Nobody likes tough macro events, especially during the holiday season, but some things need to be said, according to Trust Economics.

As you know, US Federal Reserve Chairman Jerome Powell has promised that 2024 will be the year of interest rate cuts. In this regard, it should be pointed out that Powell is neither a dove, i.e. an advocate of very loose monetary policy, nor a hawk, i.e. a devotee of monetary tightening. We’d say it’s more like a Christmas turkey or goose. His biggest problem, on the other hand, is that he cannot accept the failure of the goals or – even to speak once released with honesty.

In any case, Trust Economics’ raw views on debt markets, bond volatility, interest rate swings and the FED’s honesty with the FED itself (with its views), this shift towards rate cuts it should come as no surprise.

As has been mentioned many times in the past, rising interest rates, i.e. the increase in the cost of money, is a dark force with particularly destructive power. Already the things that are broken are few: banks, British bonds, US bonds, middle class. There is no central banker who has not acknowledged this grim situation.

It is recalled that Powell raised interest rates so that the recession, which we are already experiencing, will be officially declared in 2024 NBER. Of course, the central banker of the USA is a position of political responsibility and, like any politician, he has learned the art of bending the truth in order to stay in his position in the long term.

It’s the recession, “stupid”!

Even Powell, despite his rhetoric about hitting the target on reducing inflation through the Volcker strategy, i.e. “keeping” interest rates high for a long time, always knew (and still knows) that the US is in already in deep recession, hungry for cheaper prices and even more debt.

The evidence for the cause of the recession, according to Trust Economics, is literally everywhere:

- from classic economic indicators such as the yield curve

of bonds (inverted), - the Conference Board of Leading Indicators (sunk down

from the 4% threshold last December) - up to the dramatic 4% reduction in the money supply

M2 (inherently deflationary), - the main indicators of the real economy, such as:

- record bankruptcies,

- continuous layoffs,

- credit card defaults (Oliver Anthony index).

So lower interest rates are needed – but there are other reasons that call for monetary easing.

The Fed serves Wall Street (and capital gains taxes), not the real economy. And Wall Street is screaming for help.

The overvalued and cheap-money-addicted S&P 500 is littered with countless zombie businesses staring down the barrel of $740 billion in convertible debt due in 2024 and another $1.2 trillion in 2025 due to higher interest rates.

Of course, a huge problem is the US debt which is staring at the US from the 34 trillion euro levels and is a ticking time bomb for the global economy, as interest rates will continue to appreciate over the next 36 months.

That’s why we at Trust Economics will continue to say that interest rates will have to, in order to avoid a market bloodbath and a debt trap, be cut soon – something that Jerome Powell has already announced – which competitive force, if not what else must have mystical powers.

Predicting any short-term movement in the markets, or even in the mind of an Fed official (which is essentially the same thing now), is indeed like playing dice: No one can pick the day, hour, or even month of a move. of the watershed. But for those watching deficits, debt markets, and thus bond dysfunction, the signals being emitted (i.e. basic math) offer very good ideas and clear evidence of what’s coming.

The clouds warn of the coming rain. But what do the storm clouds (the debt bubbles) show?

In Trust Economics’ view, the clouds we see in the bond markets are easily visible to anyone willing to open their eyes – except perhaps politicians, who prefer to keep their well-made heads buried in the sand, ostriching.

For months and months, we’ve been saying over and over again that debt matters and therefore, by extension, bond markets. Fatally the FED and other central banks will fail as the increased cost of money will force new money to be printed just to service the interest payments on the horrendous US government debt.

This is called “Fiscal Sovereignty”

Powell halted interest rate hikes. And now, as 2023 expires, he’s talking about rate cuts for 2024 – which is shocking.

When official (as opposed to honest) CPI inflation falls while interest rates (as best measured by the yield on the unloved US 10-year) rise, then “real” (ie inflation-adjusted) interest rates go positive and north.

