For decades governments and corporations have issued trillions of dollars worth of debt, whose servicing costs rise and fall with inflation. But the cost, which was cheap when prices remained stagnant, quickly turned into an expensive one. Inflation concerns the broader challenges that have arisen at the end of a more than decade-long era in which money around the world flowed easily and cheaply, a period in which borrowers were lent huge sums at very low, and sometimes negative, interest rates.

But now investors are wary, following the crisis in US regional banks this year, and emerging pressures in commercial real estate. Borrowing costs have risen sharply for governments, businesses and consumers as central banks have raised their key interest rate to absorb price pressures. Interest rates have soared on inflation-linked loans, but they are not the only source of pressure.

When fixed-rate bonds mature, they must be replaced with more expensive new debt. Meanwhile, interest rates on loans are usually floating, which means they are quickly affected by changes in interest rates.

Yields on 10-year fixed-rate bonds, a proxy for government borrowing costs, have climbed to around 4.3% in the UK and 3.9% in the US. Both yields were below 1% during the pandemic.

The 2.2 trillion dollars the cost of paying interest

According to the estimates of Fitch Ratings, only for this year the governments around the world will have to pay a total of about 2.2 trillion. dollars in interest. The US Treasury’s interest costs rose 25% to $652bn in the nine months to June. Germany’s debt servicing costs are expected to jump to 30 billion euros this year, from 4 billion euros in 2021.

At the end of 2022, governments had 3.5 trillion. dollars in outstanding inflation-linked debt, according to the Bank for International Settlements, which translates to nearly 11% of their total borrowing.

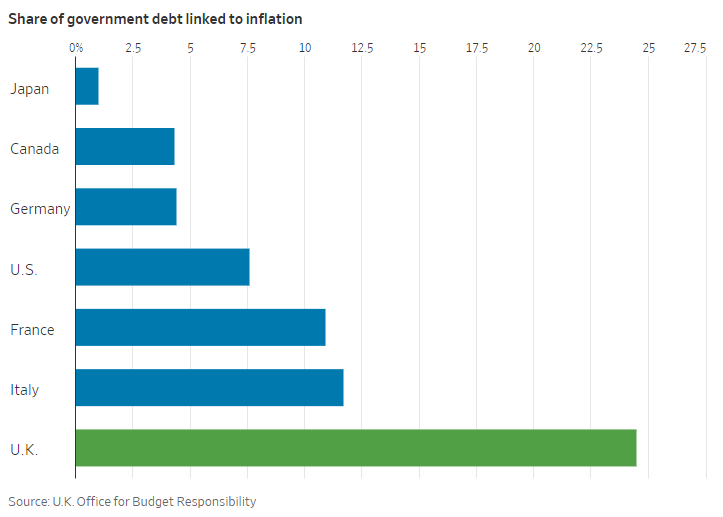

The “black sheep” of the inflation-linked debt problem is Britain

The “black sheep” of the inflation-linked debt problem is Britain, which has experienced the fastest rise in debt costs in the G7. The United Kingdom first saw this type of debt positively under Margaret Thatcher’s prime ministership and in 1981 became one of the first developed economies to issue inflation-linked debt: securities known as linkers in Britain and Treasury Inflation-Protected Securities, or TIPS, in the US. Both the amount owed to investors when the bonds mature and the regular interest payments they receive fluctuate based on inflation.

Around a quarter of the UK’s debt is now linked to inflation, following the example of some emerging markets with a history of out-of-control prices such as Uruguay, Brazil and Chile.

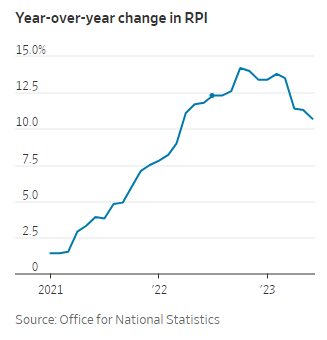

Britain’s debt problems are compounded by its long-standing reliance on a measure of price growth that is out of favor: the retail price index, or RPI. Around £600bn of bonds are linked to this measure, which has consistently risen faster than the most widely used measures of consumer prices. London has committed to phasing out RPI by 2030.

