The US national debt, which is over 120% of GDP, is a mathematical deterrent to real, not debt-based, growth. Debt-based “growth” is not real growth, but more debt. The war on inflation, which FED Chairman Powell famously described as temporary, is not only far from over, but the worst wounds (ie the pains of inflation) have yet to come to the fore. Simply put, Powell needs inflation and a depreciating dollar to service not only the growing US public debt, but also unfunded liabilities off the government balance sheet.

In this fatal debt substratum, the FED—and therefore the US economy and the dollar—is now openly trapped, and whatever one thinks of Putin, one knows this to be true. Powell’s rate hikes from 2022 were indeed deflationary, but they strengthened the US dollar, crushed bond prices and sent yields skyrocketing – thanks to foreigners holding more than $13 trillion in debt. This caused foreigners to sell 7.6 trillion in bonds for dollars.

The net result was an increasingly disorderly bond market as dollars rose while bond prices fell, which added more depth to US deficits (fiscal sovereignty), more pain to small businesses, more US interest, tighter bank lending and more debt issuance from the US.

However, no one wants US bonds anymore. Confidence in US debt is fading, as is confidence in the “weaponized” dollar. Central banks know this, and so does Vladimir Putin.

So unless USA wants to default on his debt or allows a US Treasury auction to fail (it won’t happen), the only realistic option for dollar liquidity (short of Bretton Woods 2.0) will boil down to more synthetic liquidity: first from repo markets and the Treasury General Account (as seen in September 2019 and 2022 and March and October 2023) and finally from new QE (quantitative easing). As for when Super QE will start, don’t look for dates.

No one knows – but it’s coming, and at a faster pace than in the past. But what does all this debt, bond, currency and Fed dysfunction mean for the average citizen, your markets and fiat money? Probably, a lot. The middle income class is ending.

Stocks, Gold, BTC and Bonds

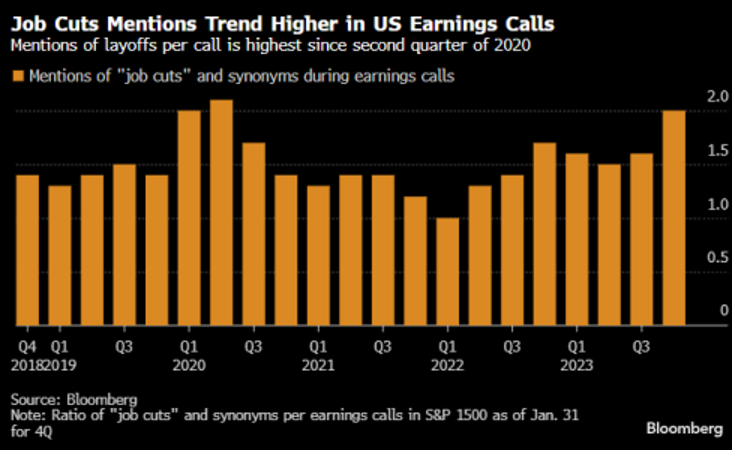

Job cuts are objectively bullish on markets, which boosts profits for companies with fewer expenses. Full-time employment fell by 1.4 million Americans in the past 3 months, a rate rarely seen in US history, while politicians brag about GDP growth.

But GDP “growth” comes from deficit spending (deficit to GDP at 8%), not a strong growth spurt. In the short term, these dysfunctions, layoffs, forecasts of lower interest rates from the FED, and embarrassing debt levels are actually bullish for stocks.

Despite the market opening in 2024 at all-time highs reminiscent of the dot.com craze, the market is dangerously tight – led by Amazon, Microsoft, Nvidia and META. The fact that Microsoft is bigger than France’s GDP, while, in the space of 30 days, Nvidia has become another Tesla in terms of its capitalization, with unbearable movements of pairs of factors.

The signals we see look almost identical to 1998-2000, 2006-08 and 1970-73, conditions that ended in “carnage-blood”.

Long-term investment wisdom

Longer-term investors tend to be more prudent than short-term speculators.

They see the debt spiral of US currency and IOUs (as measured by the US Treasury Index or TLT). The rising performance of the GLD/TLT, BTC/GLD and SPX/TLT indices (i.e. Gold, Bitcoin and the S&P are outperforming the US10Y bond), for example, is pretty clear evidence that the markets are seeing what we’ve been warning, ie :

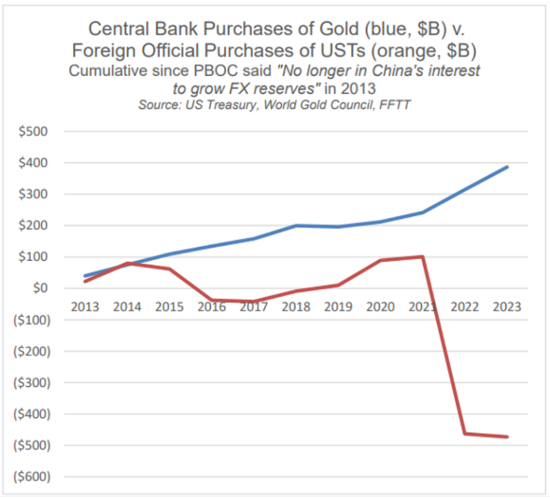

Cash and bonds are no longer a “safe haven” in a nation on its knees with debt and a devalued dollar. At the same time, more and more nations are moving away from the dollar, settling their trade relations in gold rather than dollars. Premiums in the SGE, as well as the pricing of the metal, move from West to East. At some point, the 200-day moving averages in the price of gold set on the London and New York exchanges will have to reflect rather than ignore what is happening in the increasingly popular Chinese stock market.

And speaking of SGE, big things are happening right before our eyes. Notably, SGE just saw 271 tonnes of gold withdrawals in a single month, the most on record in 10 years.

If the dollar price of gold were to crash, then oil prices would have to crash along with the price of gold, which would “crush” US shale oil production and cede the global black gold market to Russia and Saudi Arabia. This makes the US nervous. And most importantly, it will force some changes.

More simply, thanks to the West’s surprise sanctions against Putin, the West now has an unwitting vested interest in keeping gold at a fairer price. Besides, the US can’t just ignore what the rest of the world is doing with gold and oil. In other words, the East, in short, is now reminding the world, and the West, that in a world of increasingly lousy paper dollars, money printing, and disappearing debt: Gold matters.

This means that the US-led West will have to face tough realities about currency and debt markets. Putin, trusted or not, has proposed peace and more cooperation. Will the US Pentagon and State Department, so openly disconnected from citizens, pursue the same? Or will Washington just do what Hemingway warned about by dragging us into wars and a devalued dollar?