debt problems. UK and US aid packages are only for military equipment and cannot be used for budget support. The G7 loan will be more flexible, but that money is not expected to be delivered until later this year.

Ukraine must balance immediate war financing needs with long-term economic concerns and domestic political pressures. The stakes couldn’t be higher. The terms Ukraine secures in the debt negotiations will affect not only its ability to finance the current war effort, but also its ability to rebuild its economy once the conflict ends.