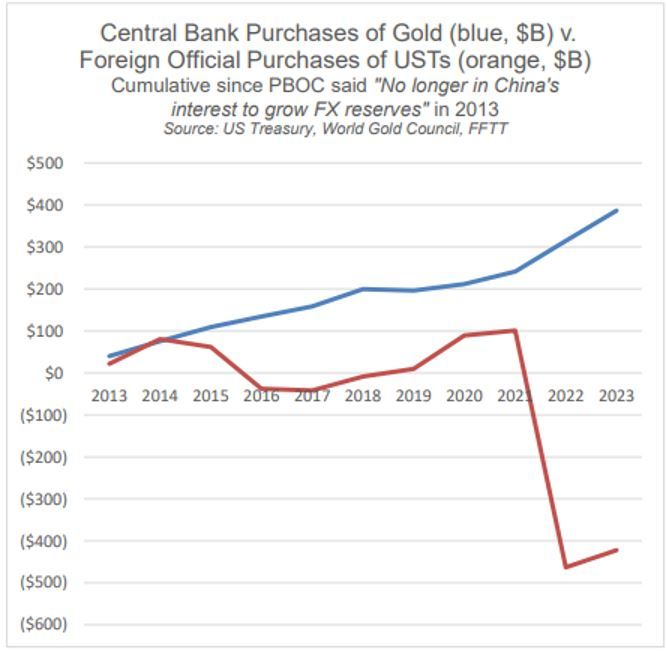

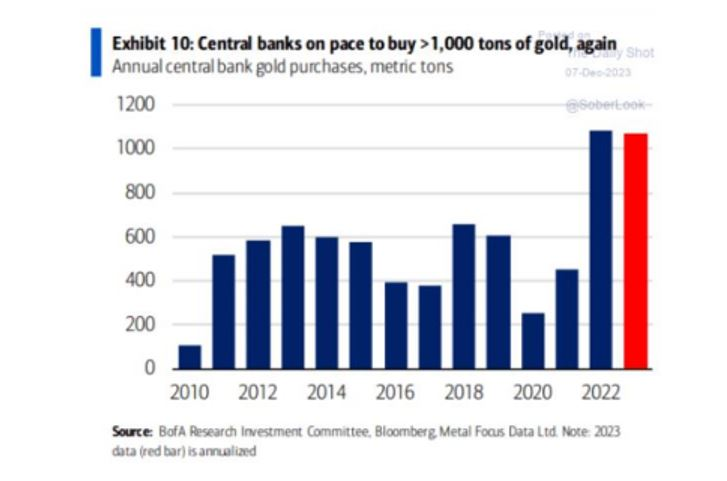

And when real interest rates approach 2%, that means debt becomes really painful for companies, individuals and, of course, governments like the US. Meanwhile, the rest of the world knows this, which is why central banks are dumping non-favored US Treasuries (red line) and piling on gold (blue line), insisting they hold real money rather than an impaired asset.

This global dumping of US Treasuries pushed the prices of all debt securities down and therefore yields and interest rates up, meaning that US interest payments worsened by $1 trillion a year. And even Janet Yellen, having moved from FED Chair to Treasury Secretary, realized there was a problem with Powell’s rate hikes.

As Janet Yellen admitted just last week: “Rising real interest rates may affect the FED’s decision on the path of interest rates.”

Of course, there was never any demand for US bonds from the rest of the world, only policymakers were satisfied with the strategy of quantitative easing. So they saved the US 10-year bond from an oversupply slump for the time being simply by over-issuing more bonds from the short end of the yield curve – just buying time with this strategy.

At the same time, Washington shuffled risk from ten-year to two-year, draining $150 billion per month of liquidity from the US Treasury’s General Account. But if, according to the consensus, November was a victory for the FED and bonds, why is the December version of the once-hawkish Powell talking disdainfully about rate cuts in 2024?

From false victory to open collapse: There are no good options at the FED. The simple answer is because the US is not in a period of victory, but in a period of open and obvious decline that is clear to all.

Why? Because debt destroys nations and therefore central planners, who have nothing but bad options to deal with very bad math. That is, if they don’t cut interest rates and print more fake money, assets are at risk and the economy will descend into a severe recession. But if central bankers loosen policy to save the system, they will kill the currency’s inherent purchasing power—which is exactly what Powell will do next.