Inflation, as measured by the RPI, topped 14% in October and was still at 11% in June compared with a year earlier. Economists expect UK inflation to continue to ease this year, although more slowly than in other major economies.

Theory is far from practice

In theory, higher interest payments should be offset by increased revenue. While higher inflation means bigger payouts to bondholders, it should also bring in more taxes.

This logic is particularly true in markets like Britain, where inflation indicators are deeply embedded in the economy. Tax thresholds, pensions and welfare spending, rail tickets and mobile phone bills are often linked to price indices.

But the energy shock that fueled recent inflation upended that math, as higher energy bills pushed the Consumer Price Index higher even as earnings and consumer spending lagged. The UK is experiencing the “wrong kind of inflation”, Britain’s Office for Budget Responsibility said this month. The sensitivity of UK debt to inflation is unprecedented, he adds.

The UK’s debt sustainability has been at the center of investor attention since last autumn’s market crash, triggered by then-Prime Minister Liz Truss’ plans to cut taxes.

Her successor Rishi Sunak and Finance Minister Jeremy Hunt have sought to restore market confidence with pledges to contain inflation and reduce debt. As Britain’s interest costs rise and with debt now over 100% of GDP, these promises are becoming increasingly difficult to keep while maintaining investor confidence.

The debt burden also undermines Sunak’s hopes of persuading voters and reviving the economy with tax cuts and spending measures ahead of elections due next year.

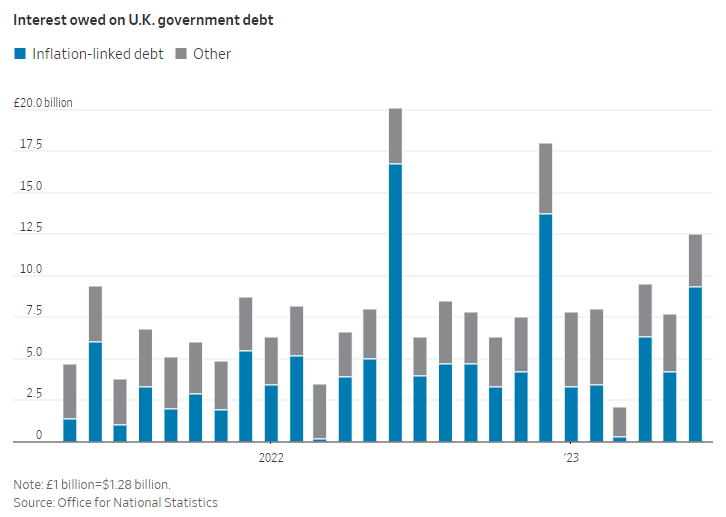

Service costs follow the upward trend

Higher bond yields and persistent inflation will add an extra £30bn to the cost of servicing UK government debt, Trust Economics estimates.

The government’s options are it could raise taxes or it could borrow more. One could certainly say that this increase in debt interest costs is incompatible with reducing taxes.

Britain is selling fewer inflation-linked bonds, which are likely to make up 11% of bond issuance this financial year, down from more than 20% throughout the 2010s.

But the linkers have largely done their job as envisioned in the 1980s. It was a decade in which inflation was extremely high. People were very wary of the ability of any government, especially the Conservative government, to reduce inflation to a low and stable rate.

Fears that these bonds would lead to new wage-price spirals, as unions demanded increases to keep pace with inflation, did not materialize. Thatcher, who has called inflation the “ruiner of everything”, saw the linkers as “sleeper cops”, ensuring the government would not be tempted to let inflation run wild to help inflate the debt. Linkers make the current fiscal position more difficult. But that is what Mrs Thatcher really wanted. He wanted governments to fight inflation more vigorously.

Companies are also feeling the pressure from inflation-linked debt. The UK’s biggest water company, Thames Water, has nearly collapsed in recent weeks as investors have questioned its ability to repay £14bn of debt, around half of which is linked to inflation. Thames Water’s debt is linked to inflation, but customer prices now follow the consumer price index, which lags RPI by around 3 percentage points.