Scary math

According to the Economics Trust, the only thing we can do is simply reflect on the facts and not the drama of a nation whose debt profile makes growth impossible.

- Current US debt to GDP has crossed the 100% red line, in the 120% range.

- The federal budget deficit in terms of GDP is at 8% and growing.

- The Net International Investment Position (ie, the piggy bank of foreign assets) is at negative 65%.

- The public debt is at 34 trillion. dollars, and according to the Congressional Budget Office, the US is going to get rid of at least another 20 trillion. dollars in US Treasuries over the next 10 years – and that modest number (?) assumes no recession in the interim.

- The combined public and private debt in the US is about 100 trillion dollar.

But who will buy US bonds to cover their ballooning deficits? According to simple math and hard facts, the answer as of 2014 is the FED.

We can assure you that no one in Washington knows how to pay this debt. Debt Collateral Damage: The Dollar, Inflation, Markets, etc.

US Dollar: The Relative strength is not enough

As for the dollar, it remains the world’s reserve currency and the world still needs it.

-70% of world GDP is measured in dollars,

-80% of world trade is settled in dollars.

There is a lot of demand for dollars – mainly from the dollar-euro markets, derivatives markets and oil markets. So this “super currency” (ie the dollar) is extremely strong, and therefore the need for dollar liquidity is a huge headwind for the US currency.

But this huge aura wind is not an immortal aura wind. The evidence of increasing de-dollarization following US-Russia sanctions (and the weaponization of the dollar) is not an urban myth, but an open and undeniable reality. China and Russia are increasingly moving to buy oil in yuan (which Russia then converts into gold in Shanghai), while an exponentially increasing number of bilateral trade deals between the BRICS+ countries are now conducted outside the dollar.

Just like the gold decoupling during the Nixon presidency

in 1971 led to the slow death of the dollar’s inherent purchasing power, its weaponization will lead to the end of its global hegemony.

We warned about this from day 1 of sanctions against Russia. For now, however, the dollar is still the dominant currency, but its relative strength does not appear to be pushing the dollar index (DXY) past 150.

This is for the simple reason that even the US knows that the rest of its friends and foes cannot afford to pay off $14 trillion in debt without having to dump most of the roughly $7.6 trillion worth of US bonds held abroad. dollars), which would crush the pricing of US bonds and send yields and interest rates skyrocketing.

In short: even the US is afraid of rising interest rates and an excessively strong dollar. Such a fear of rising interest rates combined with the reality of growing US deficits (and thus the growing need for more US bonds) will soon lead to excessive bond supply/issuance. And the only buyer of US bonds,

that will control yields/interest rates, it will be the FED, not the rest of the world (See chart above…).

However, this kind of bond buying with money created out of thin air kills a currency. In this case the FED would have to print trillions of dollars to buy its own government bonds – a

inherently inflationary policy that weakens rather than strengthens the dollar in the long run.

This is why Powell’s “pause” and now “rate cut” in 2024 will eventually be followed by “mega-money printing.” We saw this exact pattern between 2018 (QT) and 2020 (unlimited QE). The future therefore looks ominous, as money creation brings devaluation and therefore more inflation.

But first, deflation

But before that we’ll have to go into an “official” recession in 2024 – and recessions are inherently deflationary, if not downright deflationary. Again, the inflation-deflation debate is not a debate, but a cycle.

Historically, moreover, dramatic declines in the M2 index always lead to deflation. Always.

As for the stock and bond bubbles, the markets certainly like cheaper debt (ie lower interest rates) and unconditional QE. For now, of course, they are waiting. With 25% of US GDP sitting in cash equivalents, Powell’s projected rate cuts in 2024 will send much of that money into already existing market bubbles, sending asset inflation even higher, which means more tax revenue for the US government.

If the dollar index (DXY) remains low, markets will rise. And if the FED is accommodative, markets will rise as well. This includes Bitcoin and the digital dollar.

It’s that simple: tight policies are a market headwind, loose policies are a headwind. This is because capitalism is long dead and needs to be reborn, and the FED is essentially the de facto market maker for the S&P, Dow & NASDAQ.